How to Start Investing in Stocks: Your Definitive Guide for 2026

The journey to financial independence often begins with a single, crucial step: investing. For many, the stock market represents the most powerful engine for long-term wealth creation, a testament to the compounding returns it has historically delivered. However, the sheer volume of information, coupled with the inherent volatility of markets, can make starting seem daunting. You might be asking: “Where do I even begin?” or “Is 2026 the right time to dive in?”

At Trading Costs, we believe in numbers-backed insights, real strategies, and no-hype guidance. This comprehensive guide is designed to cut through the noise, providing individual investors and financially ambitious readers with a practical, step-by-step roadmap to confidently start investing in stocks in 2026 and beyond. We’ll demystify the process, equip you with the knowledge to make informed decisions, and lay the groundwork for a robust, long-term investment strategy.

Laying the Foundation: Financial Prerequisites Before You Buy Your First Stock

Before you commit a single dollar to the stock market, it’s imperative to ensure your personal financial house is in order. Investing with shaky foundations can turn potential gains into significant stress or even financial setbacks. This isn’t just conservative advice; it’s a data-driven strategy to protect your investments and provide peace of mind.

Build an Emergency Fund

Your emergency fund is your financial safety net, designed to cover unexpected expenses without forcing you to sell investments at an inopportune time. Imagine needing immediate cash for a car repair or a medical emergency; without an emergency fund, you might be forced to liquidate stocks during a market downturn, locking in losses. Financial experts universally recommend holding 3 to 6 months’ worth of essential living expenses in an easily accessible, liquid account, such as a high-yield savings account. For example, if your monthly expenses are $3,000, aim for $9,000 to $18,000 in your emergency fund.

Eliminate High-Interest Debt

The guaranteed return on investment (ROI) from eliminating high-interest debt often far surpasses the historical average returns of the stock market. Consider credit card debt, which frequently carries Annual Percentage Rates (APRs) ranging from 18% to 25% or even higher. The S&P 500, a common benchmark for stock market performance, has historically delivered an average annual return of approximately 10% over the long term. Paying off debt with an 18% interest rate is equivalent to earning a guaranteed, risk-free 18% return on your money – a return that’s nearly double what you might expect from stocks. Prioritize paying off credit cards, personal loans, and any other debt with rates exceeding 6-7% before actively investing in the market.

Understand Your Financial Goals

Your investment strategy should be a direct reflection of your financial goals. Are you saving for a down payment on a house in three years? Retirement in thirty years? Your timeline dictates your risk tolerance and asset allocation. Short-term goals (under 5 years) typically warrant lower-risk investments, often leaning towards cash or bonds, to preserve capital. Long-term goals (10+ years) allow for a greater allocation to stocks, leveraging their higher growth potential over time. Clearly defining these goals will help you select appropriate investment vehicles and manage expectations.

Define Your Risk Tolerance

Risk tolerance is your psychological comfort level with potential investment losses. It’s a critical factor in determining your asset allocation – the mix of stocks, bonds, and cash in your portfolio. A higher risk tolerance might mean a portfolio heavily weighted towards stocks, while a lower tolerance might favor a more conservative mix with a larger bond component. Be honest with yourself. While growth is desirable, an overly aggressive portfolio that causes you sleepless nights or prompts panic selling during downturns is counterproductive. Many brokerage firms offer questionnaires to help assess your risk tolerance, providing a data-backed starting point for your portfolio construction.

Understanding the Core Investment Vehicles: Beyond Individual Stocks

While the focus is on “starting to invest in stocks,” for most beginners, direct investment in individual company stocks is not the optimal starting point. Diversified funds, which offer exposure to many stocks at once, provide a more robust and less risky entry into the market.

Individual Stocks

- What they are: Shares of ownership in a single public company (e.g., Apple, Tesla, Coca-Cola).

- Pros:

- Highest potential for concentrated returns if you pick a winning stock.

- Direct ownership and ability to research specific companies you believe in.

- Excitement and engagement for those who enjoy in-depth company analysis.

- Cons:

- High risk: A single company’s performance can significantly impact your portfolio. Company-specific events (bad earnings, scandal, new competition) can lead to substantial losses.

- Requires significant research: Successfully picking individual stocks demands extensive due diligence, financial analysis, and ongoing monitoring. Data consistently shows that most active managers, despite their resources, underperform broad market benchmarks over the long term.

- Concentration risk: Lack of diversification exposes you to greater volatility.

Exchange-Traded Funds (ETFs)

- What they are: A type of investment fund that holds a collection of underlying assets (like stocks, bonds, or commodities) and trades on stock exchanges like individual stocks.

- Pros:

- Instant diversification: A single ETF can give you exposure to hundreds or thousands of companies. For example, an S&P 500 ETF holds shares in the 500 largest U.S. companies.

- Low expense ratios: ETFs are typically passively managed, resulting in very low annual fees. Broad market ETFs often have expense ratios as low as 0.03% to 0.09% (meaning you pay $3 to $9 annually for every $10,000 invested). This minimal fee significantly impacts long-term returns compared to higher-cost alternatives.

- Liquidity: You can buy and sell ETFs throughout the trading day, just like individual stocks.

- Tax efficiency: Often more tax-efficient than traditional mutual funds due to their structure.

- Examples:

- S&P 500 ETFs: VOO (Vanguard S&P 500 ETF), IVV (iShares Core S&P 500), SPY (SPDR S&P 500 ETF Trust). These track the performance of the 500 largest U.S. companies.

- Total Stock Market ETFs: VTI (Vanguard Total Stock Market ETF). This provides exposure to virtually every publicly traded U.S. company, large and small.

- International Market ETFs: VXUS (Vanguard Total International Stock ETF). Essential for global diversification.

Mutual Funds

- What they are: A professionally managed portfolio of stocks, bonds, or other investments, funded by multiple investors. When you invest, you buy shares in the fund, and your money is pooled with others to buy a diversified portfolio.

- Pros:

- Diversification: Similar to ETFs, they offer broad exposure.

- Professional management: Fund managers make investment decisions for you.

- Cons:

- Higher expense ratios: Actively managed mutual funds typically have higher annual fees, often ranging from 0.5% to 1.5% or more, which can significantly erode returns over time compared to low-cost ETFs.

- Less liquidity: Mutual funds are typically traded only once a day, after the market closes, at their Net Asset Value (NAV).

- Potential for sales loads: Some mutual funds charge “loads” or commissions (front-end, back-end, or level loads) when you buy or sell shares, further increasing costs.

Index Funds (A Type of Mutual Fund or ETF)

- What they are: Funds (either mutual funds or ETFs) designed to track the performance of a specific market index, such as the S&P 500 or the total U.S. stock market. They are passively managed, meaning they don’t try to beat the market, just match it.

- Pros:

- Extremely low cost: Because they are passively managed, they have minimal operating expenses, often mirroring the low expense ratios of broad market ETFs.

- Broad diversification: By tracking an index, they inherently provide broad market exposure.

- Historically strong performance: Over the long term, index funds tracking broad markets like the S&P 500 have consistently outperformed the majority of actively managed funds. The simplicity and low cost are powerful drivers of long-term wealth.

Trading Costs Recommendation for Beginners: Focus primarily on low-cost, broad-market index ETFs (or index mutual funds if offered without transaction fees by your chosen brokerage). These provide instant diversification, minimize fees, and have a proven track record of strong long-term performance without requiring you to become a stock-picking expert.

Opening Your Investment Account: Step-by-Step for 2026

Once you’ve understood the foundational principles and chosen your preferred investment vehicles, the next practical step is to open an investment account. This process is straightforward and can typically be completed online in a matter of minutes.

Choose the Right Account Type

The type of account you open depends on your goals and tax situation. Each has distinct advantages:

- Taxable Brokerage Account:

- Flexibility: No contribution limits, and you can withdraw funds at any time (though capital gains taxes will apply).

- Taxation: Investment gains (dividends, capital gains from selling appreciated assets) are subject to taxes in the year they are realized.

- Best for: Non-retirement goals like a house down payment, saving for a large purchase, or simply investing beyond the limits of tax-advantaged accounts.

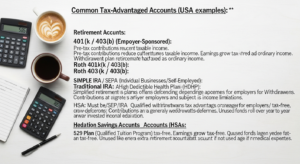

- Retirement Accounts (Tax-Advantaged): These accounts offer significant tax benefits, making them crucial for long-term wealth building.

- Roth IRA:

- Contributions: Made with after-tax money.

- Growth & Withdrawals: Grow tax-free, and qualified withdrawals in retirement are also tax-free.

- Contribution Limit: Subject to IRS limits (e.g., approximately $7,000 for 2026, though this adjusts annually). Income limitations may apply.

- Best for: Individuals who expect to be in a higher tax bracket in retirement than they are today.

- Traditional IRA:

- Contributions: May be tax-deductible in the year you contribute (reducing your taxable income now).

- Growth & Withdrawals: Grow tax-deferred, but withdrawals in retirement are taxed as ordinary income.

- Contribution Limit: Same as Roth IRA (e.g., approximately $7,000 for 2026).

- Best for: Individuals who expect to be in a lower tax bracket in retirement or want immediate tax deductions.

- 401(k) / 403(b): Employer-sponsored retirement plans.

- Contributions: Made directly from your paycheck, often pre-tax (reducing current taxable income). Roth 401(k) options are also available.

- Employer Match: Many employers offer a matching contribution (e.g., they contribute 50 cents for every dollar you contribute, up to 6% of your salary). This is essentially free money and should be maximized before any other investment priority.

- Contribution Limit: Significantly higher than IRAs (e.g., approximately $24,500 for 2026, which typically adjusts annually).

- Best for: Everyone with access to an employer-sponsored plan, especially to capture any matching contributions.

- Roth IRA:

Trading Costs Priority: If available, contribute enough to your 401(k)/403(b) to get the full employer match first. Then, consider maxing out a Roth IRA. After that, contribute more to your 401(k) beyond the match, and finally, consider a taxable brokerage account for additional savings.

Select a Brokerage Firm

Choosing the right brokerage is crucial. Look for firms that align with your needs for low costs, user experience, and available tools. Key criteria include:

- Low/Zero Commissions: Most reputable online brokers now offer commission-free trading for stocks and ETFs. Ensure this is the case.

- Low Expense Ratios: If considering their proprietary funds, check their expense ratios. Vanguard, for instance, is renowned for its ultra-low-cost index funds and ETFs.

- User-Friendly Platform & Mobile App: Especially important for beginners, an intuitive interface makes managing your investments easier.

- Robust Research Tools & Educational Resources: Access to market data, company analysis, and learning materials can be invaluable.

- Customer Service: Accessible and helpful support is important when you have questions.

- Fractional Shares Availability: This allows you to invest a specific dollar amount (e.g., $50) into a stock or ETF, even if the share price is higher. This is excellent for beginners with smaller starting amounts.

Types of Brokerage Firms:

- Discount Brokers: Fidelity, Charles Schwab, Vanguard, E*TRADE, Interactive Brokers. These offer a wide range of investment products and tools, typically with low fees.

- Robo-Advisors: Betterment, Wealthfront. These services use algorithms to manage diversified portfolios based on your risk tolerance and goals. They offer automated rebalancing and tax-loss harvesting, often for a low advisory fee (e.g., 0.25% to 0.50% of assets under management). They are excellent for hands-off investors.

Actionable Step: Research and compare 2-3 firms based on the criteria above. Read recent reviews and explore their platforms before making a decision.

The Account Opening Process

Once you’ve chosen a brokerage, the process is largely online:

- Online Application: Fill out an application providing personal information (name, address, date of birth, Social Security Number or Tax ID, employment details).

- Identity Verification: You may need to upload a copy of your driver’s license or other government ID.

- Link Bank Account: Connect your checking or savings account for easy funding. This typically involves providing your bank’s routing and account numbers, and verifying small trial deposits.

- Review and Sign: Electronically sign the necessary disclosures and agreements.

Funding Your Account

After your account is open and verified, you’ll need to transfer money into it. Common methods include:

- ACH Transfer (Automated Clearing House): The most common method, allowing electronic transfers directly from your bank account. It’s usually free but can take 1-3 business days for funds to settle.

- Wire Transfer: Faster but often incurs a fee from your bank.

- Check Deposit: Mail a check, which will take several days to clear.

Trading Costs Tip: Set up recurring, automatic deposits. Whether it’s $50 or $500 per paycheck or monthly, automating your contributions is one of the most effective ways to build wealth consistently and avoid procrastination.

Crafting Your Diversified Portfolio: Strategies for Long-Term Growth

With your account open and funded, it’s time to build your portfolio. The goal isn’t to pick the next hot stock, but rather to construct a resilient, diversified portfolio that aligns with your long-term goals and risk tolerance.

The Power of Diversification

Diversification is the cornerstone of prudent investing. It’s the strategy of spreading your investments across various assets to minimize risk. The adage “don’t put all your eggs in one basket” holds profound truth in investing. By diversifying, you reduce unsystematic risk – the risk specific to a particular company or industry. If one investment performs poorly, others may perform well, cushioning the impact on your overall portfolio.

- Asset Class Diversification: Spreading investments across different asset classes (e.g., stocks, bonds, real estate, cash).

- Geographic Diversification: Investing in companies across different countries (e.g., U.S. and international stocks) to reduce reliance on a single economy.

- Sector Diversification: Spreading investments across various industries (e.g., technology, healthcare, consumer staples) to avoid overexposure to any single sector.

Core-Satellite Approach (Simplified for Beginners)

A practical way to implement diversification, especially for new investors, is a simplified core-satellite strategy:

- The Core (70-90% of your portfolio): This should consist of broad-market, low-cost index ETFs or mutual funds. These are your foundational, diversified holdings that aim to capture overall market returns.

- Examples:

- A Total U.S. Stock Market ETF (like VTI or ITOT) for exposure to thousands of U.S. companies.

- An S&P 500 ETF (like VOO, IVV, or SPY) for exposure to the 500 largest U.S. companies.

- A Total International Stock Market ETF (like VXUS or IXUS) for global diversification.

- A Total U.S. Bond Market ETF (like BND or AGG) for stability and income (see Asset Allocation below).

- Why: These funds offer instant diversification, low fees, and have historically delivered strong long-term returns, making them ideal for the bulk of your portfolio.

- Examples:

- The Satellite (Optional 10-30% of your portfolio): Once your core is established, if you have a strong interest, time for research, and higher risk tolerance, you can allocate a smaller portion to individual stocks or more niche ETFs (e.g., a specific sector ETF like clean energy or artificial intelligence).

- Why: This portion allows for potential higher returns (and higher risk) if you have conviction in specific investments, without jeopardizing your entire portfolio.

- Caution: For most beginners, sticking to a 100% core strategy with broad-market index funds is often the most effective and least stressful path.

Asset Allocation Based on Age and Goals

Asset allocation is the process of deciding how much of your portfolio to allocate to different asset classes, primarily