Your Definitive Guide to Net Worth: Calculation, Analysis, and Strategic Growth

In the complex landscape of personal finance, many metrics vie for your attention: income, cash flow, debt-to-income ratios. Yet, one stands paramount as the truest barometer of your long-term financial health and progress: your net worth. It’s more than just a number; it’s a dynamic snapshot of everything you own minus everything you owe, providing a clear, unbiased assessment of your wealth-building journey. At Trading Costs, we believe in numbers-backed insights and real strategies, not hype. This comprehensive guide will equip you with the precise tools and knowledge to accurately calculate your net worth, interpret what it means for your financial future, and implement specific, actionable strategies to grow it consistently and sustainably.

What is Net Worth and Why Does It Matter?

At its core, net worth is a simple equation:

Total Assets – Total Liabilities = Net Worth

An asset is anything you own that has monetary value, from the cash in your checking account to your investment portfolio and real estate. A liability is anything you owe, such as a mortgage, student loans, or credit card debt.

While seemingly straightforward, the significance of net worth extends far beyond its basic definition. It is the single most important metric for several critical reasons:

* True Measure of Financial Health: Unlike income, which only reflects how much money flows in, net worth shows how much wealth you’re actually accumulating. A high income with high spending and debt can result in a stagnant or even negative net worth.

* Progress Toward Financial Goals: Whether your goal is early retirement, financial independence, or buying a dream home, net worth is the ultimate scorecard. Tracking its growth (or decline) provides tangible evidence of your progress and helps you stay motivated.

* Informs Major Financial Decisions: Understanding your net worth helps you assess your capacity for major purchases, manage risk, and plan for future expenses. It provides the context needed to make informed choices about borrowing, investing, and spending.

* Identifies Areas for Improvement: A regular review of your assets and liabilities can highlight where your money is tied up, where you might be over-leveraged, or where you have opportunities to optimize your financial structure. For instance, a high proportion of non-liquid assets might signal a need for more accessible funds, while significant high-interest debt points to an immediate area for reduction.

In essence, net worth is your financial compass, guiding you toward your desired financial destination. Ignoring it is akin to sailing without a map.

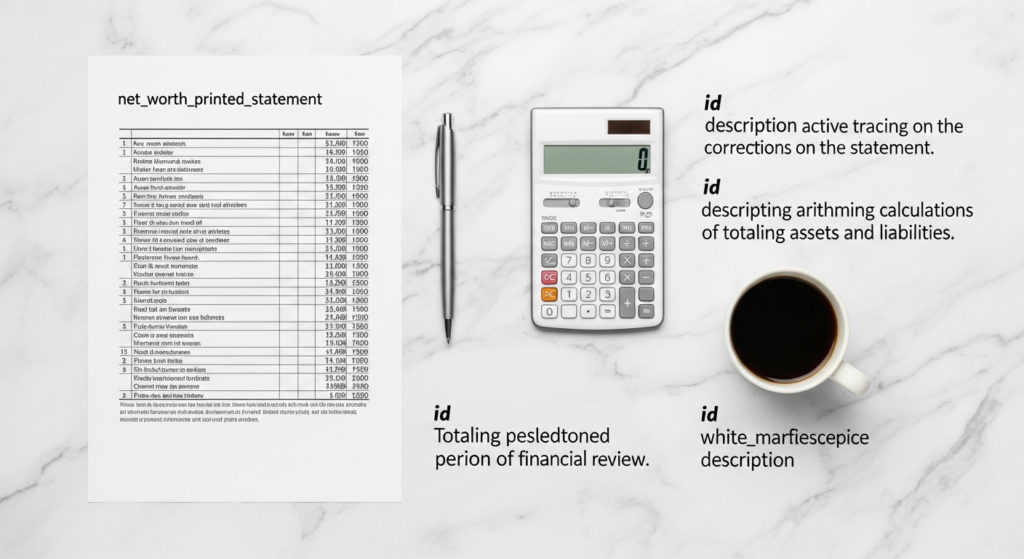

Step-by-Step Guide to Calculating Your Net Worth

Calculating your net worth is a foundational exercise in personal finance. It requires a systematic approach to ensure accuracy. Here’s how to do it:

Step 1: Inventory Your Assets

Gather documentation for all your financial accounts and assets. Be thorough, but also realistic about valuations.

* Liquid Assets (Cash & Equivalents):

* Checking accounts

* Savings accounts

* Money market accounts

* Certificates of Deposit (CDs)

* Physical cash (if significant)

Example:* $5,000 (checking) + $15,000 (savings) = $20,000

* Investment Assets:

* Brokerage accounts (stocks, bonds, mutual funds, ETFs)

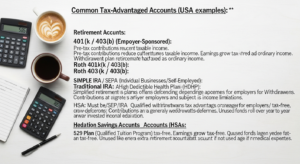

* Retirement accounts (401(k), 403(b), IRA, Roth IRA, SEP IRA, SIMPLE IRA)

* Health Savings Accounts (HSAs) with investment options

* Cryptocurrency holdings

* Education savings accounts (529 plans)

Example:* $150,000 (401k) + $40,000 (IRA) + $60,000 (brokerage) + $5,000 (crypto) = $255,000

* Real Estate:

Primary Residence: Use a conservative estimate of its current market value. This can be obtained from recent comparable sales, online valuation tools (like Zillow or Redfin), or a professional appraisal. Caution: While an asset, home equity is not liquid.*

* Investment Properties (rental homes, land): Market value.

Example:* $450,000 (primary residence) + $200,000 (rental property) = $650,000

* Personal Assets (with caveats):

* Vehicles: Use Kelley Blue Book or Edmunds for resale value.

Valuables (jewelry, art, collectibles): Only include if they have significant, easily convertible market value. For most personal items, their sentimental value far outweighs their financial contribution to net worth, and including them often inflates the true financial picture. For a conservative and actionable net worth calculation, it’s often best to exclude most personal possessions unless they are truly investment-grade assets.*

Example:* $25,000 (car)

* Business Interests:

* Value of your stake in a privately held business (requires professional valuation for accuracy).

Total Assets = Sum of all the above

Step 2: List Your Liabilities

Gather statements for all your outstanding debts.

* Mortgages:

* Primary residence mortgage balance

* Investment property mortgage balances

* Home Equity Lines of Credit (HELOCs)

Example:* $300,000 (primary mortgage) + $120,000 (rental mortgage) = $420,000

* Student Loans:

* Federal and private student loan balances

Example:* $80,000

* Auto Loans:

* Outstanding balances on vehicle loans

Example:* $15,000

* Credit Card Debt:

* Total outstanding balances across all credit cards

Example:* $10,000

* Personal Loans:

* Any unsecured personal loans

Example:* $5,000

* Other Debts:

* Medical bills, tax liabilities, payday loans, etc.

Total Liabilities = Sum of all the above

Step 3: Perform the Calculation

Once you have your totals, simply apply the formula:

Total Assets – Total Liabilities = Net Worth

Illustrative Example:

Let’s assume the examples listed above are for a single individual:

* Total Assets: $20,000 (liquid) + $255,000 (investments) + $650,000 (real estate) + $25,000 (car) = $950,000

* Total Liabilities: $420,000 (mortgages) + $80,000 (student loans) + $15,000 (auto loan) + $10,000 (credit cards) + $5,000 (personal loan) = $530,000

Net Worth = $950,000 – $530,000 = $420,000

Step 4: Regular Tracking and Reporting

Calculating your net worth once is a good start, but its true power lies in consistent tracking.

* Frequency: Aim to calculate it at least quarterly, or monthly if you’re actively managing debt or making significant investments.

* Method: Use a dedicated spreadsheet, a personal finance app, or a simple notebook. The consistency of the method is more important than the method itself.

* Review: Look for trends. Is your net worth growing? What factors are contributing to its changes? This regular review provides invaluable insights into the effectiveness of your financial strategies.

Interpreting Your Net Worth: Benchmarks and Context

Once you have your net worth number, the natural next question is: “Is it good?” The answer is nuanced, as “good” is subjective and highly dependent on individual circumstances, age, income, and goals. However, we can provide benchmarks and context to help you interpret your figure.

Benchmarking Your Net Worth

While direct comparisons can be misleading, general guidelines can offer a sense of perspective. Financial experts and studies (such as those from the Federal Reserve’s Survey of Consumer Finances, though we avoid specific years) often point to net worth as a multiple of income or by age.

* By Age and Income (General Guidelines, not rigid rules):

* Under 30: It’s common to have a low or even negative net worth, especially if you’re just starting your career, carrying student loan debt, or recently purchased a home. Aiming for 0.5 to 1 times your annual salary can be a solid initial goal.

* Age 30-40: As careers progress and incomes rise, net worth should begin to accelerate. Many financial planners suggest aiming for 1 to 3 times your annual salary by age 40. The focus should be on aggressive debt reduction (especially high-interest debt) and consistent investment.

* Age 40-50: This decade is often a period of significant wealth accumulation. Goals frequently range from 3 to 6 times your annual salary. Retirement savings become a major driver of net worth growth.

* Age 50-60+ (Pre-Retirement): Nearing retirement, net worth should ideally be substantial, potentially 6 to 10 times your annual salary, providing a buffer and income stream for your non-working years.

* The “Why” Behind the Numbers: These benchmarks are not mandates but rather common trajectories. They help you understand if you’re generally on track for typical financial goals. More importantly, they encourage self-reflection: Are your current savings and investment rates aligned with your long-term aspirations?

The Nuances of Net Worth

* Negative Net Worth: It’s not uncommon, especially for young professionals with significant student loan debt, or those who recently took on a mortgage. A negative net worth simply means your liabilities outweigh your assets. The goal is to move it into positive territory and then grow it aggressively.

* Home Equity: Your primary residence is typically your largest asset, but the equity tied up in it is not liquid cash. While it contributes to your total net worth, you can’t easily use it to cover daily expenses without selling or borrowing against it. For this reason, some analyses also consider “liquid net worth” (excluding primary residence equity and illiquid personal assets).

* Student Loan Debt as an Investment: While a liability, student loan debt can be viewed as an investment in human capital, potentially leading to higher earning potential over a lifetime. However, it still needs to be managed and paid down strategically.

* Net Worth Trajectory: Your net worth is rarely static. It will fluctuate with market performance, debt payments, and new savings. The key is to observe the trend over time; consistent upward movement is the goal.

Ultimately, your net worth is a personal metric. While benchmarks provide context, your individual financial goals and desired lifestyle should be the primary drivers of what constitutes a “good” net worth for you.

Strategic Pathways to Grow Your Net Worth

Growing your net worth is a journey that involves a combination of increasing assets, decreasing liabilities, and smart financial management. Here are specific, data-driven strategies to accelerate your wealth accumulation.

1. Increase Your Assets

This is the most direct path to boosting your net worth.

* Boost Your Savings Rate: The single most powerful lever you control. Aim to save and invest at least 15-20% of your gross income, or even more if you aspire to early financial independence. The higher your savings rate, the faster your net worth will grow.

Action:* Automate transfers to savings and investment accounts immediately after payday. Treat savings as a non-negotiable expense.

* Invest Wisely and Consistently:

* Harness Compounding: The “eighth wonder of the world,” compounding allows your investment earnings to generate more earnings. Start early and invest consistently.

* Diversification: Don’t put all your eggs in one basket. Invest across various asset classes (stocks, bonds, real estate) and geographies to mitigate risk.

* Low-Cost Index Funds and ETFs: For most individual investors, broad-market index funds (e.g., tracking the S&P 500) or diversified ETFs offer excellent returns with minimal fees. Historically, the S&P 500 has averaged around 10% annual returns over long periods, though past performance is not indicative of future results and market volatility is inherent.

* Max Out Tax-Advantaged Accounts: Prioritize contributions to 401(k)s, IRAs, Roth IRAs, and HSAs. These accounts offer significant tax benefits that accelerate growth. For example, a 401(k) match is free money – always contribute enough to get the full match.

* Automate Investments: Set up recurring investments to remove emotion from the process and ensure consistency (dollar-cost averaging).

Specific Data:* The “Rule of 72” estimates how long it takes for an investment to double. Divide 72 by your annual rate of return. At a 7.2% annual return, your money doubles every 10 years.

* Increase Your Income: More income provides more capital to save and invest.

* Career Advancement: Invest in skills, pursue promotions, negotiate salaries effectively.

* Side Hustles: Explore opportunities to generate additional income outside your primary job.

* Entrepreneurship: Starting a business, if successful, can significantly impact your net worth.

* Strategic Real Estate Appreciation:

* Primary Residence: While illiquid, a strategically purchased and maintained home can appreciate over time, building equity.

* Investment Properties: Rental properties can provide rental income and asset appreciation, though they come with management responsibilities and risk.

2. Reduce Your Liabilities

Attacking debt, especially high-interest debt, is a powerful way to improve your net worth.

* Aggressive Debt Management:

* Prioritize High-Interest Debt: Credit card debt and personal loans often carry interest rates of 15% or more. Paying these down is equivalent to a guaranteed, tax-free return on your money.

* Debt Avalanche vs. Snowball:

* Avalanche Method (Data-Driven): Pay down debts with the highest interest rates first, regardless of balance. This saves you the most money in interest over time.

* Snowball Method (Behavioral): Pay off the smallest balance first to gain psychological momentum.

Recommendation:* For maximum financial efficiency, the avalanche method is superior.

* Refinance Loans: If interest rates have dropped or your credit score has improved, consider refinancing mortgages, student loans, or auto loans to secure a lower interest rate and reduce your total interest paid.

* Avoid Unnecessary Debt: Be mindful of lifestyle inflation. As your income grows, resist the urge to immediately upgrade your lifestyle to match, especially through financing depreciating assets.

3. Optimize and Protect Your Wealth

Smart management and protection ensure your net worth continues to grow without unnecessary setbacks.

* Budgeting and Expense Tracking: You can’t manage what you don’t measure. Use a budget to understand where your money is going and identify areas for reduction, freeing up more funds for savings and investments.

Tools:* Spreadsheets, personal finance apps like Mint or YNAB (You Need A Budget).

* Tax Efficiency:

* Asset Location: Strategically place different asset types in specific account types (e.g., high-growth stocks in Roth accounts, bonds in tax-deferred accounts) to minimize taxes.

* Tax-Loss Harvesting: If you have investments in a taxable brokerage account, sell losing investments to offset capital gains and potentially up to $3,000 of ordinary income annually.

* Comprehensive Insurance: Protect your existing assets and future earning potential.

* Health insurance, auto insurance, home insurance, life insurance (especially if you have dependents), and disability insurance are crucial for preventing financial catastrophe that could decimate your net worth.

* Estate Planning: For those with substantial assets, a will, trusts, and other estate planning documents ensure your wealth is distributed according to your wishes and minimizes taxes for your heirs.

By consistently applying these strategies, you’ll not only see your net worth grow but also build a robust and resilient financial foundation for the future.

Tools and Technologies for Net Worth Management

In today’s digital age, a plethora of tools can simplify the process of tracking, analyzing, and growing your net worth. Leveraging these can provide clarity and automate much of the heavy lifting.

* Spreadsheets (Google Sheets, Microsoft Excel):

* Pros: Highly customizable, free (Google Sheets), offers complete control over data entry and calculations. You can design a net worth tracker exactly to your specifications.

* Cons: Requires manual input and updates for all accounts, which can be time-consuming.

* Best for: Detail-oriented individuals who prefer manual control and a deep understanding of each line item. Many templates are available online to get started.

* Financial Aggregation Apps (Empower (formerly Personal Capital), Mint, YNAB):

* Pros: Automatically link to your bank accounts, investment accounts, credit cards, and loans, providing a real-time, consolidated view of your net worth. They offer dashboards, budgeting tools, and investment analysis features. Empower, for instance, provides a detailed breakdown of your asset allocation and portfolio fees.

* Cons: Data privacy concerns (you’re linking all your financial accounts), occasional syncing issues, and sometimes less granular control than a custom spreadsheet. Free versions may contain ads.

* Best for: Individuals who want an automated, hands-off approach to tracking, with visual dashboards and quick insights.

* Brokerage and Retirement Account Dashboards:

* Pros: Most major investment platforms (e.g., Fidelity, Vanguard, Charles Schwab) offer robust dashboards that show the performance of your holdings with them. Some even allow you to link external accounts to provide a more holistic view of your net worth, albeit often limited to investment assets.

* Cons: Primarily focused on investment performance rather than a comprehensive net worth calculation that includes all liabilities.

* Best for: Monitoring investment growth and asset allocation within your primary investment ecosystem.

* Robo-Advisors (Betterment, Wealthfront):

Pros: While not primarily net worth trackers, robo-advisors are excellent for growing* the investment portion of your net worth. They offer automated, diversified portfolios tailored to your risk tolerance, with features like automatic rebalancing and tax-loss harvesting. This systematic approach contributes directly to asset accumulation.

* Cons: Fees are typically a percentage of assets under management (though lower than traditional advisors). Less suitable for those who prefer full control over individual stock picks.

* Best for: Hands-off investment management to consistently build your asset base.

* Professional Financial Advisors:

* Pros: For complex financial situations, high net worth individuals, or those needing comprehensive planning (e.g., retirement planning, estate planning, tax optimization), a fee-only certified financial planner (CFP) can be invaluable. They provide personalized advice, help you set and achieve goals, and can often identify opportunities you might miss.

* Cons: Can be expensive (either hourly, flat fee, or AUM-based). Requires finding a trustworthy and competent advisor.

* Best for: Comprehensive financial planning beyond just tracking, especially when dealing with significant assets, multiple income streams, or specific life events.

Choosing the right tools depends on your comfort level with technology, your desire for automation, and the complexity of your financial situation. The most effective approach often involves a combination – a primary tracking app complemented by a custom spreadsheet for deeper analysis or a robo-advisor for investment growth.

Frequently Asked Questions About Net Worth

Q1: Is my primary residence included in net worth?

Yes, your primary residence is an asset and should be included in your net worth calculation at its estimated market value. However, it’s crucial to also include the outstanding mortgage balance as a liability. While it contributes to your overall wealth, remember that home equity is largely illiquid; you can’t easily spend it without selling the property or taking out a loan against it.

Q2: What’s a “good” net worth?

A “good” net worth is highly subjective and depends on your age, income, lifestyle, and financial goals. There are general benchmarks (e.g., multiples of your income by certain ages), but ultimately, a good net worth is one that is consistently growing and aligns with your personal objectives, whether that’s early retirement, specific purchases, or leaving a legacy. Focus on your personal trajectory rather than direct comparison.

Q3: Can my net worth be negative? What does that mean?

Yes, your net worth can absolutely be negative, especially early in your career. This often happens due to student loans, car loans, or a new mortgage where liabilities exceed current assets. A negative net worth means you owe more than you own. It’s a common starting point for many, and the key is to develop a plan to reduce liabilities and accumulate assets to move into positive territory.

Q4: How often should I calculate my net worth?

For most individuals, calculating your net worth quarterly (every three months) is a good balance. This frequency allows you to see meaningful changes and trends without getting bogged down in daily or weekly fluctuations. If you’re actively paying down significant debt or undergoing major financial changes, monthly tracking might be more beneficial.

Q5: What’s the difference between net worth and liquid net worth?

Net worth includes all your assets (liquid and illiquid) minus all your liabilities. Liquid net worth, on the other hand, specifically measures your easily accessible assets (cash, savings, readily marketable investments) minus your total liabilities. It excludes illiquid assets like primary residence equity, personal vehicles, or private business interests. Liquid net worth provides a clearer picture of your immediate financial flexibility and emergency preparedness.

Conclusion: Your Net Worth as a Compass, Not Just a Scoreboard

Your net worth is far more than a static figure; it’s a dynamic compass guiding your financial journey. It provides an honest, data-driven assessment of your progress, revealing the effectiveness of your financial decisions and highlighting areas where strategic adjustments are needed. At Trading Costs, we advocate for this metric because it cuts through the noise, offering a tangible measure of your true wealth.

By systematically calculating your assets and liabilities, interpreting your standing against realistic benchmarks, and diligently implementing strategies to increase assets and reduce debt, you take decisive control of your financial destiny. Whether you’re starting with a negative net worth or already on the path to significant wealth, consistency and patience are your most valuable allies.

Don’t let this crucial metric remain an unknown. Start tracking your net worth today. Make it a regular habit, and watch how informed, numbers-backed action transforms your financial landscape. Your journey to financial independence begins with understanding where you stand, and your net worth is the clearest map you have.

“`json

{

“@context”: “https://schema.org”,

“@graph”: [

{

“@type”: “Article”,

“mainEntityOfPage”: {

“@type”: “WebPage”,

“@id”: “https://tradingcosts.com/net-worth-guide-calculate-grow/”

},

“headline”: “Your Definitive Guide to Net Worth: Calculation, Analysis, and Strategic Growth”,

“description”: “A comprehensive, authoritative guide for individual investors to understand, calculate, interpret, and strategically grow their net worth. Covers assets, liabilities, benchmarks, and actionable wealth-building strategies.”,

“image”: [

“https://tradingcosts.com/images/net-worth-guide-hero.jpg”,

“https://tradingcosts.com/images/net-worth-calculation-example.jpg”,

“https://tradingcosts.com/images/net-worth-growth-strategies.jpg”

],

“author”: {

“@type”: “Person”,

“name”: “Trading Costs Editorial Team”

},

“publisher”: {

“@type”: “Organization”,

“name”: “Trading Costs”,

“logo”: {

“@type”: “ImageObject”,

“url”: “https://tradingcosts.com/images/tradingcosts-logo.png”

}

},

“datePublished”: “2024-03-10”,

“dateModified”: “2024-03-10”,

“keywords”: “net worth, calculate net worth, grow net worth, financial health, assets, liabilities, wealth building, investing strategies, financial planning, personal finance, financial independence, debt management”,

“articleSection”: [

“What is Net Worth and Why Does It Matter?”,

“Step-by-Step Guide to Calculating Your Net Worth”,

“Interpreting Your Net Worth: Benchmarks and Context”,

“Strategic Pathways to Grow Your Net Worth”,

“Tools and Technologies for Net Worth Management”,

“Frequently Asked Questions About Net Worth”

]

},

{

“@type”: “FAQPage”,

“mainEntity”: [