Mastering the Leverage Game: Understanding Margin Accounts and Interest Rates in 2026

The allure of market leverage is a powerful draw for retail investors. The ability to control more stock than your cash balance allows can accelerate gains during a bull market, transforming a modest portfolio into a significant powerhouse. However, leverage is never free. As we navigate the financial landscape of 2026, the mechanics of margin accounts have become more sophisticated, and the impact of interest rates on net returns has never been more critical. For the cost-conscious trader, understanding the nuance of margin isn’t just about knowing how to buy more shares; it’s about understanding the “hurdle rate”—the minimum return your investments must achieve just to break even after accounting for borrowing costs. This guide delves into the structural realities of margin accounts, the mathematics of interest accrual, and the strategic maneuvers necessary to keep your overhead low while maximizing your market exposure.

How Margin Accounts Work: The Mechanics of Borrowed Capital

At its core, a margin account is a brokerage account that allows the investor to borrow money from the broker to purchase securities. The securities in the account serve as collateral for the loan. While a standard cash account requires you to pay the full price for every share, a margin account operates under the framework of “buying on margin.”

In 2026, most brokerage firms still operate under the fundamental guidelines of Regulation T (Reg T), which generally allows investors to borrow up to 50% of the purchase price of a security. This is known as the **Initial Margin**. For example, if you wish to purchase $20,000 worth of a highly liquid tech stock, you provide $10,000 of your own capital, and the broker lends you the remaining $10,000.

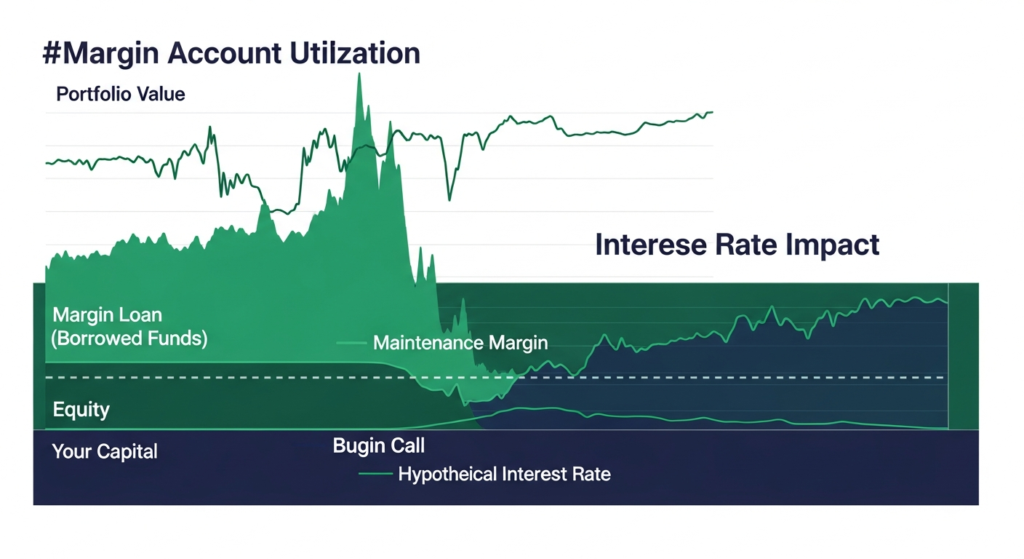

The relationship doesn’t end at the purchase. Once you hold a margined position, you must adhere to **Maintenance Margin** requirements. This is the minimum amount of equity you must maintain in your account at all times. If the value of your stocks drops significantly, your equity—the difference between the market value of the securities and the amount you owe the broker—decreases. If it falls below the maintenance threshold (often 25% to 30%, depending on the volatility of the asset), the broker will issue a **Margin Call**. This requires you to either deposit more cash or sell assets immediately to bring the account back to the required level. Understanding these mechanical triggers is the first step in avoiding forced liquidations that can decimate a portfolio.

Decoding Margin Interest Rates: How Costs Are Calculated

For the retail trader focused on cost-efficiency, the interest rate is the most important variable in the margin equation. Margin interest is not a flat fee; it is an annual percentage rate (APR) that is usually calculated daily and charged monthly.

Brokers typically set their margin rates based on a **Base Rate** (such as the Federal Funds Rate or the Effective Federal Funds Rate) plus a **Spread** or markup. In the economic environment of 2026, these spreads vary wildly between “zero-commission” brokers and “pro-tier” platforms.

The formula for calculating your daily interest cost is:

*Daily Interest = (Margin Balance x Annual Interest Rate) / 360 (or 365)*

Most brokers use a 360-day year for this calculation, which slightly increases the effective cost to the borrower. For instance, if you have a $50,000 debit balance at an 8% interest rate, your daily cost is approximately $11.11. While $11 may seem negligible, over a month, that is over $330. Over a year, you are paying nearly $4,000 in interest. This “debit balance” is the actual amount you owe the broker. Unlike a mortgage or an auto loan, margin interest is often “capitalized,” meaning the unpaid interest is added to your balance, potentially leading to a compounding effect where you end up paying interest on previous interest.

The Hurdle Rate: Why High Interest Rates Kill Returns

The primary danger for retail investors is ignoring the **Hurdle Rate**. If your broker charges you 9% interest on your margin loan, your investment must appreciate by more than 9% annually just for you to stay flat on the borrowed portion of your capital.

Let’s look at the math for a cost-conscious trader:

Suppose you invest $10,000 of your own money and borrow $10,000 on margin to buy $20,000 of an ETF.

– **Scenario A (No Margin):** The ETF rises 10%. You make $1,000. Your return is 10%.

– **Scenario B (With Margin at 9%):** The ETF rises 10%. The total value is $22,000. You owe $10,000 (principal) + $900 (interest). Your remaining equity is $11,100. Your net profit is $1,100. Your return on your $10,000 is 11%.

In Scenario B, despite doubling your exposure, you only increased your net return by 1%. You took on 100% more risk for a mere 1% of additional profit. This illustrates the “drag” of interest rates. When interest rates are high, the margin for error becomes razor-thin. If the ETF had only gained 5%, the margin trader would have actually *lost* money ($1,000 gain minus $900 interest, but with the added risk and potential for a margin call if the price had dipped mid-year). To minimize costs, traders must aggressively seek the lowest possible interest rates or ensure their expected alpha significantly exceeds the borrowing cost.

Strategies for Minimizing Margin Interest Expenses

Active traders in 2026 use several sophisticated strategies to keep their borrowing costs from eroding their capital.

1. **Tiered Pricing Advantage:** Many brokers offer tiered interest rates. The more you borrow, the lower the rate. While it sounds counter-intuitive to borrow more to save money, some traders consolidate their various loans (like high-interest credit card debt or personal loans) into a margin loan if their portfolio size allows for a lower interest tier, provided they maintain a massive safety buffer.

2. **Negotiating with Your Broker:** Margin rates are often negotiable, especially for accounts over $100,000. If you have a clean trading history and a substantial balance, call your broker’s “Private Client” or “Active Trader” desk. Mentioning a competitor’s lower rate is often enough to secure a 1% to 2% reduction in your spread.

3. **Asset-Based Lending Alternatives:** Some firms offer “Pledged Asset Lines” (PALs) or “Securities-Based Lines of Credit” (SBLOCs). These are separate from the trading margin and often come with lower interest rates. While you cannot use a PAL to buy more securities (due to Reg U requirements), you can use it for outside expenses, preventing you from having to sell your stocks and trigger capital gains taxes.

4. **Portfolio Margin:** For experienced traders with at least $110,000 to $150,000 in equity, applying for **Portfolio Margin** can be a game-changer. Unlike Reg T margin, which uses fixed percentages, Portfolio Margin calculates risk based on the overall volatility of the portfolio. This often allows for higher leverage but, more importantly, can lead to more efficient capital use and potentially lower interest-bearing debit balances.

Risk Management: Avoiding the Dreaded Margin Call

The most expensive event in a trader’s career is a margin call. When a broker issues a call, they are entitled to sell your positions at current market prices—which are usually at a low point—to cover the loan. You lose control over the timing of your exit, often “locking in” losses.

To minimize the “hidden costs” of margin risk, implement a **Self-Imposed Maintenance Level**. If your broker requires 30% equity, you should aim to never let your equity drop below 50%. This “buffer” ensures that a 10% or 15% market correction doesn’t trigger a liquidation.

Furthermore, cost-conscious traders avoid using margin on highly volatile stocks. Brokers often increase “Special Maintenance Requirements” for meme stocks or low-cap biotech firms, sometimes requiring 100% margin (meaning you cannot borrow against them at all). By sticking to highly liquid ETFs or blue-chip stocks for your margined positions, you benefit from the lowest maintenance requirements and the most stable interest rate tiers.

Alternatives to Traditional Margin for the Cost-Conscious

If the interest rates in 2026 are prohibitively high, savvy traders look for “synthetic leverage,” which often carries a lower “embedded” interest rate than a brokerage debit balance.

– **Deep-in-the-Money (ITM) LEAPS:** Buying a Call option with an expiration date a year or two away (LEAPS) and a strike price far below the current market price mimics the movement of the stock. The “extrinsic value” or “premium” you pay for the option is often cheaper than the cumulative interest you would pay on a margin loan over the same period.

– **Futures Contracts:** For broad market exposure (like the S&P 500), futures offer incredibly high leverage with very low capital requirements. The “cost of carry” in futures is often more institutional and competitive than retail margin rates.

– **Box Spreads:** A highly advanced strategy involves using European-style options (like SPX) to create a “Box Spread.” This is essentially a way for a retail investor to borrow money at rates very close to the Treasury rate, bypassing the broker’s markup entirely. However, this requires a deep understanding of option Greeks and is generally reserved for professional-level retail traders.

FAQ

**Q1: Is margin interest tax-deductible in 2026?**

Generally, margin interest is considered “investment interest expense.” In the United States, you can deduct investment interest expense up to the amount of your net investment income. However, you must itemize your deductions on your tax return. It is always advisable to consult with a tax professional regarding your specific situation.

**Q2: Can a broker change my margin interest rate without notice?**

Yes. Most margin agreements state that the interest rate is variable and can change at the broker’s discretion, usually in line with changes to the Base Rate. Brokers are typically not required to provide advance notice of a rate hike, although most will notify you via the platform or email.

**Q3: What happens if I can’t meet a margin call?**

If you cannot deposit more funds or sell securities to meet the call, the broker has the legal right to sell any or all of the securities in your account without consulting you. They will choose which ones to sell, often starting with the most liquid assets, to satisfy the debt. You are also responsible for any remaining deficit if the sale of the securities doesn’t cover the loan.

**Q4: Does margin interest accrue on weekends and holidays?**

Yes. Interest is calculated based on the number of days you hold the debit balance. Since the loan remains outstanding over weekends and holidays when the markets are closed, you continue to accrue interest during those times.

**Q5: Is there a way to see how much margin interest I’ve paid so far?**

Most modern trading platforms provide a “YTD Interest Paid” section in the account settings or monthly statements. Monitoring this regularly is vital for understanding your true net performance.

Conclusion: Balancing Leverage and Expense

In the fast-moving markets of 2026, margin remains one of the most powerful tools in a retail investor’s arsenal, but it is a tool that requires surgical precision. The difference between a successful leveraged trader and one who faces financial ruin often comes down to the management of interest expenses and the maintenance of a safety buffer.

To minimize costs, you must view margin interest not as a minor fee, but as a significant capital expense. Shop for brokers with the lowest spreads, negotiate your rates, and always calculate your hurdle rate before entering a position. By treating your margin account with the same scrutiny a CFO treats a corporate balance sheet, you can harness the power of leverage while shielding your portfolio from the eroding effects of high interest rates and the catastrophic risks of margin calls. Leverage is a bridge to higher returns, but only if the cost of building that bridge doesn’t exceed the value of the destination.