Navigating Your Financial Journey: Understanding Average Net Worth by Age and How to Exceed It

In the intricate landscape of personal finance, few metrics offer as comprehensive a snapshot of an individual’s or household’s financial health as net worth. It’s a fundamental calculation that distills your entire financial life into a single number, representing the sum of everything you own minus everything you owe. For many, understanding where they stand relative to their peers—the elusive “average net worth by age”—becomes a compelling, albeit sometimes misleading, benchmark. At TradingCosts, we believe in empowering investors and financially savvy individuals with data-driven insights. This article delves deep into what net worth truly signifies, dissects the statistical averages and medians across different age groups, and critically, outlines robust strategies to not just meet, but significantly exceed these benchmarks. We’ll explore the multifaceted factors influencing wealth accumulation, from investment strategies to debt management, offering an expert perspective to guide your financial journey.

This article is for informational purposes only and does not constitute financial advice. Consult with a qualified financial professional before making any investment decisions.

What is Net Worth, Really? A Foundation for Financial Health

At its core, net worth is a simple equation: Assets – Liabilities = Net Worth. While the formula is straightforward, its implications are profound. It provides a holistic view of your financial standing at any given moment, acting as a critical barometer for measuring progress toward your financial goals, be it retirement, a major purchase, or financial independence.

Understanding Your Assets

Assets are anything of monetary value that you own. They can be broadly categorized as:

- Liquid Assets: Easily convertible to cash. This includes cash in checking accounts, savings accounts, money market accounts, and certificates of deposit (CDs).

- Investment Assets: Holdings designed to grow over time. This encompasses stocks, bonds, mutual funds, Exchange Traded Funds (ETFs), individual retirement accounts (IRAs), 401(k)s, 403(b)s, Roth accounts, and other brokerage accounts. The value of these assets fluctuates with market conditions.

- Real Estate: Your primary residence, vacation homes, and investment properties. While often a significant asset, it’s important to remember that the equity (market value minus outstanding mortgage) is what contributes to net worth.

- Personal Property: Valuables such as vehicles, jewelry, art, and other collectibles. For most, these are less liquid and often depreciate, so their inclusion in net worth calculations should be considered carefully, primarily focusing on items with significant, demonstrable market value.

- Business Interests: Ownership stakes in private businesses, which can be substantial but are often illiquid and require professional valuation.

Identifying Your Liabilities

Liabilities are financial obligations or debts that you owe to others. These typically include:

- Mortgages: The outstanding balance on your home loan.

- Student Loans: Both federal and private student debt.

- Auto Loans: Debts incurred to finance vehicle purchases.

- Credit Card Debt: Balances carried on credit cards, often characterized by high interest rates.

- Personal Loans: Unsecured loans from banks or other lenders.

- Other Debts: Medical bills, tax liabilities, or any other outstanding financial obligations.

Regularly calculating your net worth—we recommend at least quarterly or annually—allows you to track your financial trajectory. A rising net worth indicates positive financial momentum, while a stagnating or declining figure signals a need for strategic adjustments.

The Averages and Medians: A Statistical Snapshot by Age

When discussing “average” net worth, it’s crucial to distinguish between the mean and the median. The mean (average) is calculated by summing all net worths in a group and dividing by the number of individuals. The median, on the other hand, is the middle value when all net worths are arranged in ascending order. The median is often a more representative figure for the “typical” household because it is less skewed by extremely wealthy individuals who can significantly inflate the mean. For instance, a few billionaires in a dataset can dramatically increase the mean net worth for an entire age group, making it seem higher than what most people experience.

The gold standard for U.S. household financial data is the Federal Reserve’s Survey of Consumer Finances (SCF), conducted every three years. The most recent comprehensive data available is from the 2022 SCF, released in October 2023. Let’s examine the mean and median net worth across different age demographics:

| Age Group | Median Net Worth (2022 SCF) | Mean Net Worth (2022 SCF) |

|---|---|---|

| Under 35 | $40,600 | $183,500 |

| 35-44 | $219,400 | $549,300 |

| 45-54 | $370,100 | $1,180,900 |

| 55-64 | $577,300 | $1,739,700 |

| 65-74 | $665,900 | $1,987,100 |

| 75+ | $407,800 | $1,673,300 |

Source: Federal Reserve Survey of Consumer Finances, 2022

Observe the significant disparity between the median and mean net worth, particularly in older age groups. This stark difference underscores the concentration of wealth at the top. For example, a household in the 35-44 age bracket with a net worth of $219,400 is statistically “average” (median), while the mean for that group is more than double at $549,300. This highlights why solely chasing the “average” can be misleading; the median often provides a more realistic benchmark for the typical American household.

It’s also important to note that these figures represent snapshots in time and are influenced by prevailing economic conditions, inflation, and market performance. While these statistics offer a valuable context, they should serve as a guide, not a rigid target. Your personal financial journey is unique, shaped by a multitude of individual circumstances.

Beyond the Numbers: Factors Influencing Your Net Worth

While statistical averages provide a general framework, a myriad of individual factors profoundly influence one’s net worth trajectory. Understanding these drivers is key to formulating a personalized wealth accumulation strategy.

Income & Career Path

Your earning potential is arguably the most fundamental determinant of your ability to save and invest. Higher income generally provides more discretionary funds to allocate towards wealth-building. Factors like education level, chosen industry, geographic location, and career progression significantly impact income. Pursuing in-demand skills, negotiating salaries effectively, and seeking opportunities for professional growth can substantially boost your income over your working life.

Savings Rate

It’s not just how much you earn, but how much you save. A high savings rate—the percentage of your income you save or invest—is a powerful accelerator of net worth growth, especially when coupled with the magic of compounding. Even modest incomes can lead to substantial wealth over time if a disciplined savings rate is maintained. Aiming for a savings rate of 15-20% or more of your gross income is often recommended, but any increase makes a difference.

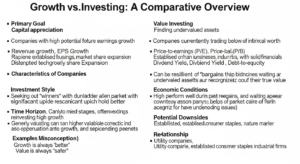

Investment Strategy & Risk Tolerance

Simply saving cash won’t keep pace with inflation. Investing is essential for long-term wealth creation. Your investment strategy, dictated by your risk tolerance and time horizon, plays a pivotal role:

- Asset Allocation: Deciding how to divide your investments among different asset classes like stocks, bonds, and real estate. Younger investors with a long time horizon often opt for a higher allocation to equities (stocks) due to their higher potential for growth, accepting greater short-term volatility. As one approaches retirement, a shift towards more conservative assets like bonds is common to preserve capital.

- Long-Term Investing: The stock market has historically delivered strong returns over the long run. The S&P 500, for instance, has generated an average annual return of approximately 10-12% (including dividends) over the past several decades, though past performance is not indicative of future results and significant volatility is inherent. Consistent investing, even through market downturns, allows you to benefit from dollar-cost averaging and compounding.

- Platform Choice: Utilizing low-cost, reputable brokerage platforms like Vanguard, Fidelity, and Charles Schwab is critical. These platforms offer a wide array of investment vehicles, including low-cost index funds and ETFs (e.g., VOO, SPY for S&P 500 exposure), which minimize expense ratios and maximize your returns.

- Risk Considerations: While investing is crucial, it comes with risks. Market risk (fluctuations in asset prices), inflation risk (erosion of purchasing power), and interest rate risk (impact on bond values) are ever-present. A diversified portfolio helps mitigate some of these risks.

Debt Management

Debt is a liability that directly reduces net worth. While “good debt” like a mortgage on an appreciating asset can be part of a wealth-building strategy, high-interest “bad debt” such as credit card balances can severely hinder progress. Strategically paying down high-interest debt frees up capital for saving and investing, accelerating net worth growth.

Geographic Location & Cost of Living

Where you live significantly impacts both your assets and liabilities. Housing costs vary dramatically by region, affecting the value of your primary residence (an asset) and the size of your mortgage (a liability). High cost-of-living areas also demand more income to maintain a certain lifestyle, potentially reducing your savings rate.

Major Life Events

Life events like marriage, having children, purchasing a home, starting a business, or experiencing a health crisis can have profound effects on net worth. While some events (e.g., homeownership) can boost assets, others (e.g., childcare costs, medical emergencies) can increase liabilities or reduce savings capacity. Proactive financial planning can help mitigate the negative impacts of unforeseen events.

Strategies for Accelerating Your Net Worth Growth

Building substantial net worth isn’t about luck; it’s about intentional, disciplined action. Here are expert-backed strategies to help you accelerate your wealth accumulation:

1. Maximize and Automate Savings

The cornerstone of wealth building is a high savings rate. Make saving automatic by setting up recurring transfers from your checking account to your savings and investment accounts. Prioritize contributions to tax-advantaged retirement accounts like 401(k)s (especially if your employer offers a match – it’s free money!), Traditional IRAs, and Roth IRAs. For 2024, the contribution limit for 401(k)s is $23,000 ($30,500 if 50 or older), and for IRAs, it’s $7,000 ($8,000 if 50 or older). Maxing out these accounts year after year is one of the most effective ways to build tax-efficient wealth.

2. Implement a Smart, Diversified Investment Strategy

Investing early and consistently is paramount due to the power of compounding. Choose a diversified portfolio that aligns with your risk tolerance and time horizon. For most long-term investors, a portfolio heavily weighted towards low-cost index funds or ETFs that track broad market indices like the S&P 500 (e.g., Vanguard’s VOO, iShares’ IVV, or SPDR’s SPY) or total stock market funds (e.g., Vanguard’s VTI) is highly effective. These funds offer instant diversification across hundreds or thousands of companies, reducing individual stock risk while capturing market returns.

- Minimize Fees: Be acutely aware of expense ratios. A difference of even 0.5% in fees can cost you tens or hundreds of thousands of dollars over a lifetime. Platforms like Vanguard, Fidelity, and Schwab are known for their low-cost offerings.

- Rebalance Regularly: Periodically adjust your portfolio back to your target asset allocation. For example, if stocks have outperformed, you might sell some stock funds and buy bond funds to restore your desired ratio.

- Tax Efficiency: Utilize strategies like tax-loss harvesting in taxable accounts and prioritize tax-advantaged accounts to minimize your tax burden on investment gains.

3. Aggressively Tackle High-Interest Debt

High-interest debt, such as credit card balances, can be a major drag on your net worth. The interest paid on these debts is essentially a guaranteed negative return on your money. Prioritize paying off these liabilities using strategies like the debt snowball (pay smallest balance first) or debt avalanche (pay highest interest rate first). Once eliminated, redirect those payments towards savings and investments.

4. Enhance Your Income Streams

While cutting expenses is important, increasing your income can have an even greater impact on your ability to save and invest. Consider:

- Skill Development: Invest in education, certifications, or training to increase your market value in your current career or pivot to a higher-paying field.

- Negotiation: Regularly negotiate your salary and benefits. Don’t underestimate your worth.

- Side Hustles: Explore opportunities to earn extra income outside your primary job, such as freelancing, consulting, or starting a small business.

5. Engage in Proactive Financial Planning

A well-defined financial plan provides a roadmap for your wealth journey. This includes setting clear financial goals, creating a budget, managing cash flow, and regularly reviewing your progress. Consider working with a Certified Financial Planner (CFP) who can provide personalized advice, help you navigate complex financial decisions, and ensure your strategy remains aligned with your evolving goals. Regular reviews (at least annually) of your net worth, budget, and investment performance are crucial to stay on track.

6. Strategic Real Estate Decisions

Your primary residence can be a significant asset, but it’s essential to view it strategically. While it provides shelter, it’s not always a pure investment. Consider the costs of ownership (property taxes, insurance, maintenance) versus potential appreciation. For some, investing in income-generating real estate (rental properties) can be a powerful way to diversify assets and create additional income streams, though it comes with its own set of risks and management responsibilities.

Common Pitfalls and How to Avoid Them

Even with the best intentions, many individuals fall prey to common financial missteps that impede net worth growth. Recognizing these pitfalls is the first step toward avoiding them.

1. Lifestyle Creep

As income increases, it’s natural to desire a higher standard of living. However, if your spending rises proportionally with your earnings, your savings rate stagnates, and your net worth growth slows or stops. This phenomenon, known as lifestyle creep, can be insidious. To combat it, commit to saving and investing a significant portion of every raise or bonus before adjusting your discretionary spending.

2. Ignoring Debt, Especially High-Interest Debt

Allowing high-interest debt, like credit card balances, to accumulate is a critical error. The compounding interest on these liabilities can quickly spiral out of control, making it incredibly difficult to build wealth. Prioritize paying off these debts aggressively. Consider debt consolidation or balance transfer options if appropriate, but only if you have a solid plan to avoid accumulating new debt.

3. Lack of an Emergency Fund

An insufficient emergency fund (typically 3-6 months of essential living expenses) leaves you vulnerable to financial shocks. Unexpected job loss, medical emergencies, or car repairs can force you to dip into investments or take on high-interest debt, derailing your financial plan. Build and maintain a robust emergency fund in a liquid, easily accessible account.

4. Market Timing and Panic Selling

Attempting to predict market movements (“market timing”) is a futile exercise for most investors and often leads to worse returns than a buy-and-hold strategy. Similarly, panic selling during market downturns locks in losses and prevents participation in the subsequent recovery. A long-term perspective, coupled with a diversified portfolio and a disciplined rebalancing strategy, is far more effective than reacting emotionally to market volatility.

5. High Investment Fees

Seemingly small investment fees can significantly erode your returns over decades. Expense ratios on mutual funds, advisory fees, and trading commissions all eat into your capital. Opt for low-cost index funds, ETFs, and consider robo-advisors or fee-only financial planners if you seek advice. Scrutinize every fee associated with your investments.

6. Insufficient Insurance Coverage

Unexpected catastrophic events—a major illness, disability, or premature death—can devastate a family’s finances and erase years of wealth building. Adequate health insurance, disability insurance, life insurance, and appropriate property/casualty insurance are not optional; they are fundamental layers of financial protection that safeguard your net worth and your family’s future.

Frequently Asked Questions About Net Worth

Q1: Is my primary residence included in my net worth calculation?

A: Yes, your primary residence is typically included as an asset in your net worth calculation. However, only the equity—the market value of your home minus any outstanding mortgage balance—contributes positively to your net worth. The mortgage itself is a liability that reduces your net worth. It’s important to use a realistic market valuation, not just what you paid for the home.

Q2: How often should I calculate my net worth?

A: We recommend calculating your net worth at least once a year, preferably quarterly. Regular tracking allows you to monitor your progress, identify trends, and make timely adjustments to your financial plan. Many personal finance apps and spreadsheets can automate this process by linking to your accounts, making it a quick and easy exercise.

Q3: What’s a “good” net worth for someone in their 30s/40s/50s?

A: While the median net worth figures from the Federal Reserve (e.g., $219,400 for 35-44, $370,100 for 45-54, $577,300 for 55-64) provide a statistical benchmark, what constitutes a “good” net worth is highly personal. It depends on your individual financial goals, income level, cost of living, and desired lifestyle. Rather than comparing yourself to averages, focus on setting your own realistic goals and consistently working towards them. A good net worth is one that is steadily growing and aligning with your long-term objectives.

Q4: Should I compare my net worth to others?

A: While it’s natural to be curious about how you stack up against others, excessive comparison can be detrimental. Everyone’s financial journey is unique, influenced by factors like education, career choices, family circumstances, and luck. Instead of comparing yourself to others, focus on your own progress and financial goals. Use the average and median figures as general context, but let your personal financial plan and objectives be your primary guide.

Q5: What’s the single most important factor in growing net worth?

A: There isn’t a single factor, but rather a synergistic combination of consistent saving, smart investing, and diligent debt management. However, if forced to choose one overarching principle, it would be consistency over time. Starting early and maintaining consistent contributions to diversified, low-cost investments, coupled with a commitment to living below your means, harnesses the power of compounding and is arguably the most powerful driver of long-term net worth growth.

Conclusion

Understanding “average net worth by age” offers a valuable statistical context, but it’s crucial to remember that these figures are merely benchmarks, not mandates. True financial health is a deeply personal journey, shaped by individual choices, circumstances, and strategic decisions. At TradingCosts, we advocate for a data-driven yet personalized approach to wealth accumulation.

By diligently tracking your net worth, implementing a disciplined savings rate, embracing a diversified, low-cost investment strategy, and proactively managing debt, you lay a robust foundation for financial prosperity. Avoid common pitfalls like lifestyle creep and market timing, and instead focus on consistent action and long-term vision. Whether you are just starting your career or nearing retirement, the principles of smart financial planning remain constant. Take control of your financial narrative, set your own ambitious goals, and equip yourself with the knowledge and tools to not just meet, but significantly exceed, the averages on your path to lasting financial independence.

“`json

{

“@context”: “https://schema.org”,

“@graph”: [

{

“@type”: “Article”,

“mainEntityOfPage”: {

“@type”: “WebPage”,

“@id”: “https://www.tradingcosts.com/blog/net-worth-by-age-what-is-average”

},

“headline”: “Navigating Your Financial Journey: Understanding Average Net Worth by Age and How to Exceed It”,

“image”: [

“https://www.tradingcosts.com/images/net-worth-by-age-hero.jpg”,

“https://www.tradingcosts.com/images/net-worth-by-age-graph.jpg”

],

“datePublished”: “2024-03-10T08:00:00+00:00”,

“dateModified”: “2024-03-10T08:00:00+00:00”,

“author”: {

“@type”: “Person”,

“name”: “TradingCosts Expert Team”

},

“publisher”: {

“@type”: “Organization”,

“name”: “TradingCosts”,

“logo”: {

“@type”: “ImageObject”,

“url”: “https://www.tradingcosts.com/logo.png”

}

},

“description”: “An expert guide to understanding average net worth by age, differentiating between mean and median, and providing actionable strategies to grow your wealth beyond statistical benchmarks. Includes data from the Federal Reserve’s Survey of Consumer Finances.”,

“articleSection”: [

“Personal Finance”,

“Wealth Management”,

“Investment Strategies”

],

“keywords”: “net worth by age, average net worth, median net worth, wealth accumulation, financial planning, investment strategies, personal finance, financial health, retirement planning, debt management”,

“wordCount”: “2100”

},

{

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “Is my primary residence included in my net worth calculation?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes, your primary residence is typically included as an asset in your net worth calculation. However, only the equity—the market value of your home minus any outstanding mortgage balance—contributes positively to your net worth. The mortgage itself is a liability that reduces your net worth. It’s important to use a realistic market valuation, not just what you paid for the home.”

}

},

{

“@type”: “Question”,

“name”: “How often should I calculate my net worth?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “We recommend calculating your net worth at least once a year, preferably quarterly. Regular tracking allows you to monitor your progress, identify trends, and make timely adjustments to your financial plan. Many personal finance apps and spreadsheets can automate this process by linking to your accounts, making it a quick and easy exercise.”

}

},

{

“@type”: “Question”,

“name”: “What’s a \”good\” net worth for someone in their 30s/40s/50s?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “While the median net worth figures from the Federal Reserve (e.g., $219,400 for 35-44, $370,100 for 45-54, $577,300 for 55-64) provide a statistical benchmark, what constitutes a \”good\” net worth is highly personal. It depends on your individual financial goals, income level, cost of living, and desired lifestyle. Rather than comparing yourself to averages, focus on setting your own realistic goals and consistently working towards them. A good net worth is one that is steadily growing and aligning with your long-term objectives.”

}

},

{

“@type”: “Question”,

“name”: “Should I compare my net worth to others?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “While it’s natural to be curious about how you stack up against others, excessive comparison can be detrimental. Everyone’s financial journey is unique, influenced by factors like education, career choices, family circumstances, and luck. Instead of comparing yourself to others, focus on your own progress and financial goals. Use the average and median figures as general context, but let your personal financial plan and objectives be your primary guide.”

}

},

{

“@type”: “Question”,

“name”: “What’s the single most important factor in growing net worth?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “There isn’t a single factor, but rather a synergistic combination of consistent saving, smart investing, and diligent debt management. However, if forced to choose one overarching principle,