The Ultimate 401(k) Guide: Maximize Your Retirement Savings with Precision and Strategy

For individual investors and financially ambitious readers, the 401(k) isn’t merely an employee benefit; it’s a foundational pillar of long-term wealth accumulation and a powerful engine for achieving financial independence. Yet, despite its critical role, many participants navigate their 401(k) accounts with less than optimal strategy, leaving significant potential growth unrealized. At Trading Costs, we believe in numbers-backed insights and real strategies over vague advice. This comprehensive guide will dissect the mechanics of your 401(k), providing actionable, data-driven strategies to maximize your retirement savings, minimize frictional costs, and secure your financial future with precision.

Understanding Your 401(k) Fundamentals: More Than Just a Number

Before optimizing, we must first understand the core components of a 401(k). This employer-sponsored defined-contribution plan allows employees to save and invest for retirement on a tax-advantaged basis. Its structure offers distinct benefits that, when leveraged correctly, can significantly outperform taxable investment accounts.

Traditional vs. Roth 401(k): A Critical Distinction

The first fundamental choice often involves selecting between a traditional or Roth 401(k) if both are offered by your employer.

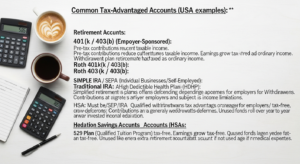

* Traditional 401(k): Contributions are made pre-tax, meaning they reduce your taxable income in the year they are made. Your investments grow tax-deferred, and you pay ordinary income tax on withdrawals in retirement. This is generally advantageous if you expect to be in a lower tax bracket in retirement than you are today.

* Roth 401(k): Contributions are made after-tax, meaning they do not reduce your current taxable income. However, qualified withdrawals in retirement are entirely tax-free. This is often preferred if you expect to be in a higher tax bracket in retirement or if you value the certainty of tax-free income later in life.

The choice between traditional and Roth depends heavily on your current income, anticipated future income, and overall tax strategy. For instance, a young professional early in their career, expecting higher income in the future, might find the Roth 401(k) more appealing due to the long runway for tax-free growth.

Contribution Limits and Catch-Up Provisions

The IRS sets annual limits on how much you can contribute to your 401(k). For the current year, the elective deferral limit is a significant figure that proactive savers should strive to meet. For instance, as of 2026, the anticipated standard contribution limit could be around $24,500. For individuals aged 50 and over, additional “catch-up” contributions are permitted, often adding an extra $8,000 to the annual limit, bringing their total potential contribution to $32,500 in our 2026 example. These limits are subject to inflation adjustments, so always verify the most current figures.

The Employer Match: Your First Priority for “Free Money”

Perhaps the most compelling immediate benefit of a 401(k) is the employer match. Many companies offer to contribute a certain percentage of your salary to your 401(k) if you contribute a minimum amount. A common structure might be a 50% match on the first 6% of your salary you contribute. This means if you earn $100,000 and contribute $6,000, your employer adds an extra $3,000 – a guaranteed 50% return on that portion of your contribution, immediately.

Data Point: A recent study indicated that approximately one-quarter of employees do not contribute enough to their 401(k) to receive the full employer match, effectively leaving “free money” on the table. Over a 30-year career, consistently missing out on a $3,000 annual match (assuming an average 7% annual return) could cost an individual over $280,000 in lost retirement savings. This single oversight is one of the costliest mistakes an investor can make.

Vesting Schedules: Understanding Ownership

Employer contributions, including the match, are often subject to a vesting schedule. This dictates when you gain full ownership of those funds.

* Cliff Vesting: You become 100% vested after a specific period (e.g., 3 years). If you leave before this period, you forfeit all employer contributions.

* Graded Vesting: You become gradually vested over time (e.g., 20% after 2 years, 40% after 3 years, etc., reaching 100% after 6 years).

Understanding your plan’s vesting schedule is crucial for career planning and evaluating job changes, as unvested funds are not yours to keep. Your own contributions are always 100% vested immediately.

Strategic Contributions: Hitting Your Maximum Potential

Guide: Maximize Your Retirement Savings with Precision and Strategy 11")

Maximizing your 401(k) isn’t just about opening an account; it’s about a disciplined, strategic approach to contributions that leverages compounding and tax advantages to their fullest.

Step 1: Always Secure the Full Employer Match

As highlighted, this is non-negotiable. If your employer offers a match, contribute at least the minimum required to receive every dollar. This is often the highest guaranteed return you’ll ever get on an investment. If you are contributing less than this threshold, prioritize increasing your contributions immediately.

Step 2: Strive for the IRS Maximum Contribution Limit

Once you’ve secured the match, your next goal should be to contribute the maximum allowed by the IRS, if financially feasible. The difference between contributing a percentage of your salary and hitting the absolute maximum can be astronomical over decades.

Example:

Consider two individuals, both starting at age 30, earning $80,000 annually, and achieving an average 7% annual return.

* Individual A: Contributes 10% of their salary ($8,000 annually), receiving a 50% match on the first 6% ($2,400). Total annual contribution: $10,400.

* Individual B: Contributes the maximum IRS limit (let’s use the 2026 example of $24,500), also receiving the $2,400 match. Total annual contribution: $26,900.

After 30 years, assuming a consistent 7% annual return:

* Individual A would have approximately $1,114,000.

* Individual B would have approximately $2,886,000.

This nearly $1.77 million difference illustrates the profound impact of maximizing contributions. It’s not just about saving more; it’s about giving more capital a longer runway to compound tax-deferred.

The Power of Dollar-Cost Averaging

By contributing a fixed amount from each paycheck, you are inherently practicing dollar-cost averaging. This strategy involves investing a consistent amount of money at regular intervals, regardless of market fluctuations. When prices are high, your fixed contribution buys fewer shares; when prices are low, it buys more. Over time, this averages out your purchase price, reduces risk from market timing, and can lead to superior long-term returns compared to trying to time the market. This disciplined approach is a cornerstone of effective 401(k) management.

Automate Your Increases

Many 401(k) plans allow you to set up automatic contribution increases, often called “auto-escalation.” This feature gradually increases your contribution rate by a small percentage (e.g., 1% annually) until you reach a predetermined cap or the IRS maximum. This “set it and forget it” approach makes increasing your savings effortless, aligning with behavioral finance principles to overcome inertia. Even a 1% annual increase can add up significantly over a 20-30 year career.

Investment Selection: Building a Robust Portfolio Within Your 401(k)

Contributing strategically is only half the battle; the other half involves intelligently investing those contributions. The investment options within a 401(k) plan are typically limited to a curated selection of mutual funds, exchange-traded funds (ETFs), or collective investment trusts (CITs). Your goal is to construct a diversified, low-cost portfolio that aligns with your risk tolerance and time horizon.

Understanding Your Fund Options

1. Target-Date Funds (TDFs): These are “fund of funds” that automatically adjust their asset allocation over time, becoming more conservative as you approach a specific retirement year (e.g., “2050 Target Date Fund”). TDFs are an excellent “set it and forget it” option for investors who prefer simplicity, but always scrutinize their underlying expense ratios and specific holdings.

2. Index Funds: These funds passively track a specific market index (e.g., S&P 500 index fund, total U.S. stock market index fund, total international stock market index fund, total bond market index fund). They are renowned for their low expense ratios and broad diversification. For many investors, a combination of 2-4 low-cost index funds can form the core of an exceptionally effective portfolio.

3. Actively Managed Funds: These funds are managed by professionals who attempt to outperform a specific benchmark index through active stock picking or market timing. While some active managers succeed in the short term, historical data consistently shows that the vast majority fail to beat their benchmarks over extended periods, especially after accounting for their higher fees.

Evaluating Expense Ratios: The Silent Wealth Eroder

The expense ratio is the annual fee charged by a fund, expressed as a percentage of your investment. This seemingly small number has a monumental impact on your long-term returns due to compounding.

Data Point: Consider two funds, both returning 7% annually before fees, over a 30-year period on an initial $100,000 investment.

* Fund A: Expense Ratio of 0.05% (e.g., a low-cost index fund).

* Fund B: Expense Ratio of 0.50% (e.g., a moderately priced actively managed fund).

After 30 years:

* Fund A would yield approximately $745,000.

* Fund B would yield approximately $657,000.

The seemingly small difference of 0.45% in fees costs the investor nearly $88,000 in lost wealth over three decades. This is a critical insight for any financially ambitious investor: lower fees directly translate to higher net returns over the long run. Always prioritize funds with the lowest expense ratios for a given asset class. Look for funds under 0.10% for broad market index funds.

Diversification and Asset Allocation

Your investment portfolio should be diversified across different asset classes (stocks, bonds), geographies (U.S., international), and market capitalizations (large-cap, mid-cap, small-cap). This reduces risk and provides smoother returns over time.

* Stocks (Equities): Offer higher potential returns but come with greater volatility. They are suitable for long-term growth.

* Bonds (Fixed Income): Offer lower returns but provide stability and income, acting as a buffer during stock market downturns.

Asset Allocation Strategies:

* Age-Based Rule of Thumb: A common guideline is to subtract your age from 110 or 120 to determine the percentage of your portfolio that should be in stocks. For a 30-year-old, this suggests 80-90% in stocks.

* Risk Tolerance: Your personal comfort level with market fluctuations should also guide your allocation. If significant market drops cause you undue stress, a more conservative allocation might be appropriate, even if it means slightly lower expected returns.

* Core-Satellite Approach: Many investors build a “core” portfolio of broad, low-cost index funds (e.g., 70% total U.S. stock, 30% total international stock) and then add “satellite” investments if they wish to express specific views or seek higher returns (e.g., a small allocation to a sector-specific ETF, though this is less common within 401k plans).

Rebalancing Your Portfolio

Over time, market movements will cause your asset allocation to drift from your target. Rebalancing involves selling appreciated assets and buying underperforming ones to restore your desired allocation. This is a disciplined way to “buy low and sell high” and manage risk. Most experts recommend rebalancing annually or when an asset class deviates by more than 5-10% from its target.

Minimizing Fees: The Silent Killer of Retirement Wealth

Guide: Maximize Your Retirement Savings with Precision and Strategy 12")

While investment selection is crucial, a deep understanding of all fees associated with your 401(k) is paramount for maximizing your net returns. High fees are a drag on performance that compounds relentlessly, eroding your wealth over decades.

Types of 401(k) Fees

1. Administrative Fees: These cover the costs of running the plan (recordkeeping, legal, accounting, compliance). They can be charged as a flat fee, a percentage of assets, or per participant.

2. Investment Management Fees (Expense Ratios): As discussed, these are embedded within the funds you choose and cover the costs of managing the underlying investments.

3. Transaction Fees: Less common in modern plans, but could include fees for buying/selling funds, transfers, or withdrawals.

The Cumulative Impact of High Fees

Let’s revisit the power of compounding, this time focusing on fees. If you have $250,000 in your 401(k) and are paying 1.5% in total annual fees versus a plan with 0.3% in total fees, that 1.2% difference might seem small. However, over 25 years with an average 7% annual return, the investor in the 1.5% fee plan would have $836,000, while the investor in the 0.3% fee plan would have $1,080,000. That’s a staggering $244,000 difference, purely due to fees.

How to Identify and Assess Fees

1. Summary Plan Description (SPD): Your employer is legally required to provide an SPD, which outlines plan rules, eligibility, and fee structures.

2. Fee Disclosures (404(a)(5) Notices): The Department of Labor mandates that plan administrators provide annual fee disclosures to participants. These documents detail administrative fees, individual transaction fees, and investment fund fees (expense ratios, trading costs within funds).

3. Fund Prospectuses: For each specific fund option, the prospectus (or summary prospectus) provides detailed information, including the expense ratio, management fees, and other charges.

4. Online Portal: Your 401(k) provider’s website often has a section detailing fees and fund performance.

Actionable Advice: Review these documents annually. Compare the expense ratios of your chosen funds to similar index funds available in the broader market (e.g., Vanguard, Fidelity, Schwab). If your 401(k) plan’s options are significantly more expensive, it’s a red flag.

Advocating for Lower-Cost Options

While individual employees typically can’t negotiate plan fees, collective action can be powerful. If your plan has consistently high fees and poor investment options, consider discussing it with your HR department or plan administrator. Employers have a fiduciary duty to offer a plan that is in the best interest of their employees, which includes reasonable fees. Many employers are unaware of how their plan’s fees compare to the market.

Consider Rollovers: If you leave a job, rolling over your old 401(k) into a low-cost IRA often provides access to a much wider array of low-cost investment options and greater control over fees. This is a powerful strategy to escape high-fee institutional plans.

Navigating Rollovers and Withdrawals: Protecting Your Nest Egg

Understanding how to manage your 401(k) when changing jobs or approaching retirement is critical to preserving its tax-advantaged status and avoiding costly penalties.

Rollover Options Upon Job Change

When you leave an employer, you typically have four options for your old 401(k):

1. Leave it with your old employer: This is often the path of least resistance but might mean retaining access to high-fee funds or a limited investment selection.

2. Roll it into your new employer’s 401(k): If your new plan has good investment options and reasonable fees, this can simplify your financial life by consolidating accounts.

3. Roll it into an Individual Retirement Account (IRA): This is often the most flexible option, providing access to a vast universe of low-cost funds and ETFs, along with greater control. You can open a Traditional IRA or a Roth IRA (though rolling a pre-tax 401(k) into a Roth IRA involves paying taxes on the conversion).

4. Cash it out: This is almost always the worst option. Cashing out before age 59 ½ will result in your withdrawal being taxed as ordinary income, plus a 10% early withdrawal penalty. You lose the tax-deferred growth and severely jeopardize your retirement savings.

Direct Rollover is Key: Always choose a “direct rollover” where funds are transferred directly from your old plan administrator to your new plan or IRA custodian. If you receive a check made out to you, you have 60 days to deposit it into a qualified retirement account, or it will be treated as a taxable distribution subject to taxes and penalties.

Understanding Withdrawal Rules and Penalties

* Age 59 ½ Rule: Generally, you can begin taking penalty-free withdrawals from your 401(k) after reaching age 59 ½. Withdrawals from a traditional 401(k) are taxed as ordinary income, while qualified withdrawals from a Roth 401(k) are tax-free.

* Required Minimum Distributions (RMDs): The IRS mandates that you begin taking withdrawals from traditional 401(k)s (and IRAs) once you reach a certain age, currently 73. RMDs ensure that the government eventually collects taxes on your tax-deferred savings. Failing to take RMDs results in a hefty 25% penalty on the amount you should have withdrawn. Roth 401(k)s, for the original owner, do not have RMDs until after death.

* Early Withdrawal Penalties: As mentioned, taking money out before 59 ½ typically incurs a 10% penalty on top of ordinary income taxes. There are limited exceptions (e.g., disability, certain medical expenses, qualified birth/adoption expenses), but these should be thoroughly researched and are generally not recommended for financial planning.

401(k) Loans vs. Hardship Withdrawals: Avoid If Possible

While some plans allow you to borrow from your 401(k) (up to 50% of your vested balance or $50,000, whichever is less), it’s generally ill-advised. You repay yourself with interest, but the money is removed from the market, missing out on potential growth. If you lose your job, the loan may become due immediately. Hardship withdrawals are even worse, as they typically trigger taxes and penalties, effectively dismantling your retirement savings. Exhaust all other options before considering these.

Advanced Strategies and Ongoing Management

For the financially ambitious, there are advanced strategies to further optimize your 401(k) and integrate it seamlessly into your broader financial plan.

The Roth 401(k) Advantage for High Earners

Beyond the standard Roth 401(k) contributions, some plans allow for “mega backdoor Roth” conversions. If your plan permits after-tax contributions (beyond the regular pre-tax or Roth limits) and in-service distributions or conversions, you can contribute additional after-tax money to your 401(k) and then immediately convert it to a Roth 401(k) or Roth IRA. This allows high-income earners, who may be phased out of direct Roth IRA contributions, to get substantial amounts of money into a Roth account, where it can grow and be withdrawn tax-free in retirement. This strategy requires careful planning and confirmation that your specific plan supports these features.

Periodically Review Your 401(k)

Your 401(k) is not a “set it and forget it” mechanism for your entire career. Regular reviews are essential:

* Annual Check-up: At least once a year, review your investment performance, current asset allocation, and the expense ratios of your chosen funds.

* Life Events: Reassess your strategy after significant life changes (marriage, children, new job, salary increase). Your risk tolerance, contribution capacity, and financial goals may shift.

* Plan Changes: Employers sometimes change 401(k) providers or update the fund lineup. Be aware of these changes and how they might impact your investment options and fees.

Integrate with Your Overall Financial Plan

Your 401(k) is one piece of your financial puzzle. Consider how it fits with other retirement accounts (IRAs, HSAs), taxable brokerage accounts, and your overall estate plan. A holistic view ensures that all your financial vehicles are working in concert towards your long-term objectives.

For instance, consider how your 401(k) contributions interact with your tax situation. If you’re in a high tax bracket, traditional 401(k) contributions offer immediate tax deductions. If you anticipate much higher income in retirement, Roth contributions might be more beneficial.

Utilizing Financial Advisors

While this guide provides comprehensive, actionable advice, complex financial situations or a desire for personalized guidance may warrant consulting a fee-only financial advisor. A qualified advisor can help with advanced tax planning, optimizing asset allocation across multiple accounts, and integrating your 401(k) with your broader wealth management strategy. Ensure any advisor you engage is a fiduciary, meaning they are legally obligated to act in your best financial interest.

Conclusion

The 401(k) stands as one of the most powerful tools for building substantial retirement wealth. Its tax advantages, coupled with the immense benefit of employer matching, create an unparalleled opportunity for financial growth. However, simply participating is not enough. Maximizing your 401(k) requires a strategic, data-driven approach: consistently maximizing contributions, meticulously selecting low-cost investments, diligently minimizing fees, and prudently managing rollovers and withdrawals.

By embracing these numbers-backed strategies and committing to ongoing review, you transform your 401(k) from a passive benefit into an active engine for your financial freedom. The difference between a passively managed, high-fee 401(k) and one actively optimized for costs and growth can literally be hundreds of thousands, if not millions, of dollars over a career. Take control of your retirement savings today – your future self will thank you.

Frequently Asked Questions About 401(k)s

Q: Can I have multiple 401(k)s?

A: Yes, you can have multiple 401(k) accounts, typically one for each employer you’ve worked for. However, the IRS contribution limits apply across all your 401(k) accounts combined in a given year. For example, if you change jobs mid-year, the total amount you contribute to both your old and new 401(k)s cannot exceed the annual limit.

Q: What happens to my 401(k) if I change jobs?

A: When you leave a job, you generally have four options: leave the money in your old 401(k) plan (if allowed), roll it over into your new employer’s 401(k), roll it over into an Individual Retirement Account (IRA), or cash it out. Cashing out is almost always discouraged due to taxes and penalties. Rolling it into an IRA often provides the most flexibility and control over investment options and fees.

Q: Should I borrow from my 401(k)?

A: Generally, borrowing from your 401(k) should be a last resort. While it allows you to access funds without immediate taxes or penalties and you pay interest back to yourself, the money is removed from the market and misses out on potential investment growth. If you lose your job, the loan may become due immediately, potentially leading to a taxable distribution and a 10% penalty if you can’t repay it.

Q: How do I know if my 401(k) fees are too high?

A: To assess your 401(k) fees, review your annual fee disclosure statements (404(a)(5) notices) and fund prospectuses. Compare the expense ratios of your chosen funds to low-cost index funds from providers like Vanguard, Fidelity, or Schwab, which often have expense ratios below 0.10%. If your total fees (administrative + investment management) exceed 0.50% to 1.00% annually, they are likely on the higher side and warrant investigation.

Q: What’s the difference between a traditional 401(k) and a Roth 401(k)?

A: The primary difference lies in their tax treatment. With a traditional 401(k), contributions are made pre-tax, reducing your current taxable income, and withdrawals in retirement are taxed. With a Roth 401(k), contributions are made after-tax, meaning no immediate tax deduction, but qualified withdrawals in retirement are entirely tax-free. The choice depends on whether you expect to be in a higher or lower tax bracket in retirement.

“`json

{

“@context”: “https://schema.org”,

“@graph”: [

{

“@type”: “Article”,

“mainEntityOfPage”: {

“@type”: “WebPage”,

“@id”: “https://www.tradingcosts.com/401k-guide-maximize-retirement-savings”

},

“headline”: “The Ultimate 401(k) Guide: Maximize Your Retirement Savings with Precision and Strategy”,

“description”: “A comprehensive, data-driven guide for individual investors on how to maximize 401(k) retirement savings through strategic contributions, optimized investment selection, fee minimization, and advanced planning.”,

“image”: “https://www.tradingcosts.com/images/401k-maximization-guide.jpg”,

“author”: {

“@type”: “Organization”,

“name”: “Trading Costs”

},

“publisher”: {

“@type”: “Organization”,

“name”: “Trading Costs”,

“logo”: {

“@type”: “ImageObject”,

“url”: “https://www.tradingcosts.com/logo.png”

}

},

“datePublished”: “2024-04-23T10:00:00Z”,

“dateModified”: “2024-04-23T10:00:00Z”,

“keywords”: “401k, retirement savings, maximize 401k, 401k guide, investment strategy, retirement planning, employer match, 401k fees, Roth 401k, 401k rollover, financial planning”,

“articleSection”: [

“Understanding Your 401(k) Fundamentals”,

“Strategic Contributions”,

“Investment Selection”,

“Minimizing Fees”,

“Navigating Rollovers and Withdrawals”,

“Advanced Strategies and Ongoing Management”

]

},

{

“@type”: “FAQPage”,

“mainEntity”: [

{

“@type”: “Question”,

“name”: “Can I have multiple 401(k)s?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “Yes, you can have multiple 401(k) accounts, typically one for each employer you’ve worked for. However, the IRS contribution limits apply across all your 401(k) accounts combined in a given year. For example, if you change jobs mid-year, the total amount you contribute to both your old and new 401(k)s cannot exceed the annual limit.”

}

},

{

“@type”: “Question”,

“name”: “What happens to my 401(k) if I change jobs?”,

“acceptedAnswer”: {

“@type”: “Answer”,

“text”: “When you leave a job, you generally have four options: leave the money in your old 401(k) plan (if allowed), roll it over into your new employer’s 401