The Definitive Guide to Early Retirement (FIRE Movement) by 2026: A Practical Blueprint for Financial Independence

The dream of ditching the daily grind decades before traditional retirement age isn’t just a fantasy; it’s a meticulously planned reality for a growing number of individuals. The Financial Independence, Retire Early (FIRE) movement offers a compelling framework for achieving this ambitious goal. It’s not about deprivation, but about intentional living, aggressive savings, and strategic investing to reclaim your time and design a life on your own terms. At Trading Costs, we believe in numbers-backed insights and real strategies. This comprehensive guide will strip away the hype and provide a practical, data-driven blueprint for pursuing FIRE, with a specific focus on the aggressive timeline of aiming for financial independence by 2026. Whether 2026 is your exact target or a motivational benchmark, the principles outlined here will equip you with the tools and knowledge to accelerate your journey towards financial freedom. Let’s dive into the specifics of how to build your FIRE foundation.

Understanding the FIRE Philosophy and Its Core Principles

At its heart, FIRE is more than simply stopping work; it’s about achieving a state where your passive income and investments are sufficient to cover your living expenses, thereby giving you the ultimate freedom: the option to work or not. This foundational concept redefines “retirement” from an age-based event to a financial milestone.

The Pillars of Financial Independence

The FIRE movement stands on three critical pillars, each demanding a conscious shift in financial behavior:

- High Savings Rate: This is the cornerstone. Unlike the average U.S. personal savings rate, which often hovers between 5% and 10% (according to data from the U.S. Bureau of Economic Analysis), FIRE adherents typically aim for 50%, 60%, or even 70% or more of their take-home pay. This isn’t just about accumulating money; it’s about drastically reducing your “financial runway” – the number of years your current expenses require you to work.

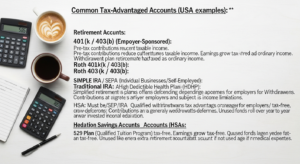

- Aggressive Investing: Saved money must be put to work. Idle cash erodes in value due to inflation. FIRE strategies emphasize investing these savings wisely, primarily in passive, low-cost index funds and Exchange-Traded Funds (ETFs), allowing the power of compounding to accelerate wealth growth.

- Lifestyle Optimization: This isn’t necessarily about extreme frugality, but about intentional spending and avoiding “lifestyle inflation.” It involves a deep understanding of what truly brings value to your life and cutting mercilessly from areas that don’t, thus minimizing your annual expenses both now and in retirement.

The 4% Rule and Your FIRE Number

The bedrock of safe withdrawal rates in early retirement planning is often attributed to the “Trinity Study,” which proposes the 4% rule. Based on historical market data (a diversified portfolio of stocks and bonds), the study suggests that withdrawing 4% of your initial portfolio value (adjusted for inflation annually) has a very high probability (historically over 95%) of lasting 30 years or more. For those planning a retirement that could span 40, 50, or even 60+ years, some FIRE practitioners opt for a more conservative withdrawal rate of 3.5% or even 3% to increase the margin of safety.

To apply this, you must calculate your “FIRE Number” – the total investment portfolio you need to accumulate.

Your FIRE Number = Annual Expenses / Safe Withdrawal Rate

For example, if your current annual expenses are $60,000 and you plan to use a 4% withdrawal rate, your target FIRE number would be:

$60,000 / 0.04 = $1,500,000

A critical insight here is that a higher savings rate creates a powerful double-whammy: you save more, and by living on less, you reduce your annual expenses, which in turn reduces your required FIRE number. This accelerates your timeline significantly.

Variations of the FIRE Movement

The FIRE philosophy isn’t monolithic; it has evolved into several sub-movements, each with a slightly different approach:

- LeanFIRE: Focuses on extreme frugality, targeting a lower FIRE number (e.g., annual expenses under $40,000).

- FatFIRE: Aims for a luxurious or high-spending retirement, requiring a significantly larger nest egg (e.g., annual expenses $100,000+).

- BaristaFIRE: Achieves financial independence but works part-time, often for benefits like health insurance or simply for enjoyment and supplemental income.

- CoastFIRE: Involves saving and investing a substantial amount early in your career, then allowing those investments to grow passively to cover traditional retirement without further contributions, freeing you to pursue less stressful or lower-paying work.

- REFIRE: (Real Estate FIRE) Focuses on building wealth through real estate investments to generate passive income.

Understanding these variations helps you tailor the FIRE principles to your personal aspirations and comfort level, ensuring your journey is sustainable and aligned with your values.

Phase 1: Turbocharging Your Income and Savings Rate

by 2026: A Practical Blueprint for Financial Independence 6")

Achieving FIRE by 2026 requires an aggressive approach to both earning and saving. This phase is about maximizing the input side of your financial equation.

Maximizing Income – The Fuel for Your FIRE Engine

While cutting expenses is vital, there’s a limit to how much you can cut. There’s virtually no limit to how much you can earn.

- Career Advancement & Negotiation: Don’t passively wait for raises. Proactively seek promotions, acquire high-demand skills, and negotiate aggressively for higher salaries. Data from various labor market analyses consistently shows that individuals who periodically switch jobs (e.g., every 2-4 years) often experience significantly higher salary growth (e.g., 8-15% per move) compared to those who remain with a single employer for extended periods. Document your achievements and market value.

- Side Hustles & Gig Economy: Leverage existing skills or learn new ones to generate additional income outside your primary job. This extra income, ideally, should go directly into savings and investments.

- Freelancing: Writing, graphic design, coding, virtual assistance, consulting in your area of expertise. Platforms like Upwork or Fiverr can connect you with clients.

- Gig Work: Food delivery (DoorDash, Uber Eats), ride-sharing (Uber, Lyft), task services (TaskRabbit).

- Online Businesses: E-commerce (Etsy, Shopify), blogging, creating digital products