Your Definitive Guide to Investing in S&P 500 Index Funds for 2026 and Beyond

The S&P 500 index fund stands as a cornerstone for millions of investors seeking broad market exposure, robust returns, and simplified portfolio management. For individual investors and financially ambitious readers, understanding how to effectively harness this powerful investment vehicle is crucial for building long-term wealth. At Trading Costs, we cut through the noise, offering numbers-backed insights and real strategies. This comprehensive guide will demystify S&P 500 index funds, providing a practical, data-driven roadmap for investing in 2026 and positioning your portfolio for sustained growth. Forget the hype; we’re focusing on specific, actionable steps to integrate this foundational asset into your financial future.

Understanding the S&P 500: The Benchmark of American Equities

Before diving into investment vehicles, it’s essential to grasp what the S&P 500 truly represents. The S&P 500, short for the Standard & Poor’s 500, is a stock market index that tracks the performance of 500 of the largest publicly traded companies in the United States. These companies are selected by a committee at S&P Dow Jones Indices based on criteria such as market size, liquidity, and sector representation, ensuring the index is a reliable barometer of the U.S. stock market and the broader economy.

Unlike a simple average, the S&P 500 is a market-capitalization-weighted index. This means companies with larger market values (share price multiplied by the number of outstanding shares) have a greater impact on the index’s performance. For instance, a movement in Apple or Microsoft, which are among the largest components, will influence the index more significantly than a similar percentage move in a smaller constituent company. This weighting accurately reflects the overall market value distribution.

Why is the S&P 500 so important? It serves multiple critical functions:

* Economic Indicator: Economists, analysts, and policymakers closely monitor the S&P 500 as a leading indicator of U.S. economic health.

* Diversification: By investing in the S&P 500, you gain exposure to a vast array of industries—from technology and healthcare to finance and consumer staples—providing immediate, broad diversification across the American economy.

* Performance Benchmark: It is the most widely cited benchmark for large-cap U.S. equities. Professional money managers are often judged on how well their portfolios perform relative to the S&P 500.

Historically, the S&P 500 has demonstrated remarkable resilience and growth. Over multi-decade periods, it has delivered average annual returns in the double digits, a testament to the long-term upward trend of the U.S. economy and corporate earnings. While past performance is never a guarantee of future results, this consistent historical track record underscores its appeal as a core holding for long-term investors. Investing in an S&P 500 index fund allows you to capture these returns without the arduous task of picking individual stocks.

Why Invest in S&P 500 Index Funds? The Case for Passive Investing

The allure of S&P 500 index funds stems from a confluence of compelling advantages that align perfectly with the principles of smart, cost-effective investing. For individual investors, they offer a powerful combination of diversification, low costs, simplicity, and historically robust performance, making them a cornerstone of passive investment strategies.

Instant Diversification

When you invest in an S&P 500 index fund, you are not buying a single stock; you are buying a tiny slice of 500 different companies. This inherent diversification significantly reduces company-specific risk. If one company faces challenges, its impact on your overall portfolio is mitigated by the performance of the other 499 constituents. This broad exposure across various sectors and industries provides a robust foundation for your portfolio, smoothing out volatility compared to holding just a handful of individual stocks.

Low Costs: The Power of Expense Ratios

One of the most significant advantages of index funds, and a core tenet of Trading Costs, is their remarkably low expense ratios (ERs). An expense ratio is the annual fee charged by the fund provider as a percentage of your investment. Because S&P 500 index funds are passively managed—meaning they simply track the index rather than employing a team of analysts to pick stocks—their operational costs are minimal.

Typical S&P 500 index funds boast ERs ranging from as low as 0.03% to around 0.09%. To put this into perspective, for every $10,000 invested, you might pay only $3 to $9 per year in fees. Compare this to actively managed mutual funds, which often carry ERs between 0.50% and 1.50% or even higher. Over decades, these seemingly small differences compound dramatically. A 1% difference in fees can erode tens of thousands, even hundreds of thousands, of dollars from your portfolio’s growth over a long investing horizon. Minimizing these “trading costs” directly translates into greater wealth accumulation for you.

Simplicity and Time Efficiency

Investing in an S&P 500 index fund is remarkably straightforward. Once you’ve chosen your fund and set up your investment, there’s little need for constant monitoring, research, or rebalancing—at least not at the individual stock level. This “set it and forget it” approach (with periodic portfolio reviews) frees up your time and reduces the psychological stress often associated with active stock picking. It allows you to focus on other aspects of your financial life while your investment quietly grows.

Historical Performance and the Challenge to Active Management

The data consistently shows that the vast majority of actively managed funds fail to beat their benchmark, the S&P 500, over the long term, especially after accounting for their higher fees. Studies across decades routinely reveal that a significant percentage of active fund managers underperform the S&P 500 over 5, 10, and 15-year periods. This isn’t due to a lack of effort or skill from active managers, but rather the inherent difficulty of consistently outperforming a broad, efficient market, coupled with the drag of higher trading costs and management fees. By investing in an S&P 500 index fund, you are essentially betting on the collective success of the largest American companies, a bet that has historically paid off handsomely for patient investors.

Tax Efficiency

S&P 500 index funds tend to be more tax-efficient than actively managed funds, particularly in taxable brokerage accounts. Because they simply track an index, they have lower portfolio turnover (i.e., they buy and sell stocks less frequently). This results in fewer capital gains distributions, which are taxable events for investors. Lower turnover means you defer taxes on capital gains until you actually sell your shares, allowing your investments to grow unimpeded for longer.

Choosing Your S&P 500 Vehicle: ETFs vs. Mutual Funds

Once you’ve committed to investing in the S&P 500, the next practical step is selecting the right investment vehicle. The two primary options are Exchange-Traded Funds (ETFs) and traditional Index Mutual Funds. Both offer exposure to the S&P 500, but they differ in how they are traded, their cost structures, and minimum investment requirements.

S&P 500 Exchange-Traded Funds (ETFs)

ETFs are funds that hold a basket of assets—in this case, the 500 stocks of the S&P 500—but trade on stock exchanges like individual stocks.

* Trading Flexibility: ETFs can be bought and sold throughout the trading day at market prices, similar to stocks. This offers more flexibility for investors who wish to react to intraday market movements, though for long-term S&P 500 investing, this is rarely a significant advantage.

* Lower Minimums: Most ETFs can be purchased for the price of a single share, making them accessible to investors with smaller amounts of capital. Many brokerages also offer fractional share investing, allowing you to invest any dollar amount you choose.

* Expense Ratios: S&P 500 ETFs are renowned for their ultra-low expense ratios, often identical to or even slightly lower than their mutual fund counterparts.

* Examples:

* SPDR S&P 500 ETF Trust (SPY): One of the oldest and most liquid ETFs, SPY is often used by institutional investors and traders. Its expense ratio is 0.09%.

* iShares Core S&P 500 ETF (IVV): Offered by BlackRock, IVV also tracks the S&P 500 with an extremely competitive expense ratio of 0.03%.

* Vanguard S&P 500 ETF (VOO): Vanguard’s offering, VOO, is highly popular among individual investors due to its low 0.03% expense ratio and Vanguard’s reputation for investor-friendly practices.

S&P 500 Index Mutual Funds

Traditional index mutual funds are pooled investment vehicles that also track the S&P 500.

* Trading Simplicity: Mutual funds are bought and sold only once a day, after the market closes, at their Net Asset Value (NAV). This eliminates the need to monitor intraday price fluctuations.

* Automated Investing: Mutual funds are often ideal for automated investing strategies, allowing you to set up regular, recurring contributions directly from your bank account.

* Minimum Investments: Historically, index mutual funds often had higher minimum initial investment requirements (e.g., $3,000 for Vanguard’s Admiral Shares, or lower for specific fund families). However, many brokers now offer their own S&P 500 index mutual funds with no minimums or very low minimums.

* Expense Ratios: Competitive S&P 500 index mutual funds also feature very low expense ratios, often in the 0.03% to 0.09% range.

* Examples:

* Vanguard 500 Index Fund Admiral Shares (VFIAX): A flagship fund from Vanguard, known for its low 0.04% expense ratio (requires a $3,000 minimum initial investment).

* Fidelity 500 Index Fund (FXAIX): Fidelity’s popular S&P 500 index mutual fund, boasting a minuscule 0.015% expense ratio and no minimum initial investment.

* Schwab S&P 500 Index Fund (SWPPX): Charles Schwab’s equivalent, with a 0.02% expense ratio and a $1 minimum.

Key Considerations for Your Choice:

* Expense Ratio: Prioritize the lowest possible ER. Even a few basis points (0.01%) matter over decades.

* Tracking Error: This measures how closely the fund’s performance matches the index it tracks. Reputable S&P 500 funds have minimal tracking error.

* Minimum Investment: If you’re starting with a small amount, ETFs or mutual funds with no minimums (like FXAIX or SWPPX) are often preferable.

* Brokerage Account: Your existing brokerage may offer proprietary S&P 500 funds with zero transaction fees, which can simplify management.

* Trading Habits: If you prefer setting up automated contributions and not thinking about market timing, mutual funds can be more convenient. If you prefer the flexibility of trading throughout the day or wish to employ limit orders, ETFs might appeal more.

For most long-term individual investors focused on consistent contributions and minimal intervention, the choice between a low-cost S&P 500 ETF and a low-cost S&P 500 index mutual fund often comes down to personal preference and which provider aligns best with their overall financial strategy. Both are excellent vehicles for capturing the growth of the U.S. large-cap market.

How to Invest in the S&P 500 Index Fund: A Step-by-Step Guide for 2026

Investing in an S&P 500 index fund is a straightforward process, but it requires a structured approach to ensure you set yourself up for long-term success. Here’s a practical, step-by-step guide for getting started in 2026:

Step 1: Define Your Investment Goals and Risk Tolerance

Before you commit any capital, understand why you are investing and what your financial timeline looks like.

* Goals: Are you saving for retirement (20+ years away), a down payment on a house (5-10 years), or another objective? Long-term goals are best suited for equity investments like the S&P 500.

* Risk Tolerance: While the S&P 500 offers diversification, it is still an equity investment subject to market fluctuations. Be prepared for periods of volatility and potential drawdowns. Your ability to stomach these downturns without panicking and selling is crucial. The S&P 500 is generally considered a moderate-risk investment for a long horizon.

Step 2: Choose and Open a Brokerage Account

You need a financial intermediary to buy and hold your S&P 500 fund. Consider the following account types:

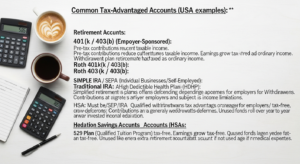

* Tax-Advantaged Accounts:

* Individual Retirement Accounts (IRAs): Traditional IRA (tax-deductible contributions, tax-deferred growth) or Roth IRA (after-tax contributions, tax-free growth in retirement). Excellent for long-term retirement savings.

* 401(k) / 403(b): If your employer offers one, check if an S&P 500 index fund is available as an investment option. These offer significant tax benefits and often employer matching contributions.

* Taxable Brokerage Accounts: For investments outside of retirement accounts, offering flexibility but subject to capital gains taxes on distributions and sales.

Reputable Brokerage Firms:

* Vanguard: Known for its low-cost index funds and ETFs (e.g., VOO, VFIAX).

* Fidelity: Offers a wide range of low-cost funds, including zero-expense-ratio index funds (e.g., FXAIX).

* Charles Schwab: Another leader in low-cost investing (e.g., SWPPX, SCHX ETF).

ETRADE, TD Ameritrade (now Schwab), Interactive Brokers: Offer robust platforms for self-directed investors.

The account opening process typically involves providing personal information (SSN, address, employment details) and linking a bank account.

Step 3: Fund Your Account

Once your brokerage account is open, you need to deposit money into it. Common methods include:

* Electronic Funds Transfer (EFT): Linking your bank account for direct transfers (usually takes 1-3 business days).

* Wire Transfer: Faster but often involves a fee from your bank.

* Check Deposit: Slower processing time.

* Direct Deposit: Some brokers allow you to set up a portion of your paycheck to be deposited directly into your investment account.

Step 4: Select Your S&P 500 Fund

Based on your preferences (ETFs vs. Mutual Funds, expense ratio, minimums, brokerage offerings), choose your specific S&P 500 fund.

* ETFs: VOO (Vanguard), IVV (iShares), SPY (SPDR). Search for them by their ticker symbol.

* Mutual Funds: VFIAX (Vanguard), FXAIX (Fidelity), SWPPX (Schwab). Search by ticker or fund name.

Pay close attention to the expense ratio (ER). Aim for funds with ERs below 0.10%, ideally in the 0.03%-0.05% range.

Step 5: Place Your Order

This is where you execute your investment.

* For ETFs:

* Enter the ticker symbol (e.g., VOO).

* Specify the number of shares or a dollar amount (if fractional shares are available).

* Choose your order type:

* Market Order: Buys/sells immediately at the current market price. Best for highly liquid ETFs like S&P 500 funds.

* Limit Order: Buys/sells only at a specified price or better. Can be useful if you’re trying to buy on a dip, but might not execute if the price isn’t met. For long-term S&P 500 investing, a market order is usually sufficient.

* Review and confirm your order.

* For Mutual Funds:

* Enter the fund name or ticker symbol (e.g., FXAIX).

* Specify the dollar amount you wish to invest.

* Mutual fund orders are processed at the fund’s Net Asset Value (NAV) calculated at the end of the trading day.

* Review and confirm.

Consider implementing a dollar-cost averaging (DCA) strategy from the outset. Instead of investing a lump sum all at once, invest a fixed amount regularly (e.g., $200 every two weeks or $500 monthly). This strategy helps mitigate the risk of investing a large sum at a market peak and averages out your purchase price over time.

Step 6: Monitor and Rebalance (Periodically)

While S&P 500 index investing is largely “set it and forget it,” it doesn’t mean “never look at it.”

* Monitor: Periodically check your account to ensure transactions are occurring as planned and to observe your portfolio’s growth. Avoid daily checking, as short-term fluctuations can induce unnecessary stress.

* Rebalance: The S&P 500 fund itself is internally rebalanced to track the index. However, within your broader portfolio, you might need to rebalance your asset allocation (e.g., stocks vs. bonds, U.S. vs. international) every 1-2 years to maintain your desired risk profile. For instance, if your S&P 500 holdings grow significantly, they might become a larger percentage of your total portfolio than intended, requiring you to trim them or add to other asset classes.

Optimizing Your S&P 500 Investment Strategy

Investing in an S&P 500 index fund is a smart move, but optimizing your strategy can significantly enhance your long-term returns and minimize “trading costs” in their broadest sense—including opportunity costs and tax inefficiencies.

Embrace Dollar-Cost Averaging (DCA) Consistently

As mentioned in the previous section, dollar-cost averaging is a powerful technique. By investing a fixed amount of money at regular intervals (e.g., monthly or quarterly), you automatically buy more shares when prices are low and fewer shares when prices are high. This systematic approach eliminates the need to time the market, a notoriously difficult and often futile endeavor for even professional investors.

Example: If you invest $500 per month into an S&P 500 fund:

* Month 1: Fund price is $100/share, you buy 5 shares.

* Month 2: Fund price drops to $80/share, you buy 6.25 shares.

* Month 3: Fund price rises to $110/share, you buy 4.55 shares.

Over time, your average cost per share will be lower than if you had tried to guess market highs and lows. The discipline of DCA also fosters consistent savings habits, which is arguably even more crucial than specific investment selections.

Prioritize a Long-Term Horizon

The S&P 500 is not a vehicle for short-term gains. Its historical performance shines over multi-year and multi-decade periods. While the market experiences corrections and bear markets (drops of 10% and 20% respectively) periodically, its long-term trend has always been upward.

* Historical Resilience: Since its inception, the S&P 500 has recovered from every major downturn. The average length of a bear market is significantly shorter than the average length of a bull market.

* Compounding: The true magic of investing lies in compounding returns. Reinvesting dividends and allowing your gains to generate further gains requires time. A 10-year investment horizon is generally considered a minimum for equities, with 20+ years being ideal for maximizing the power of the S&P 500.

Minimize All Trading Costs

This is the core philosophy of our blog. Beyond just expense ratios, consider:

* Commissions: Most major brokerages now offer commission-free trading for ETFs and many mutual funds. Ensure your chosen fund is commission-free.

* Bid-Ask Spreads: For ETFs, the difference between the bid (highest price a buyer is willing to pay) and ask (lowest price a seller is willing to accept) can be a minor cost. Highly liquid S&P 500 ETFs like VOO, IVV, and SPY have very tight spreads, making this negligible for most investors.

* Avoid Unnecessary Trading: Frequent buying and selling not only incurs potential transaction costs but also increases the likelihood of poor market timing decisions and generates taxable events. Stick to your long-term plan.

Leverage Tax-Efficient Account Placement

Strategic placement of your S&P 500 fund can significantly impact your net returns.

* Tax-Advantaged Accounts First: Prioritize investing in your 401(k), 403(b), IRA, or Roth IRA.

* Growth Potential: S&P 500 funds are designed for growth. Placing them in accounts where gains grow tax-deferred (Traditional IRA, 401k) or tax-free (Roth IRA) means you avoid annual taxes on dividends and capital gains distributions. This allows your money to compound faster.

* Employer Match: Always contribute enough to your employer’s retirement plan to get the full match—it’s free money, an immediate 100% return on that portion of your investment.

* Taxable Accounts: If you’ve maxed out your tax-advantaged options, then use a taxable brokerage account. Even here, the S&P 500 fund’s low turnover makes it relatively tax-efficient compared to actively managed funds.

Integrate into a Diversified Portfolio

While the S&P 500 provides excellent diversification within U.S. large-cap equities, it is not a complete portfolio on its own.

* Global Diversification: Consider adding an international stock index fund (e.g., a total international market fund) to gain exposure to developed and emerging markets outside the U.S. This further reduces geographic risk.

* Bonds: Depending on your age and risk tolerance, incorporating a bond index fund can stabilize your portfolio, provide income, and reduce overall volatility, especially as you approach retirement.

* Asset Allocation: Your S&P 500 allocation should be part of a broader asset allocation strategy tailored to your individual risk profile, time horizon, and financial goals. For example, a younger investor might have 80-90% in equities (including S&P 500) and 10-20% in bonds, while someone closer to retirement might shift to 60% equities and 40% bonds.

By adopting these optimization strategies, you’re not just investing in the S&P 500; you’re building a resilient, cost-effective, and tax-efficient foundation for your long-term financial success.

Frequently Asked Questions About S&P 500 Index Funds

Q: Is it too late to invest in the S&P 500 for 2026?

A: Absolutely not. While market timing is generally ill-advised, the S&P 500 has demonstrated an upward trend over the long term, despite periodic downturns. Investing in 2026, or any year, with a long-term horizon (10+ years) allows you to benefit from the power of compounding and the market’s historical resilience. Time in the market, not timing the market, is the key.

Q: What’s the “best” S&P 500 ETF or mutual fund?

A: The “best” fund largely depends on your specific needs, but for most investors, it comes down to a few top contenders. Look for funds with the lowest expense ratios (typically 0.03% to 0.09%), minimal tracking error, and from reputable providers. Popular choices like Vanguard’s VOO or VFIAX, Fidelity’s FXAIX, and iShares’ IVV are all excellent, highly competitive options. The differences between them are often negligible for the average long-term investor.

Q: Can I lose money investing in the S&P 500?

A: Yes, it is entirely possible to lose money, especially in the short term. The S&P 500, like any equity investment, is subject to market fluctuations, economic downturns, and geopolitical events. There will be periods where your investment value decreases. However, historically, over long periods (e.g., 10+ years), the S&P 500 has consistently recovered from drawdowns and delivered positive average annual returns. Patience and a long-term perspective are crucial.

Q: How much money do I need to start investing in the S&P 500?

A: You can start with surprisingly little. Many brokerages offer fractional share investing for ETFs, allowing you to invest any dollar amount (e.g., $50) rather than needing enough to buy a full share. For mutual funds, some providers like Fidelity (FXAIX) and Schwab (SWPPX) have eliminated minimum initial investment requirements entirely. Even with a modest amount, consistent contributions through dollar-cost averaging can build significant wealth over time.

Q: Should I invest all my money in the S&P 500?

A: While the S&P 500 offers excellent diversification within U.S. large-cap equities, it’s generally not advisable to put all your investable money into a single index. A truly