The Strategic Benefits of Dollar Cost Averaging in 2026: A Guide for Cost-Conscious Investors

As we navigate the financial landscape of 2026, the retail investment world has undergone a significant transformation. With market volatility becoming the “new normal” and a plethora of digital assets vying for attention alongside traditional equities, the modern investor faces a daunting question: How do you build wealth without falling victim to the erratic swings of the global economy? The answer lies in a timeless, disciplined strategy that has regained immense popularity: **Dollar Cost Averaging (DCA).**

Dollar Cost Averaging is the practice of investing a fixed amount of money at regular intervals, regardless of the asset’s price. In 2026, this strategy is no longer just for the “set it and forget it” crowd; it has become a sophisticated tool for retail traders looking to minimize costs and mitigate the psychological stresses of market timing. By removing the guesswork from the equation, DCA allows investors to harness the power of compounding while systematically lowering their average purchase price over time. This article explores the multifaceted benefits of DCA in the current market environment and why it remains the gold standard for long-term wealth accumulation.

—

1. Navigating Volatility: Why DCA is Your Best Defense in 2026

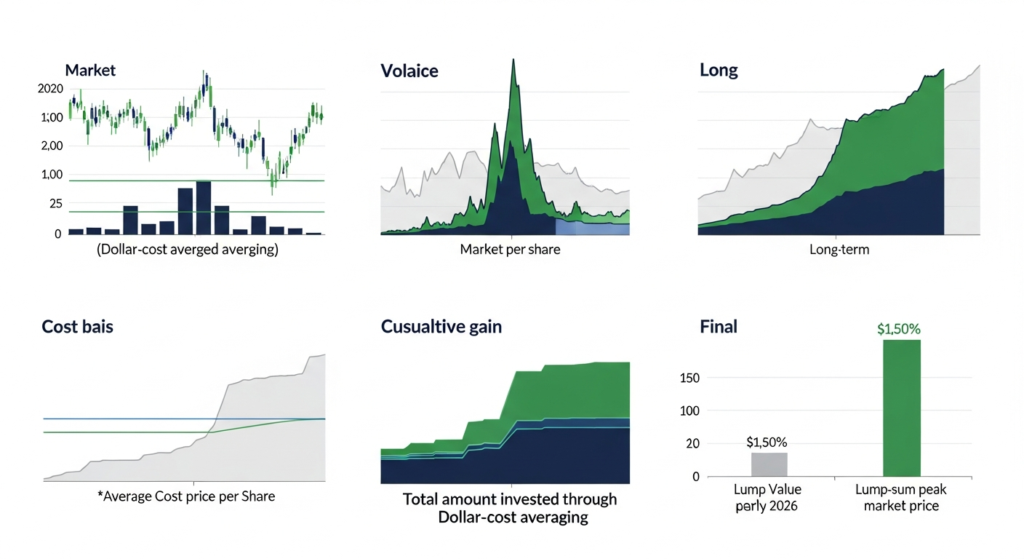

The market environment of 2026 is characterized by rapid information flow and algorithmic trading, which often leads to heightened intra-day and intra-week volatility. For the retail investor, trying to “time the bottom” in such a climate is a statistically losing game. Dollar Cost Averaging serves as a natural hedge against this turbulence.

When you commit to a DCA plan, market dips are no longer viewed as catastrophes; instead, they are seen as opportunities. Because you are investing a fixed dollar amount, you automatically buy more shares or units when prices are low and fewer when prices are high. This inverse relationship ensures that your investment health isn’t dependent on a single entry point. In a 2026 economy where geopolitical shifts and technological breakthroughs can cause sudden market corrections, DCA provides a “smoothing” effect that stabilizes your portfolio’s growth trajectory.

Furthermore, DCA protects investors from the “sequence of returns” risk. If an investor were to put a lump sum into the market just before a significant downturn, it could take years to break even. By spreading those entries across weeks or months, the investor ensures that they are participating in the recovery just as much as the decline, often resulting in a faster return to profitability.

2. Minimizing Emotional Bias and Decision Fatigue

One of the greatest hurdles for retail traders in 2026 is the psychological toll of the 24/7 news cycle. The “Fear of Missing Out” (FOMO) and “Fear, Uncertainty, and Doubt” (FUD) are amplified by social media and real-time financial apps. Emotional investing—buying at the peak due to excitement or selling at the trough due to panic—is the primary reason retail portfolios underperform the broader market.

DCA effectively “automates” your discipline. By establishing a pre-set schedule, you remove the need to make a difficult decision every time you have extra capital. This reduction in decision fatigue is crucial for maintaining a long-term perspective. In 2026, the most successful investors aren’t necessarily those with the best charts, but those with the most consistent habits.

When the market is “in the red,” the natural human instinct is to hesitate. However, a DCA plan executes regardless of sentiment. This mechanical approach ensures that you stay the course during periods of irrational pessimism, which is historically when the most significant wealth is built. By taking the “ego” out of investing, DCA turns a high-stress activity into a routine administrative task.

3. Lowering Your Average Cost Basis in a Maturing Market

The mathematical core of Dollar Cost Averaging is its ability to lower the average cost per share over time. As we look at the maturing markets of 2026, where “explosive” growth is often followed by healthy consolidation, the average cost basis becomes a vital metric for retail success.

Consider an example: if you invest $500 monthly into an Exchange Traded Fund (ETF). In Month 1, the price is $50 (you buy 10 shares). In Month 2, the price drops to $40 (you buy 12.5 shares). In Month 3, the price recovers to $45 (you buy 11.1 shares). After three months, your average cost per share is approximately $44.60, even though the price spent time at $50.

In a sideways or fluctuating market—which many analysts predict for the mid-2020s—this math works heavily in favor of the retail investor. You are essentially “averaging down” without needing to monitor the ticker symbol every hour. For traders focused on minimizing costs, reducing the average purchase price is the most effective way to increase the eventual profit margin when the asset reaches new highs.

4. Leveraging Fintech Automation and Time Efficiency

In 2026, the integration of financial technology has made DCA easier and more cost-effective than ever before. Most modern brokerage platforms and neo-banks offer “Auto-Invest” features that allow for daily, weekly, or monthly contributions with zero manual intervention.

For the retail investor, time is a finite resource. The era of spending hours analyzing candlestick patterns is being replaced by a focus on “life-centric” investing. DCA allows you to spend your time on your career, family, or hobbies while your wealth grows in the background. The automation available in 2026 also allows for “micro-investing,” where spare change from daily transactions is rounded up and funneled into a DCA plan.

This level of convenience minimizes the “friction” of investing. When the process is automated, there is no opportunity to “forget” to invest or to decide to spend that money on a whim. The 2026 investor treats their DCA contribution like a non-negotiable utility bill—a bill paid to their future self.

5. Integrating DCA with Low-Fee Platforms and Fractional Shares

A major shift for retail traders in 2026 is the universal availability of fractional shares. Previously, DCA was difficult for high-priced stocks (e.g., a stock trading at $3,000 per share). An investor with only $100 a month couldn’t participate. Today, fractional ownership allows you to DCA into any asset, regardless of its nominal price.

Furthermore, the competitive landscape of 2026 has driven commission fees to near zero across most major platforms. This is a game-changer for the DCA strategy. In the past, frequent small purchases would be eaten away by transaction costs. If a trade cost $5, a $50 investment would immediately lose 10% of its value to fees.

Now, with zero-commission structures and low-spread environments, you can break your investments into much smaller, more frequent increments (like daily DCA) without any cost penalty. This allows for an even more granular “smoothing” of the price curve, ensuring that you capture the most accurate average price possible. For the cost-conscious trader, 2026 represents the most efficient era in history to implement a DCA model.

6. Long-Term Wealth Accumulation and the Power of Compounding

While DCA is a strategy for entry, its ultimate goal is to facilitate the power of compounding. In the economic landscape of 2026, where inflation-hedging and sustainable growth are priorities, the “time in the market” remains more important than “timing the market.”

By consistently adding to your positions, you are increasing the base upon which dividends and capital gains can compound. Many retail investors in 2026 utilize “DRIP” (Dividend Reinvestment Plans) alongside their DCA strategy. This creates a powerful dual-engine for wealth: you are buying more shares with your income, and your existing shares are buying even more shares through dividends.

Over a 5 to 10-year horizon, the difference between a sporadic investor and a DCA investor is often staggering. The DCA investor benefits from the “snowball effect,” where the sheer volume of shares accumulated during market lulls provides an enormous lift when the market enters a bull cycle. As we look toward the late 2020s, this disciplined accumulation is the most reliable path to financial independence for the average retail participant.

—

FAQ: Dollar Cost Averaging in 2026

**Q1: Is Dollar Cost Averaging better than a Lump Sum investment in 2026?**

While a lump sum investment can outperform DCA in a strictly trending bull market, DCA is generally considered superior for risk management in volatile environments. Given the uncertainties of 2026, DCA protects you from the risk of investing a large amount of capital right before a market correction. It offers peace of mind that a lump sum cannot.

**Q2: How often should I schedule my DCA purchases?**

The frequency depends on your cash flow. In 2026, many traders prefer weekly or even daily DCA to capture the most price points. However, monthly DCA is perfectly effective for most retail investors. The key is consistency rather than frequency; the most important thing is that you do not skip your scheduled intervals.

**Q3: Does DCA work for high-volatility assets like Crypto or Tech stocks?**

Actually, DCA is *most* effective for high-volatility assets. Because these assets have larger price swings, the “averaging” effect is more pronounced. By using DCA for volatile sectors in 2026, you avoid the trap of buying at a local “hype” peak and benefit significantly when the price inevitably dips.

**Q4: Can I still use DCA if I only have a small amount of money?**

Absolutely. Thanks to the fractional share technology and zero-commission fees prevalent in 2026, you can start a DCA plan with as little as $5 or $10. This democratization of investing is one of the primary reasons DCA has become the go-to strategy for the modern retail trader.

**Q5: When should I stop my Dollar Cost Averaging plan?**

DCA is a wealth-building strategy, not a temporary tactic. Most investors continue their DCA plan until they reach their specific financial goal (like retirement or a house down payment). However, you should periodically review your portfolio to ensure the assets you are “averaging into” still align with your long-term thesis and the 2026 economic outlook.

—

Conclusion: The Path to Financial Resilience

As we look at the investment horizon for 2026 and beyond, it is clear that the most successful retail investors won’t be those who found the “next big thing” at exactly the right second. Instead, the victors will be those who exhibited the most discipline. Dollar Cost Averaging is more than just a mathematical formula; it is a commitment to consistency over chaos.

By minimizing emotional bias, reducing average cost basis, and leveraging the automated tools of the 2026 fintech landscape, you can build a portfolio that is resilient to the whims of the market. For the retail trader focused on minimizing costs and maximizing long-term gains, DCA remains the most potent weapon in their financial arsenal. Start small, stay consistent, and let the power of averaging do the heavy lifting for you in 2026.