Mastering Tax-Efficient Investing: Your Comprehensive Guide for 2026 and Beyond

In the intricate world of investing, one of the most persistent and often overlooked drains on your long-term wealth is taxes. While market fluctuations and investment choices grab headlines, the silent erosion caused by taxes can significantly diminish your compounding returns over decades. For individual investors and financially ambitious readers committed to building substantial wealth, understanding and implementing tax-efficient investing strategies is not merely an option—it’s a fundamental imperative. At Trading Costs, we believe in numbers-backed insights and real strategies, not hype. This comprehensive guide will equip you with the specific knowledge and actionable steps to optimize your portfolio for tax efficiency, ensuring more of your hard-earned money stays invested and continues to grow for 2026 and the years to come.

The Invisible Tax Drag: Understanding Its Impact

Imagine two identical investment portfolios, both earning an average annual return of 8% before taxes. If one portfolio is managed without regard for tax efficiency, incurring, say, a 2% annual tax drag on dividends, interest, and realized capital gains, its effective return drops to 6%. While a 2% difference might seem minor on a yearly basis, the cumulative impact over decades is staggering.

Consider an initial investment of $100,000:

- At an 8% annual return, it grows to approximately $466,096 in 20 years.

- At a 6% annual after-tax return, it grows to approximately $320,713 in 20 years.

That’s a difference of over $145,000—purely due to the “invisible tax drag.” Over 30 years, the disparity becomes even more pronounced. This illustrates why tax efficiency is not about avoiding taxes entirely, but strategically minimizing their impact to maximize your net returns.

Investment taxes primarily manifest in a few key areas:

- Capital Gains Tax: Levied on the profit from selling an investment. Short-term capital gains (assets held for one year or less) are taxed at your ordinary income tax rate, which can be as high as 37% for top earners. Long-term capital gains (assets held for more than one year) are typically taxed at preferential rates: 0%, 15%, or 20%, depending on your income bracket.

- Dividend Tax: Taxes on income paid out by companies. Qualified dividends (from eligible U.S. and some foreign corporations, held for a specified period) are taxed at the same preferential rates as long-term capital gains. Non-qualified dividends are taxed as ordinary income.

- Interest Income Tax: Interest from bonds, savings accounts, and CDs is generally taxed as ordinary income. Exceptions include municipal bond interest, which is often federally tax-exempt and sometimes state/local tax-exempt if issued in your state of residency.

Understanding these tax types is the first step toward building a robust tax-efficient investing strategy.

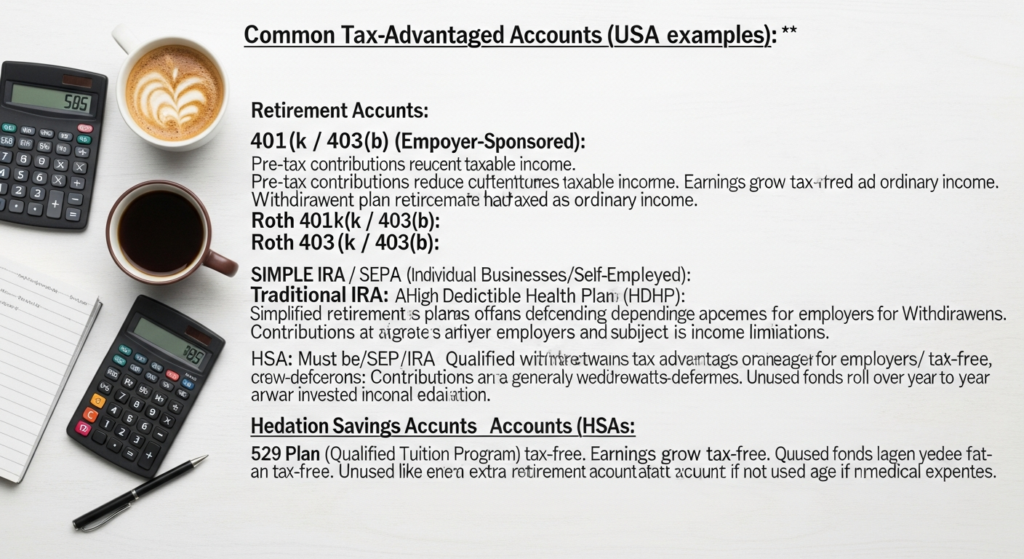

Leveraging Tax-Advantaged Accounts: Your First Line of Defense

The cornerstone of any tax-efficient investing strategy is maximizing the use of tax-advantaged accounts. These accounts, established by the government, offer specific tax benefits that allow your investments to grow more efficiently.

Employer-Sponsored Retirement Plans (401(k), 403(b), 457(b))

These plans are often your most powerful tool for tax-deferred growth.

- Pre-tax Contributions: Contributions are made with pre-tax dollars, reducing your current taxable income. Investments grow tax-deferred, meaning you don’t pay taxes until withdrawal in retirement. For 2024, the contribution limit for most 401(k) plans is $23,000, with an additional $7,500 catch-up contribution for those age 50 and over. Expect similar or slightly increased limits for 2026.

- Roth Contributions: Available in many employer plans, Roth contributions are made with after-tax dollars. While they don’t offer an upfront tax deduction, qualified withdrawals in retirement are entirely tax-free. This option is particularly attractive if you expect to be in a higher tax bracket in retirement.

- Employer Match: Don’t leave free money on the table. Many employers match a percentage of your contributions, which is an immediate, guaranteed return on your investment.

Action Step: Contribute at least enough to get the full employer match. Then, if possible, maximize your contributions up to the annual limit. Choose between pre-tax and Roth based on your current vs. anticipated future tax bracket.

Individual Retirement Accounts (IRAs)

IRAs offer flexibility and additional tax benefits beyond employer plans.

- Traditional IRA: Contributions may be tax-deductible, reducing your current taxable income. Earnings grow tax-deferred until withdrawal. For 2024, the contribution limit is $7,000, with an additional $1,000 catch-up contribution for those age 50 and over. Deductibility may be limited if you or your spouse are covered by an employer-sponsored retirement plan and your income exceeds certain thresholds.

- Roth IRA: Contributions are made with after-tax dollars, but qualified withdrawals in retirement are completely tax-free. Roth IRAs have income limitations for direct contributions. For 2024, the ability to contribute directly begins to phase out for single filers with a Modified Adjusted Gross Income (MAGI) of $146,000 and for married couples filing jointly at $230,000.

- Backdoor Roth IRA: If your income exceeds the Roth IRA contribution limits, you can still contribute to a Roth IRA through the “backdoor” strategy. This involves contributing non-deductible funds to a Traditional IRA and then immediately converting them to a Roth IRA. This strategy is particularly useful for high-income earners.

Action Step: Prioritize funding a Roth IRA if you expect your tax bracket to be higher in retirement. If your income is too high, explore the backdoor Roth IRA strategy.

Health Savings Accounts (HSAs)

Often hailed as the “triple-tax advantaged” account, HSAs offer unparalleled tax benefits for those enrolled in a high-deductible health plan (HDHP).

- Tax-Deductible Contributions: Contributions reduce your taxable income.

- Tax-Free Growth: Investments within the HSA grow tax-free.

- Tax-Free Withdrawals: Qualified withdrawals for eligible medical expenses are tax-free.

Unlike Flexible Spending Accounts (FSAs), HSA funds roll over year after year and can be invested. After age 65, HSA funds can be withdrawn for any purpose without penalty, though non-medical withdrawals are taxed as ordinary income.

For 2024, the individual contribution limit is $4,150, and the family limit is $8,300, with an additional $1,000 catch-up contribution for those age 55 and over. Expect similar or increased limits for 2026.

Action Step: If eligible, maximize your HSA contributions. Treat it as an investment vehicle for future medical expenses or even as an additional retirement account.

529 Plans

These plans are specifically designed for education savings.

- Tax-Free Growth & Withdrawals: Investments grow tax-free, and qualified withdrawals for education expenses are tax-free.

- State Tax Benefits: Many states offer a tax deduction or credit for contributions to their 529 plan, providing an immediate tax benefit.

Action Step: If saving for education, explore 529 plans, especially those offering state tax benefits.

Strategic Asset Location: Optimizing Where You Hold Investments

Once you’ve maximized contributions to tax-advantaged accounts, the next layer of tax efficiency comes from strategically deciding where to hold different types of investments. This is known as “asset location.” The goal is to place assets that generate the most tax-inefficient income (e.g., high-turnover funds, taxable bonds) into tax-advantaged accounts, and assets that are naturally more tax-efficient (e.g., broad-market index ETFs, municipal bonds) into taxable accounts.

Here’s a general framework for asset location:

Tax-Deferred Accounts (401(k), Traditional IRA):

These accounts shield your investments from annual taxation, deferring taxes until withdrawal. They are ideal for:

- High-Turnover Funds: Actively managed mutual funds that frequently buy and sell securities generate more short-term capital gains, which are taxed at ordinary income rates. Placing them here avoids immediate taxation.

- Taxable Bonds: Corporate bonds, U.S. Treasury bonds, and bond funds generate interest income, which is taxed as ordinary income. Holding them in tax-deferred accounts allows this income to compound without annual tax drag.

- Real Estate Investment Trusts (REITs): REITs often distribute non-qualified dividends, which are taxed at ordinary income rates. They are highly tax-inefficient in taxable accounts.

Tax-Free Accounts (Roth IRA, HSA):

These accounts offer the ultimate tax advantage: tax-free growth and tax-free withdrawals in retirement. They are best suited for:

- High-Growth Assets: Investments with the potential for substantial long-term appreciation, such as aggressive growth stocks or growth-oriented equity funds. The idea is to allow these assets to grow significantly and then withdraw the large gains completely tax-free in retirement.

- Assets Expected to Generate Significant Income: If you anticipate an investment will generate substantial dividends or interest, placing it in a Roth account ensures those distributions are never taxed.

Taxable Brokerage Accounts:

For investments held outside of tax-advantaged accounts, focus on strategies that minimize annual tax liability:

- Tax-Efficient Equity Funds: Broad-market index ETFs (e.g., S&P 500 ETFs) are generally very tax-efficient due to low turnover, low dividend yields, and the “in-kind” redemption mechanism that allows them to avoid realizing capital gains.

- Individual Stocks: For long-term investors, individual stocks held for more than a year generate long-term capital gains and potentially qualified dividends, both taxed at preferential rates.

- Municipal Bonds: Interest from municipal bonds is generally exempt from federal income tax, and often from state and local taxes if issued by a municipality in your state of residency. This makes them highly tax-efficient for taxable accounts, especially for high-income earners.

Example Scenario:

A common portfolio might include a mix of U.S. equities, international equities, and bonds.

- 401(k)/Traditional IRA: Hold taxable bond funds, REITs, and potentially actively managed funds.

- Roth IRA/HSA: Hold high-growth U.S. and international equity ETFs/funds.

- Taxable Brokerage Account: Hold broad-market U.S. equity ETFs (e.g., VOO, SPY, ITOT), international equity ETFs (e.g., VXUS, IXUS), and potentially municipal bond funds.

Studies, such as those by Vanguard, suggest that effective asset location can add an additional 0.15% to 0.75% to annual after-tax returns, a significant boost over decades.

Advanced Tax Management Techniques in Taxable Accounts

Even with optimal asset location, you’ll likely have investments in taxable brokerage accounts. Here are advanced strategies to further minimize tax drag.

Tax-Loss Harvesting

This powerful strategy involves selling investments at a loss to offset capital gains and potentially reduce your ordinary income.

- How it works: If you sell an investment for a loss, you can use that loss to offset any capital gains you realized during the year. If your capital losses exceed your capital gains, you can deduct up to $3,000 of the net loss against your ordinary income. Any remaining net loss can be carried forward indefinitely to offset future gains.

- The Wash-Sale Rule: To prevent abuse, the IRS has the “wash-sale rule.” You cannot claim a loss if you buy a “substantially identical” security within 30 days before or after the sale. To avoid this, you can buy a similar but not identical ETF (e.g., sell an S&P 500 ETF from Vanguard and buy one from iShares or Fidelity) or wait 31 days to repurchase the original security.

Action Step: Review your portfolio annually, especially towards year-end or during market downturns, for opportunities to harvest losses. Many robo-advisors (e.g., Wealthfront, Betterment) offer automated tax-loss harvesting.

Qualified vs. Non-Qualified Dividends

Be mindful of the type of dividends your investments generate.

- Qualified Dividends: Generally from U.S. corporations and certain qualified foreign corporations, held for more than 60 days during a 121-day period. These are taxed at the lower long-term capital gains rates.

- Non-Qualified Dividends: All other dividends, taxed at your ordinary income tax rate. REIT dividends are a common example of non-qualified dividends.

Action Step: In taxable accounts, favor investments that generate qualified dividends over non-qualified dividends where possible, or place non-qualified dividend generators in tax-deferred accounts.

Long-Term vs. Short-Term Capital Gains

The holding period of an asset significantly impacts its tax treatment.

- Long-Term Capital Gains: Assets held for more than one year are taxed at preferential rates (0%, 15%, or 20%).

- Short-Term Capital Gains: Assets held for one year or less are taxed at your ordinary income tax rate.

Action Step: Exercise patience. Avoid frequent trading in taxable accounts. Aim to hold investments for at least a year and a day to qualify for lower long-term capital gains rates.

Minimizing Portfolio Turnover and Expense Ratios

High turnover within a mutual fund leads to more realized capital gains, which are then passed on to you as taxable distributions, even if you don’t sell your shares. High expense ratios eat into your returns.

- Low-Cost Index Funds and ETFs: These are inherently tax-efficient due to their passive management style, low turnover, and often use of in-kind redemptions (especially ETFs). Their low expense ratios also maximize your net returns. Vanguard’s total stock market ETF (VTI) or an S&P 500 ETF (VOO) are prime examples.

Action Step: Prioritize low-cost, broad-market index funds and ETFs in your taxable accounts. Look for expense ratios below 0.10% for core holdings.

Charitable Giving Strategies

For charitably inclined investors, specific strategies can offer significant tax benefits.

- Donating Appreciated Securities: Instead of selling appreciated stock and donating the cash, donate the stock directly to a qualified charity. You avoid capital gains tax on the appreciation and can deduct the fair market value of the stock (up to certain limits).

- Donor-Advised Funds (DAFs): These allow you to make an irrevocable charitable contribution, receive an immediate tax deduction, and then recommend grants to charities over time. The assets grow tax-free within the DAF.

- Qualified Charitable Distributions (QCDs): If you are 70½ or older, you can make direct transfers of up to $105,000 (for 2024, subject to annual inflation adjustments) from your IRA directly to a qualified charity. This distribution counts towards your Required Minimum Distribution (RMD) but is excluded from your taxable income, which can be highly beneficial.

Action Step: Consult with a financial advisor to integrate charitable giving into your tax-efficient wealth plan, especially if you have highly appreciated assets or are nearing RMD age.

Building a Tax-Efficient Portfolio: A Step-by-Step Guide for 2026

Synthesizing these strategies into a cohesive plan can significantly enhance your long-term wealth. Here’s a practical, step-by-step approach:

Step 1: Maximize Tax-Advantaged Accounts

This is your foundational step. Prioritize contributions to:

- Employer-sponsored plans (401(k), 403(b), 457(b)) – especially to get the employer match, then up to the annual limit.

- Health Savings Account (HSA) – if eligible, due to its triple tax advantage.

- Individual Retirement Accounts (Traditional or Roth IRA) – up to the annual limit, considering your income and future tax bracket. Explore backdoor Roth if income-limited.

- 529 Plans – if saving for education, taking advantage of state tax benefits.

Step 2: Determine Your Overall Asset Allocation

Before deciding where to put specific investments, decide on your overall mix of stocks, bonds, and other assets based on your risk tolerance, time horizon, and financial goals. A common starting point might be 60% equities / 40% bonds, adjusted for individual circumstances.

Step 3: Implement Strategic Asset Location

With your asset allocation in mind, assign asset classes to the most appropriate account types:

- Roth IRA/HSA: High-growth equities, potentially specific individual stocks you expect significant appreciation from.

- 401(k)/Traditional IRA: Taxable bonds, REITs, high-turnover funds, and other assets generating ordinary income.

- Taxable Brokerage: Low-cost, broad-market equity index ETFs, municipal bonds (if suitable for your tax bracket), and individual stocks held for the long term.

Step 4: Select Tax-Efficient Investments within Each Account Type

Choose specific funds and securities that align with the tax characteristics of the account:

- In taxable accounts, favor ETFs over actively managed mutual funds for equities due to their tax efficiency and lower costs.

- For bonds in taxable accounts, consider municipal bonds. Otherwise, place taxable bond funds in tax-deferred accounts.

- Regularly review expense ratios and fund turnover.

Step 5: Practice Annual Tax-Loss Harvesting

Make it a routine to review your taxable portfolio for tax-loss harvesting opportunities, especially during market downturns or towards the end of the year. This can offset gains and reduce your taxable income. Be mindful of the wash-sale rule.

Step 6: Review and Adjust Regularly

Tax laws change, your financial situation evolves, and market conditions shift.

- Conduct an annual review of your portfolio’s tax efficiency.

- Rebalance your portfolio while considering tax implications (e.g., selling losers to offset gains, or rebalancing within tax-advantaged accounts).

- Stay informed about changes in tax legislation for 2026 and beyond.

Tools and Resources: Many brokerage firms (e.g., Fidelity, Vanguard, Charles Schwab) offer robust planning tools. Independent platforms like Empower (formerly Personal Capital) can help you track your net worth and analyze portfolio fees and tax efficiency. Consulting with a qualified fee-only financial advisor or a tax professional is highly recommended for complex situations or personalized guidance.

Frequently Asked Questions About Tax-Efficient Investing

Q1: Is a Roth IRA always better than a Traditional IRA?

A1: Not always. The choice depends on your current income tax bracket versus your expected tax bracket in retirement. If you expect to be in a higher tax bracket in retirement, a Roth IRA is generally better because you pay taxes now at a lower rate and withdraw tax-free later. If you expect to be in a lower tax bracket in retirement, a Traditional IRA might be better as you get a tax deduction now (at a higher rate) and pay taxes later (at a lower rate).

Q2: How often should I practice tax-loss harvesting?

A2: You can practice tax-loss harvesting at any time during the year, but many investors find it most effective to review their portfolios for opportunities towards the end of the year or during significant market downturns. It’s an annual strategy that can be deployed whenever losses are present.

Q3: What’s the biggest mistake individual investors make regarding investment taxes?

A3: The biggest mistake is often ignoring investment taxes altogether or failing to maximize contributions to tax-advantaged accounts. Many investors focus solely on gross returns without considering the net, after-tax returns, which is what truly impacts long-term wealth accumulation.

Q4: Are municipal bonds always completely tax-free?

A4: Interest from municipal bonds is generally exempt from federal income tax. However, whether it’s exempt from state and local taxes depends on your state of residency. If you buy a municipal bond issued by a municipality in your state of residence, it’s typically triple tax-exempt. If you buy an out-of-state municipal bond, it may still be subject to your state and local income taxes.

Q5: Can I invest in individual stocks within my Roth IRA or 401(k)?

A5: Yes, generally you can. Most self-directed retirement accounts (like IRAs, and many 401(k) plans if they offer a brokerage window) allow you to invest in a wide range of securities, including individual stocks, ETFs, and mutual funds. The key is to choose investments that align with the tax benefits of the account – for a Roth, high-growth stocks are ideal to maximize tax-free gains.

Conclusion

The journey to financial independence is paved with strategic decisions, and among the most impactful is the diligent pursuit of tax efficiency. By understanding the various forms of investment taxation, strategically leveraging tax-advantaged accounts, implementing thoughtful asset location, and employing advanced tax management techniques, you can significantly reduce the silent drag of taxes on your portfolio. For 2026 and beyond, these numbers-backed insights and real strategies are not just about compliance; they are about empowerment—empowering you to keep more of your hard-earned money, accelerate your wealth accumulation, and achieve your financial aspirations with greater certainty. Start implementing these strategies today, and watch your net worth grow more robustly over the long term.