The Definitive Guide to Dividend Investing for Sustainable Passive Income

In the pursuit of financial independence, few concepts captivate the imagination quite like passive income. The idea of money working for you, generating a steady stream of earnings without active daily effort, is a cornerstone of long-term wealth creation. Among the most reliable and time-tested strategies for achieving this is dividend investing. Far from being a niche strategy for retirees, dividend investing offers a powerful pathway for individual investors of all ages to build substantial wealth, generate consistent cash flow, and achieve financial security.

This comprehensive guide will demystify dividend investing, moving beyond the hype to provide a data-driven, practical roadmap. We’ll explore the mechanics of dividends, articulate their profound benefits, detail actionable strategies for building a robust dividend portfolio, and navigate the crucial tax considerations. Our aim is to equip you with the knowledge and confidence to leverage dividends as a cornerstone of your investing strategy, transforming your financial future with real insights and tangible steps.

Understanding the Foundation: What Are Dividends and How Do They Work?

At its core, a dividend is a distribution of a portion of a company’s earnings to its shareholders. When you own a share of stock, you own a tiny piece of that company. If the company is profitable and its board of directors decides to share those profits, they issue a dividend. This isn’t just a handout; it’s a strategic decision by management to return capital to investors, signal financial health, and often attract a specific type of investor.

Companies typically pay dividends for several reasons: to reward shareholders for their investment, to signal financial stability and confidence in future earnings, or because they have ample cash flow beyond what’s needed for reinvestment in the business. Mature companies in stable industries, such as utilities, consumer staples, and established technology firms, are often prolific dividend payers.

While cash dividends are the most common, companies can also issue stock dividends (additional shares) or special dividends (one-time payments, often after a particularly profitable period or asset sale). For the purpose of passive income, our focus will primarily be on recurring cash dividends.

Understanding the timeline of a dividend payment is crucial for investors:

- Declaration Date: The date on which a company’s board of directors announces its intention to pay a dividend, specifying the amount per share, the record date, and the payment date.

- Ex-Dividend Date: This is arguably the most important date for investors. To receive the dividend, you must purchase the stock before the ex-dividend date. If you buy on or after this date, the seller (who owned the shares before the ex-dividend date) will receive the dividend. The stock price typically drops by the dividend amount on the ex-dividend date to reflect that new buyers will not receive the upcoming payment.

- Record Date: The date on which the company’s transfer agent reviews its records to determine which shareholders are eligible to receive the dividend. You must be recorded as a shareholder on this date. Importantly, due to settlement periods (typically two business days for stock trades), the record date is usually one business day after the ex-dividend date.

- Payment Date: The actual date when the dividend is paid to eligible shareholders. This is when the cash hits your brokerage account.

For example, if a company declares a $0.50 per share dividend with an ex-dividend date of May 15, a record date of May 16, and a payment date of June 1. To receive the $0.50 dividend, an investor must purchase the stock by May 14. If purchased on May 15 or later, the dividend goes to the previous owner.

Two key metrics help evaluate dividend-paying stocks:

1. Dividend Yield: This expresses the annual dividend payment as a percentage of the current stock price. It’s calculated as:

Dividend Yield = (Annual Dividend Per Share / Current Share Price) * 100%

If a stock trades at $100 and pays a total of $3 per share in dividends annually, its dividend yield is 3%. A higher yield means more income relative to the stock’s price, but it’s crucial to assess its sustainability. The average dividend yield for the S&P 500 typically hovers between 1.5% and 2.0% in the current market environment, so anything significantly above that warrants closer inspection.

2. Dividend Payout Ratio: This metric indicates what percentage of a company’s earnings are paid out as dividends. It’s calculated as:

Dividend Payout Ratio = (Annual Dividends Per Share / Earnings Per Share) * 100%

A payout ratio between 30% and 70% is generally considered healthy for mature companies, suggesting they have enough earnings to cover the dividend and still reinvest in the business or manage debt. A payout ratio consistently above 80-90% can be a red flag, indicating the dividend might be unsustainable, especially if earnings decline. For certain industries like Real Estate Investment Trusts (REITs), which have specific tax structures, payout ratios can be higher (often 80-90% of Funds From Operations, or FFO, which is a better measure of their cash flow). Understanding these metrics forms the bedrock of intelligent dividend investing.

The Compelling Case for Dividend Investing: Beyond Just Income

While the allure of a regular income stream is the most obvious benefit, dividend investing offers a multi-faceted approach to wealth accumulation that extends far beyond just quarterly payouts. It’s a strategy rooted in financial prudence and long-term growth.

1. Consistent Passive Income Generation: This is the primary draw. Dividends provide a predictable cash flow that can supplement your active income, cover living expenses in retirement, or be reinvested to accelerate portfolio growth. Imagine a portfolio that consistently deposits cash into your account, whether the market is up or down. This income provides a tangible return on your investment, irrespective of daily market fluctuations.

2. Enhanced Total Return Potential: Dividends contribute significantly to an investor’s total return, which includes both capital appreciation (the increase in stock price) and dividend income. Historically, dividends have accounted for a substantial portion of the S&P 500’s total returns over long periods. Studies suggest that dividends have contributed approximately 40% of the total return of the S&P 500 over several decades. This means that focusing solely on capital gains misses a crucial component of market performance. Dividend-paying companies tend to be more established, financially stable, and less volatile, which can provide a cushion during market downturns.

3. A Natural Hedge Against Inflation: Many high-quality dividend-paying companies, particularly those with a history of increasing their payouts, can offer a degree of protection against inflation. As the cost of living rises, so too can the dividends paid by financially strong companies with pricing power. Companies that consistently grow their dividends often have robust business models that allow them to raise prices and increase earnings, thereby increasing their distributions to shareholders. This growth in income stream helps maintain purchasing power over time.

4. Compounding Power Through Reinvestment: This is where dividend investing truly shines for long-term investors. By reinvesting dividends—using the received cash to buy more shares of the same stock or other dividend-paying assets—you harness the power of compounding. Each new share purchased then generates its own dividends, which in turn can buy even more shares, creating an exponential growth effect. This process, often facilitated by Dividend Reinvestment Plans (DRIPs) offered by many companies and brokerages, allows your portfolio to grow faster than simply letting the cash sit idle.

Consider a hypothetical example: An investor puts $10,000 into a stock with a 3% dividend yield that pays annually. If they reinvest those dividends, and assuming the stock price and dividend yield remain constant (a simplification for illustrative purposes), after 10 years, their initial investment would have grown significantly more than if they had just collected the cash. For instance, with a 3% annual dividend reinvested, the initial $10,000 could grow to approximately $13,439 in value from reinvested dividends alone, generating $403 in annual income. Without reinvestment, the portfolio value would remain $10,000, generating $300 in annual income, demonstrating the powerful difference compounding makes over time.

5. Psychological Benefits and Financial Discipline: Receiving regular dividend payments can provide a powerful psychological boost, reinforcing the tangible benefits of long-term investing. It instills financial discipline, encouraging investors to focus on the underlying business health rather than short-term price fluctuations. The consistent income stream can also provide a sense of financial security, reducing anxiety during volatile market periods and supporting a more patient, strategic approach to wealth building.

Crafting Your Dividend Portfolio: Strategies and Selection Criteria

Building a robust dividend portfolio requires a thoughtful approach, balancing income needs with growth potential and risk management. There isn’t a one-size-fits-all strategy; instead, investors typically gravitate towards a few key approaches or a hybrid model.

Strategy 1: Dividend Growth Investing

This strategy focuses on companies that not only pay dividends but have a consistent track record of increasing their payouts over time. The emphasis here is less on the current yield and more on the growth rate of the dividend, which often signals a financially healthy, growing business with a durable competitive advantage.

- Characteristics: Look for companies with strong free cash flow, low debt levels, a reasonable payout ratio (e.g., 30-60%), and a history of robust earnings growth. These companies typically operate in stable, mature industries but possess specific competitive advantages (moats) that allow them to sustain profitability and dividend increases.

- Benchmarks: The “Dividend Aristocrats” (S&P 500 companies with 25+ consecutive years of dividend increases) and “Dividend Kings” (50+ consecutive years) are prime examples of this strategy in action. While these lists are not buy recommendations, they serve as excellent starting points for research, demonstrating the power of consistent dividend growth.

- Metrics to Focus On: Beyond dividend yield and payout ratio, analyze the 5-year and 10-year dividend growth rates. A company consistently growing its dividend by 5-10% annually can significantly enhance your income stream over time and often leads to strong capital appreciation as well.

Strategy 2: High Dividend Yield Investing

This approach targets companies offering an above-average current dividend yield, often appealing to investors seeking maximum immediate income. While tempting, this strategy requires careful due diligence to avoid “dividend traps.”

- Caution: A very high dividend yield (e.g., significantly above the S&P 500 average, say 5%+) can sometimes indicate that the market expects a dividend cut, or that the company is experiencing financial distress, causing its stock price to fall and thus artificially inflating the yield. This is a “dividend trap.”

- Metrics to Focus On: Scrutinize the payout ratio, debt-to-equity ratio, and free cash flow. A high yield is only sustainable if backed by strong, consistent earnings and healthy cash flow. Understand why the yield is high. Is it a mature, stable business that generates ample cash, or is it a struggling company whose stock price has plummeted?

- Sectors Often Associated: Real Estate Investment Trusts (REITs) and Utilities are known for their higher yields due to their business models and regulatory structures. However, they come with their own unique risks and tax implications.

Strategy 3: Hybrid Approach

Many investors find success by combining elements of both dividend growth and high yield strategies. This involves building a diversified portfolio with a core of stable dividend growth stocks for long-term appreciation and inflation protection, complemented by a smaller allocation to carefully vetted high-yield opportunities for enhanced current income.

Key Selection Criteria for All Dividend Strategies:

- Dividend History & Growth: Look for a consistent history of paying and, ideally, increasing dividends. A long streak of dividend increases (e.g., 10+ years) is a strong indicator of financial stability and management’s commitment to shareholders.

- Sustainable Payout Ratio: As discussed, aim for a healthy range (30-70% for most companies, 50-80% for REITs/Utilities) to ensure the dividend is well-covered by earnings and cash flow.

- Robust Financial Health:

- Free Cash Flow (FCF): This is paramount. Companies pay dividends from FCF, not just reported earnings. Positive and growing FCF is a strong signal.

- Debt Levels: High debt can jeopardize dividend safety, especially in rising interest rate environments. Look for manageable debt-to-equity ratios.

- Earnings Stability & Growth: Consistent earnings allow for consistent dividend payments and growth.

- Competitive Advantage (Economic Moat): Companies with strong moats (e.g., brand loyalty, patented technology, network effects, cost advantages) are more likely to maintain profitability and grow dividends over the long term.

- Industry & Economic Trends: Understand the industry the company operates in. Is it growing or declining? Are there disruptive threats? Invest in companies positioned to thrive in the future.

- Valuation: Even the best dividend stock can be a poor investment if you overpay. Compare the current dividend yield to its historical average. Evaluate traditional valuation metrics like Price-to-Earnings (P/E) ratio relative to industry peers and historical norms. A stock with an attractive dividend yield but an excessively high P/E might be overvalued.

By diligently applying these criteria, investors can construct a resilient dividend portfolio designed for both passive income and long-term wealth appreciation.

Building Your Dividend Income Stream: A Step-by-Step Guide

Transitioning from understanding dividend investing to actually building a functional income stream requires a systematic approach. Here’s a practical, step-by-step guide to help you construct and manage your dividend portfolio.

Step 1: Define Your Goals and Risk Tolerance

Before you invest a single dollar, clarify your objectives:

- Income Target: How much passive income do you aim to generate annually, monthly, or quarterly? Is it for current expenses, or purely for reinvestment?

- Timeline: Are you investing for 5, 10, 20+ years? Your timeline will influence your strategy (e.g., more dividend growth for longer horizons).

- Risk Tolerance: How comfortable are you with market volatility and potential capital fluctuations? While dividend stocks are generally less volatile, they are not immune to market downturns.

- Capital Available: How much capital do you have to initially invest, and how much can you contribute regularly?

Step 2: Research and Due Diligence – Finding the Right Stocks

This is the most critical phase. Leverage available tools and resources:

- Stock Screeners: Utilize free online screeners (e.g., Finviz, Yahoo Finance, Google Finance) or those provided by your brokerage (e.g., Fidelity, Schwab, Vanguard).

- Key Filters: Start with filters like market capitalization (e.g., >$10 billion for stability), dividend yield (e.g., 2-5% for a balanced approach), dividend payout ratio (e.g., 30-70%), dividend growth streak (e.g., 10+ years), and industry.

- Example Search: Filter for S&P 500 companies, dividend yield > 2.5%, payout ratio < 70%, 5-year dividend growth rate > 5%, and positive free cash flow. This will narrow down your options significantly.

- Financial Reports: Once you have a shortlist, dive into the company’s annual reports (10-K) and quarterly reports (10-Q). Pay close attention to the income statement, balance sheet, and cash flow statement. Look for trends in revenue, earnings per share (EPS), free cash flow, and debt.

- Investor Relations: Many companies provide detailed investor presentations and dividend histories on their investor relations websites.

- Financial News & Analysis: Read reputable financial news sources and analyst reports (with a critical eye) to understand the company’s competitive landscape and future prospects.

Step 3: Diversification – Spreading Your Risk

Never put all your eggs in one basket. Diversification is paramount to mitigate risk:

- Across Industries: Invest in companies from different sectors (e.g., utilities, consumer staples, healthcare, technology, industrials, financials). This reduces exposure to downturns in any single industry.

- Across Market Capitalizations: Include a mix of large-cap, mid-cap, and potentially some smaller-cap dividend payers, though smaller companies generally carry more risk.

- Across Dividend Strategies: Combine dividend growth stocks with some stable, higher-yielding companies (if carefully vetted) to achieve a balanced income and growth profile.

- Consider ETFs/Mutual Funds: For broad diversification and lower individual stock risk, consider dividend-focused Exchange Traded Funds (ETFs) or mutual funds. These funds hold baskets of dividend-paying stocks, automatically providing diversification. Examples include ETFs tracking Dividend Aristocrats or broad market dividend indices.

A hypothetical diversified portfolio might look something like: 25% Utilities (stable income), 20% Consumer Staples (defensive, consistent growth), 20% Healthcare (resilient, innovation), 15% Technology (growing dividends from cash-rich giants), 10% Industrials (cyclical, but strong cash flow), 10% REITs (higher yield, real estate exposure).

Step 4: Execute Your Trades and Manage Dividends

- Open a Brokerage Account: Choose a reputable online brokerage. Consider both taxable accounts and tax-advantaged accounts (see next section).

- Place Orders: Use limit orders to control the price you pay for shares.

- Dividend Reinvestment Plans (DRIPs): Most brokerages offer the option to automatically reinvest dividends back into the same stock or fund that paid them, often commission-free. This is a powerful tool for compounding wealth, especially for long-term investors not needing immediate income. If you need the income, simply opt to receive cash payouts.

Step 5: Monitor and Adjust – Ongoing Portfolio Management

Dividend investing is not a “set it and forget it” strategy. Regular monitoring is essential:

- Review Periodically: At least annually, or quarterly, review the fundamentals of the companies in your portfolio. Check their earnings reports, dividend announcements, and any significant news.

- Check Dividend Safety: Are payout ratios still sustainable? Is free cash flow healthy? Are there any signs of financial distress that could lead to a dividend cut?

- Rebalance as Needed: Over time, some holdings may grow disproportionately, or your risk tolerance might change. Rebalance your portfolio to maintain your desired asset allocation and risk profile. This might involve selling some outperforming stocks to buy more of underperforming ones, or simply directing new capital to areas that are underweight.

- Stay Informed: Keep abreast of broader economic trends and market conditions that could impact your holdings.

By following these steps, you can systematically build and manage a dividend portfolio that aligns with your financial goals and generates a reliable stream of passive income.

Tax Implications and Account Considerations

Understanding the tax implications of dividend income is just as crucial as selecting the right stocks. The type of dividend and the account in which it’s held can significantly impact your net returns.

Qualified vs. Non-Qualified Dividends

Dividends are generally categorized into two types for tax purposes:

- Qualified Dividends: These are typically paid by U.S. corporations and certain qualified foreign corporations, provided you meet specific holding period requirements (usually owning the stock for more than 60 days during the 121-day period beginning 60 days before the ex-dividend date). Qualified dividends are taxed at the lower long-term capital gains rates, which are often 0%, 15%, or 20% depending on your taxable income. This is a significant advantage.

- Non-Qualified (Ordinary) Dividends: These do not meet the IRS’s qualified dividend criteria and are taxed at your ordinary income tax rate, which can be considerably higher than capital gains rates. Examples include dividends from REITs (often taxed as ordinary income), Master Limited Partnerships (MLPs), and some foreign companies.

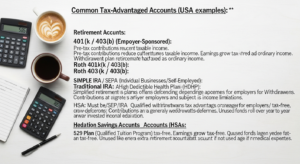

Tax-Advantaged Accounts: Maximizing Your Dividend Income

Strategic use of tax-advantaged accounts can significantly enhance the power of dividend investing:

- Roth IRA: This is an excellent vehicle for dividend growth stocks. Contributions are made with after-tax dollars, but all qualified withdrawals in retirement—including all dividend income and capital gains—are completely tax-free. This means your dividends compound and grow entirely tax-free, creating a powerful income stream for your later years.

- Traditional IRA / 401(k): Contributions are often tax-deductible, and your investments grow tax-deferred. Dividends received within these accounts are not taxed until you withdraw the funds in retirement, at which point they are taxed as ordinary income. While not as tax-efficient for dividends as a Roth IRA for distributions, the upfront tax deduction and tax-deferred growth are still highly beneficial.

- Health Savings Account (HSA): For those eligible, an HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. Investing dividends within an HSA allows them to compound tax-free, similar to a Roth IRA, but with the added benefit of tax-deductible contributions.

Taxable Brokerage Accounts

Dividends received in a standard brokerage account are subject to taxes in the year they are received. Qualified dividends will be taxed at the lower long-term capital gains rates, while non-qualified dividends will be taxed at your ordinary income rate. If you reinvest dividends in a taxable account, each reinvestment is considered a new purchase, and you will have to track the cost basis for future capital gains calculations. This is more complex than tax-advantaged accounts but offers flexibility and no withdrawal restrictions.

Special Considerations for REITs and MLPs

- REITs (Real Estate Investment Trusts): REITs are legally required to distribute at least 90% of their taxable income to shareholders annually. Because of this, most REIT dividends are typically taxed as ordinary income, not qualified dividends. This is an important distinction to consider when allocating REITs to your portfolio, often making them more suitable for tax-advantaged accounts.

- MLPs (Master Limited Partnerships): MLPs, common in the energy sector, have a unique tax structure. They don’t pay corporate income tax; instead, they pass through income and deductions to their unitholders. This means you receive a K-1 tax form instead of a 1099-DIV, which can complicate tax preparation. A significant portion of MLP distributions may be considered a “return of capital,” which reduces your cost basis and is not taxed until you sell your units.

Foreign Dividends

Dividends from foreign companies may be subject to withholding taxes by the source country. The U.S. has tax treaties with many countries to reduce or eliminate these withholding taxes. You may also be able to claim a foreign tax credit on your U.S. tax return for taxes paid to foreign governments, preventing double taxation. However, this adds a layer of complexity to tax filing.

Navigating these tax rules effectively can significantly enhance your net dividend income. Prioritizing tax-advantaged accounts for high-yielding or non-qualified dividend payers, and utilizing the favorable tax treatment of qualified dividends in taxable accounts, are key strategies for optimizing your dividend investing journey. Always consult with a qualified tax professional for personalized advice.

Frequently Asked Questions About Dividend Investing

Q: Is dividend investing only for retirees?

A: Absolutely not. While it’s excellent for retirees seeking income, dividend investing is highly effective for investors of all ages. Younger investors can leverage the power of compounding by reinvesting dividends, allowing their portfolios to grow exponentially over several decades. The consistent income stream can also provide financial flexibility at any stage of life, whether saving for a down payment, funding education, or accelerating retirement savings.

Q: What’s considered a “good” dividend yield?

A: A “good” dividend yield is subjective and depends on your investment strategy and risk tolerance. The average dividend yield for the S&P 500 typically hovers between 1.5% and 2.0% in the current market environment. A yield significantly higher than this (e.g., 5%+) warrants careful scrutiny, as it could signal underlying financial issues or an unsustainable payout (a “dividend trap”). For dividend growth investors, a moderate yield (e.g., 2-4%) combined with a strong history of dividend increases is often preferred. For income-focused investors, a yield above the market average is desirable, but always prioritize sustainability and financial health over just the raw percentage.

Q: How often are dividends paid?

A: Most companies listed on U.S. exchanges pay dividends quarterly. However, some companies pay monthly (e.g., certain REITs, BDCs, and ETFs), semi-annually, or even annually. A few companies may also issue special, one-time dividends. Understanding the payment frequency helps you plan your income stream.

Q: Should I reinvest my dividends (DRIP)?

A: For long-term growth and maximizing the power of compounding, especially during your accumulation phase, reinvesting dividends (DRIP) is highly recommended. By automatically using your dividend payouts to buy more shares, you accelerate the growth of your portfolio, leading to a larger income stream in the future. If you are in the distribution phase (e.g., retirement) and need the income to cover living expenses, then receiving cash payouts is appropriate. Your choice should align with your financial goals and current needs.