The Essential 2026 Guide to Wealth Management for Beginners: Building Your Financial Foundation

Embarking on the journey of wealth creation can feel daunting, especially for those just starting out. The financial landscape is constantly evolving, and navigating its complexities requires a clear, strategic roadmap. This comprehensive guide, tailored for individual investors and financially ambitious readers, cuts through the noise to provide a practical, data-driven framework for effective wealth management in 2026 and beyond. This isn’t about quick riches or speculative ventures; it’s about establishing robust financial habits, understanding the core principles of growth and protection, and making informed decisions that compound over time. We’ll demystify the essential components of wealth management, offering actionable insights and specific strategies to help you build a durable financial foundation and achieve your long-term financial aspirations.

Understanding Wealth Management: More Than Just Investing

At its core, wealth management is a holistic, ongoing process of planning, organizing, and directing your financial resources to achieve specific life goals. For many beginners, “wealth management” is often conflated solely with “investing.” While investing is a critical component, true wealth management encompasses a much broader spectrum, including financial planning, risk management, tax efficiency, debt management, estate planning, and even behavioral finance.

Think of it this way: financial planning is like drawing the blueprint for your dream home, outlining where everything will go and how it will function. Wealth management, then, is the entire construction project – from laying the foundation and framing the structure to installing the plumbing and ensuring long-term maintenance. It’s a continuous process that adapts to your changing life circumstances, market conditions, and regulatory environments.

For beginners, understanding this distinction is crucial. You’re not just picking stocks; you’re orchestrating a symphony of financial decisions designed to protect and grow your assets. Starting early allows the powerful force of compound interest to work its magic over decades. Even modest, consistent contributions can accumulate into substantial wealth over 20, 30, or 40 years. For instance, a consistent $300 monthly investment yielding an average 8% annual return could grow to over $450,000 in 30 years, demonstrating the profound impact of time and consistency. Neglecting comprehensive wealth management means leaving significant potential on the table, exposing yourself to unnecessary risks, and potentially delaying your financial independence.

The Foundation: Budgeting, Debt Management, and Emergency Funds

Before you can effectively grow wealth, you must first master its management. This involves three fundamental pillars: disciplined budgeting, strategic debt elimination, and building a robust emergency fund. These steps are non-negotiable prerequisites for sustainable wealth creation.

Disciplined Budgeting: Knowing Where Your Money Goes

Budgeting isn’t about restriction; it’s about control and intentionality. A popular and effective method for beginners is the 50/30/20 rule:

- 50% for Needs: Essential expenses like housing, utilities, groceries, transportation, and minimum loan payments.

- 30% for Wants: Discretionary spending such as dining out, entertainment, hobbies, and subscriptions.

- 20% for Savings & Debt Repayment: This includes contributions to your emergency fund, retirement accounts, investment funds, and any debt payments above the minimum.

Alternatively, a zero-based budget assigns every dollar a purpose, ensuring no money is unaccounted for. Tools like Mint, YNAB (You Need A Budget), or even simple spreadsheets can help you track income and expenses, identify spending patterns, and adjust your habits. The goal is to gain clarity on your cash flow, ensuring you consistently live below your means and free up capital for savings and investments.

Strategic Debt Management: Eliminating High-Interest Liabilities

High-interest debt is a corrosive force on wealth accumulation. Credit card debt, for instance, often carries annual percentage rates (APRs) ranging from 20% to 30% or even higher. Carrying such debt means you’re effectively losing money faster than most investments can reliably gain it.

Prioritize eliminating high-interest debt using one of two popular strategies:

- Debt Avalanche: Pay off debts with the highest interest rates first, regardless of balance. This method is mathematically optimal, saving you the most money on interest.

- Debt Snowball: Pay off debts with the smallest balances first, regardless of interest rate, to build momentum and motivation.

For example, if you have a credit card with a 25% APR and a personal loan at 10% APR, the avalanche method dictates you aggressively tackle the credit card first. Refinancing high-interest debt into a lower-interest personal loan or balance transfer card can also be a viable strategy, provided you address the underlying spending habits.

The Emergency Fund: Your Financial Safety Net

Before significant investing, establish an emergency fund. This fund should cover 3 to 6 months of essential living expenses, kept in a separate, easily accessible, high-yield savings account (HYSA). As of 2026, many HYSAs offer competitive annual percentage yields (APYs) often in the 4-5% range, providing a modest return while keeping your capital liquid and secure. This fund acts as a crucial buffer against unexpected job loss, medical emergencies, or significant home/auto repairs, preventing you from incurring new debt or liquidating investments during market downturns.

Strategic Investing: Building Your Portfolio from Scratch

Once your financial foundation is solid, you can confidently transition to strategic investing. This phase focuses on growing your capital through carefully selected assets, aligned with your financial goals and risk tolerance.

Defining Your Investment Goals

Start with SMART goals:

- Specific: “Save for a down payment on a house.”

- Measurable: “Accumulate $50,000.”

- Achievable: “By saving $1,000 per month.”

- Relevant: “To buy a house in a desired area.”

- Time-bound: “Within 5 years.”

Whether it’s retirement, a down payment, or funding education, clear goals dictate your investment timeline and risk appetite.

Asset Allocation and Diversification Basics

Asset allocation is the strategy of dividing your investment portfolio among different asset categories, such as stocks, bonds, and cash. Diversification involves spreading your investments across various assets within each category to minimize risk.

A common rule of thumb for equity (stock) allocation is 110 minus your age. So, a 30-year-old might aim for 80% stocks and 20% bonds. This is a starting point; your actual allocation should reflect your personal risk tolerance and time horizon.

For beginners, diversification often means investing in low-cost index funds or Exchange Traded Funds (ETFs). These funds hold a basket of hundreds or thousands of individual stocks or bonds, providing instant diversification across entire markets or sectors. Examples include:

- S&P 500 Index Funds/ETFs: (e.g., VOO, SPY, IVV) track the performance of 500 large U.S. companies.

- Total Stock Market Index Funds/ETFs: (e.g., VTI, ITOT) provide exposure to the entire U.S. stock market, including small, mid, and large-cap companies.

- Total International Stock Market Index Funds/ETFs: (e.g., VXUS, IXUS) offer diversification into global markets.

- Total Bond Market Index Funds/ETFs: (e.g., BND, AGG) provide exposure to a broad range of U.S. investment-grade bonds.

These funds are characterized by extremely low expense ratios, often below 0.10% annually, which is critical for long-term returns.

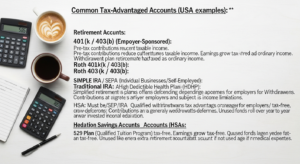

Investment Vehicles: Where to Invest

Prioritize tax-advantaged accounts first:

- Employer-Sponsored Retirement Plans (e.g., 401(k), 403(b)): If your employer offers a matching contribution, contribute at least enough to get the full match – it’s 100% immediate return on your investment. Contributions are often pre-tax, reducing your current taxable income. Current contribution limits are substantial (e.g., over $23,000 for employees in 2026, plus catch-up contributions for those 50 and older).

- Individual Retirement Accounts (IRAs):

- Traditional IRA: Contributions may be tax-deductible, and earnings grow tax-deferred until retirement.

- Roth IRA: Contributions are made with after-tax money, but qualified withdrawals in retirement are entirely tax-free. This is often preferred by beginners who anticipate being in a higher tax bracket later in life. Current contribution limits are around $7,000 for individuals in 2026, with income limitations for Roth eligibility.

- Health Savings Account (HSA): If you have a high-deductible health plan, an HSA offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. It can also function as a supplemental retirement account after age 65.

Once you’ve maximized these accounts, consider a taxable brokerage account for additional investments.

Dollar-Cost Averaging (DCA)

DCA involves investing a fixed amount of money at regular intervals (e.g., $200 every month), regardless of market fluctuations. This strategy reduces the risk of investing a large sum at an unfavorable time and removes emotion from your investment decisions. When prices are high, your fixed amount buys fewer shares; when prices are low, it buys more. Over time, this averages out your purchase price.

Assessing Your Risk Tolerance

Your risk tolerance is your ability and willingness to take on investment risk. A 25-year-old with a stable job and no dependents typically has a higher risk tolerance than a 55-year-old nearing retirement. Online questionnaires from brokerage firms can help you assess this, guiding your asset allocation choices.

Minimizing Drag: Taxes, Fees, and Inflation

Even with a solid investment strategy, your returns can be significantly eroded by three silent killers: taxes, fees, and inflation. Effective wealth management proactively addresses these factors.

Tax Efficiency

Understanding how taxes impact your investments is crucial.

- Prioritize Tax-Advantaged Accounts: As discussed, 401(k)s, IRAs (especially Roth), and HSAs offer significant tax benefits that should be fully utilized before investing in taxable accounts.

- Understand Capital Gains: When you sell an investment for a profit in a taxable account, you incur capital gains tax.

- Short-term capital gains (assets held for one year or less) are taxed at your ordinary income tax rate.

- Long-term capital gains (assets held for more than one year) are taxed at preferential rates, typically 0%, 15%, or 20% depending on your income bracket. This incentivizes long-term holding.

- Tax-Loss Harvesting: (More advanced, but good to know) In taxable accounts, you can sell investments at a loss to offset capital gains and potentially up to $3,000 of ordinary income annually.

Minimizing Fees

Fees, even small ones, compound over time to significantly reduce your total return.

- Expense Ratios: For mutual funds and ETFs, this is the annual fee charged as a percentage of your investment. Aim for funds with expense ratios below 0.10%. For example, an investment with a 1% annual fee over 30 years could reduce your total return by 25-30% compared to a fund with a 0.1% fee, assuming an 8% average annual return. Always check the expense ratio before investing.

- Trading Commissions: Most major brokerage firms now offer commission-free trading for stocks and ETFs, but be aware of potential fees for mutual funds or specific trading activities.

- Advisory Fees: If you hire a financial advisor, understand their fee structure (e.g., percentage of assets under management, hourly, flat fee). A good advisor can be worth their cost, but ensure transparency.

Combating Inflation

Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. If inflation averages 3% annually, the purchasing power of your money will halve in approximately 24 years. This means your investments must grow at a rate higher than inflation just to maintain their real value.

- Invest for Real Returns: Holding too much cash, especially in low-interest accounts, means your money is losing purchasing power over time. Investing in growth assets like stocks is crucial to generate returns that outpace inflation and grow your real wealth.

- Consider Inflation-Protected Securities: For a portion of your portfolio, Treasury Inflation-Protected Securities (TIPS) can offer protection against inflation, though they typically offer lower nominal returns.

Portfolio Rebalancing

Over time, market fluctuations will cause your asset allocation to drift from your target. Rebalancing involves periodically adjusting your portfolio back to your desired allocation (e.g., quarterly or annually). If stocks have performed exceptionally well, you might sell some stock funds and buy bond funds to restore your original balance, effectively “selling high and buying low” in a disciplined manner.

Protecting Your Wealth: Insurance and Estate Planning Basics

Wealth management isn’t just about accumulation; it’s also about protection. Safeguarding your assets and ensuring your wishes are met requires thoughtful consideration of insurance and basic estate planning.

Essential Insurance Coverage

Insurance acts as a financial safety net, mitigating the impact of unforeseen events that could otherwise devastate your financial plan.

- Health Insurance: Non-negotiable. Medical emergencies are a leading cause of bankruptcy. Ensure adequate coverage for yourself and your family.

- Disability Insurance: Protects your income if you become unable to work due to illness or injury. Your ability to earn is your greatest asset, especially for beginners.

- Life Insurance: If you have dependents (children, spouse, elderly parents), term life insurance provides a lump sum payment to your beneficiaries upon your death. Term life is generally recommended for its cost-effectiveness compared to whole life insurance for most individuals.

- Homeowner’s/Renter’s Insurance: Protects your dwelling and personal property from damage or theft, and provides liability coverage.

- Auto Insurance: Legally required in most places, protects against financial losses due to accidents.

Evaluate your needs annually and ensure your coverage is sufficient without being excessive.

Basic Estate Planning: Even for Beginners

Many assume estate planning is only for the wealthy or elderly, but even young adults with modest assets need basic protections.

- Will: A legal document outlining how your assets will be distributed and who will care for minor children upon your death. Without a will, state laws will dictate these matters, potentially contrary to your wishes.

- Durable Power of Attorney: Appoints someone to make financial decisions on your behalf if you become incapacitated.

- Healthcare Power of Attorney / Living Will: Appoints someone to make medical decisions and outlines your preferences for medical treatment if you cannot communicate them yourself.

These documents provide peace of mind and prevent potential legal and financial burdens for your loved ones during difficult times.

The Human Element: Behavioral Finance and Staying the Course

Even with the perfect strategy, human emotions can derail the best-laid plans. Behavioral finance studies the psychological influences on economic decision-making. For beginners, understanding and managing these biases is a critical component of long-term wealth management.

Avoiding Emotional Investing

Markets are inherently volatile. It’s common to feel fear during downturns and euphoria during upswings.

- Resist FOMO (Fear Of Missing Out): Chasing hot stocks or trends often leads to buying high. Stick to your diversified, long-term strategy.

- Avoid Panic Selling: Selling investments during a market crash locks in losses. History shows that markets typically recover, and patient investors are rewarded. Maintain a long-term perspective and remember your investment thesis.

A disciplined, rules-based approach (like dollar-cost averaging and regular rebalancing) helps to remove emotion from your decisions.

Discipline and Consistency

The most powerful force in wealth building is consistency.

- Automate Savings and Investments: Set up automatic transfers from your checking account to your savings and investment accounts on payday. This “pay yourself first” strategy ensures you’re consistently contributing, making it a habit rather than a choice.

- Review Periodically, Don’t Obsess: While it’s important to review your portfolio and financial plan annually, constantly checking market fluctuations or your account balance can lead to emotional decisions. Focus on your long-term goals.

Continuous Learning and Seeking Professional Advice

Financial literacy is an ongoing journey. Stay informed, read reputable financial publications, and continuously educate yourself. However, recognize when professional guidance is beneficial.

Consider a fiduciary financial advisor when:

- Your financial situation becomes complex (e.g., starting a business, inheritance, significant life changes).

- You need help staying disciplined or feel overwhelmed.

- You want a second opinion or specialized advice on topics like tax planning or estate strategies.

A fiduciary advisor is legally obligated to act in your best interest. Be wary of advisors who primarily earn commissions from selling specific products, as their incentives may not always align with yours.

Conclusion

Building wealth is a marathon, not a sprint. It demands discipline, patience, and a commitment to continuous learning. As a beginner in 2026, you have the incredible advantage of time on your side – the most powerful asset in wealth creation. By mastering budgeting, diligently managing debt, establishing an emergency fund, and strategically investing in a diversified, low-cost portfolio, you lay an unshakeable foundation for financial independence.

Remember to proactively address the “drags” of taxes, fees, and inflation, and protect your hard-earned assets with appropriate insurance and basic estate planning. Crucially, cultivate a disciplined mindset, resisting the emotional temptations of the market. This comprehensive, practical guide empowers you to take control of your financial future, transforming abstract goals into concrete achievements. Start today, stay consistent, and watch your wealth grow.