Mastering the Market Downturn: A Comprehensive Short Selling Stocks Guide for Beginners

The traditional mantra of investing has always been “buy low, sell high.” For decades, retail investors have been conditioned to look for growth, seeking out companies with rising trajectories and holding them through thick and thin. However, the financial landscape of 2026 demands a more versatile toolkit. What happens when the market turns sour, or when a specific sector faces an inevitable correction? This is where short selling comes into play.

Short selling is the practice of profiting from a decline in a stock’s price. While it may seem counterintuitive—selling something you don’t yet own—it is a fundamental pillar of modern trading that provides liquidity and price discovery to the markets. For the retail investor looking to minimize costs while maximizing flexibility, understanding how to “short” is no longer an advanced luxury; it is a necessary skill for portfolio protection and profit generation in bear markets. This guide will break down the mechanics, risks, and cost-saving strategies of short selling to help you navigate the markets with confidence.

—

1. How Short Selling Works: The Mechanics of the “Inverse” Trade

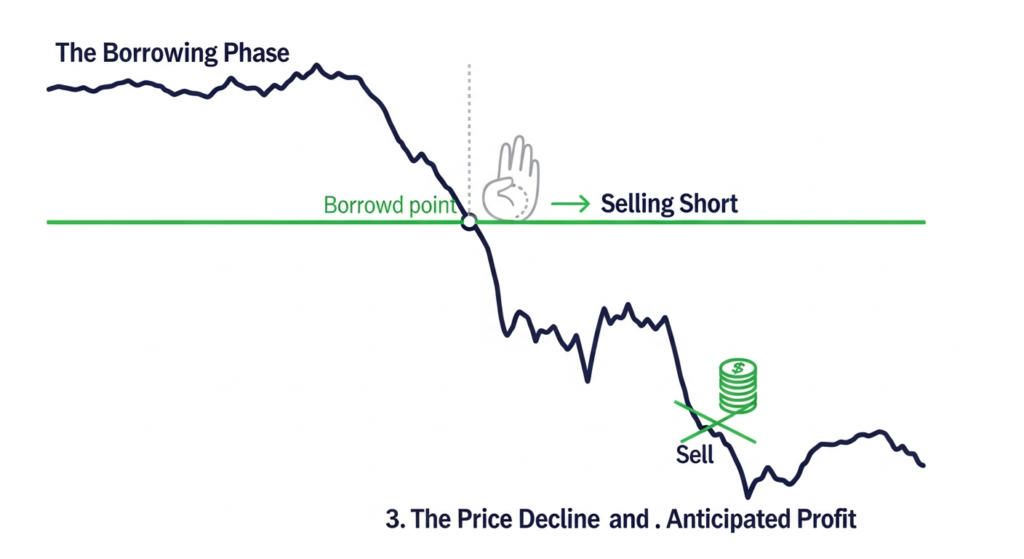

To understand short selling, you must flip your traditional perspective of a trade. In a standard “long” position, you buy a stock today, hold it, and sell it later at a higher price. In a “short” position, the sequence is reversed: you sell the stock first and buy it back later.

#

The Role of the Broker

Because you do not own the shares you wish to sell, you must borrow them. This is facilitated by your brokerage firm. The broker takes shares from their own inventory, from another client’s margin account, or from another brokerage, and lends them to you. You immediately sell these borrowed shares on the open market at the current market price. The proceeds from this sale are deposited into your account, but they are “restricted”—you cannot withdraw them because you still owe the broker the shares you borrowed.

#

Closing the Position (Covering)

To “close” your short position, you must engage in a transaction called “buying to cover.” You go back into the market, purchase the same number of shares you borrowed, and return them to the lender.

* **Profit Scenario:** If you sold the shares at $100 and bought them back at $70, you keep the $30 difference (minus fees).

* **Loss Scenario:** If the stock rises to $130 and you are forced to buy it back, you have lost $30 per share.

#

The Margin Account Requirement

For retail traders, short selling requires a **margin account**. You cannot short stocks in a standard cash account. Under federal regulations (specifically Regulation T in the U.S.), you must maintain a certain amount of equity in your account to serve as collateral for the borrowed shares. Typically, this requires an initial margin of 50% of the value of the short sale.

—

2. Why Short Sell? Profit Potential and Strategic Hedging

Short selling is often portrayed as a “predatory” move by hedge funds, but for the retail investor, it serves two very practical purposes: speculation and hedging.

#

Speculating on Overvaluation

Markets rarely move in a straight line. Often, stocks become disconnected from their fundamental reality due to hype, “meme” stock rallies, or irrational exuberance. By 2026, retail traders have become increasingly adept at identifying “bubbles.” Short selling allows you to profit when these bubbles inevitably burst. If a company reports failing earnings or faces a massive regulatory hurdle, short selling is the only way to turn that negative news into a positive return.

#

Hedging Your Long Portfolio

This is perhaps the most undervalued use of shorting for beginners. Imagine you own a portfolio of high-quality tech stocks that you want to hold for the next ten years. However, you suspect the tech sector will face a temporary 10% dip over the next three months. Rather than selling your long-term holdings (which might trigger capital gains taxes), you can “short” a tech index ETF or a similar competitor stock. If the market dips, the profits from your short position will offset the losses in your long-term portfolio. This is known as a “market-neutral” strategy.

—

3. The Risks of Shorting: Understanding Unlimited Liability

While the mechanics of shorting are straightforward, the risks are fundamentally different from traditional investing. Every beginner must respect the “asymmetry of risk” inherent in shorting.

#

The Ceiling vs. The Floor

When you buy a stock at $50, your maximum loss is $50 (if the company goes to zero). Your potential gain is infinite.

When you **short** a stock at $50, your maximum profit is $50 (if the company goes to zero). However, your potential loss is **unlimited**. Because there is no theoretical limit to how high a stock price can go, you could technically lose much more than your initial investment.

#

The Dreaded “Short Squeeze”

A short squeeze occurs when a heavily shorted stock begins to rise in price. As the price climbs, short sellers begin to lose money and “panic buy” to cover their positions. This influx of buying pressure drives the price even higher, forcing even more short sellers to exit. This feedback loop can cause astronomical price spikes in a matter of hours.

#

Margin Calls and Buy-ins

If the stock you shorted rises significantly, your broker may issue a “margin call,” requiring you to deposit more cash to cover the increased risk. If you cannot provide the funds, the broker has the right to close your position immediately at market price, regardless of the loss. Furthermore, if the original lender of the shares wants them back and the broker cannot find other shares to borrow, you may be subjected to a “forced buy-in.”

—

4. Cost-Efficient Shorting Strategies for Retail Traders

For retail investors, the goal is to minimize the friction of trading. Short selling carries unique costs that can eat into your profits if you aren’t careful.

#

Borrow Fees and “Hard to Borrow” (HTB) Stocks

Not all stocks cost the same to short. “Easy to Borrow” (ETB) stocks usually have no extra fees. However, stocks with high short interest or low float are labeled “Hard to Borrow.” Brokers charge an annualized fee—sometimes as high as 20% to 100%—to borrow these shares. As a beginner, stick to ETB stocks to minimize costs.

#

Margin Interest

Since shorting is done on margin, you are effectively borrowing the broker’s assets. While you get the cash from the sale, you must maintain a margin balance, and brokers charge interest on this. To minimize costs, look for brokers that offer competitive margin rates or consider short-term trades to avoid accruing daily interest.

#

Dividends: The Hidden Cost

If you short a stock and that company pays a dividend while you are holding the position, **you are responsible for paying that dividend** out of your own pocket. The dividend is paid to the person you “borrowed” the shares from. Always check the ex-dividend date before entering a short position to avoid this unexpected expense.

#

Low-Cost Alternatives: Inverse ETFs and Puts

If direct shorting feels too expensive or risky, consider these alternatives:

* **Inverse ETFs:** These are funds designed to move in the opposite direction of an index (e.g., the S&P 500). You can buy these in a standard cash account, avoiding margin interest and unlimited risk.

* **Put Options:** Buying a put option gives you the right to sell a stock at a specific price. Your risk is strictly limited to the price you paid for the option (the premium), yet you still profit from a downward move.

—

5. Step-by-Step Guide to Placing Your First Short Trade

If you’ve weighed the risks and are ready to proceed, follow this tactical workflow to execute your first short trade efficiently.

1. **Identify a Catalyst:** Don’t short a stock just because it “looks high.” Look for a fundamental catalyst (poor earnings, a dying industry) or a technical catalyst (the stock breaking below a major support level).

2. **Verify Borrow Availability:** Check your brokerage platform to see if the stock is “Easy to Borrow.” If it is “Hard to Borrow,” check the daily fee. If the fee is too high, it may not be worth the trade.

3. **Calculate Position Sizing:** Because of the unlimited risk, never put a large percentage of your account into a single short position. Most professionals recommend keeping a single short position to less than 2-3% of your total portfolio.

4. **Execute the “Sell to Open” Order:** Enter your order as a “Sell Short” or “Sell to Open.” This signals to the broker that you are initiating a new short position rather than selling shares you already own.

5. **Set a Stop-Loss Immediately:** This is non-negotiable for beginners. Set a “Stop-Loss Buy” order at a price point where your thesis is proven wrong. This protects you from a catastrophic short squeeze.

6. **Monitor and Cover:** Once the stock hits your profit target, execute a “Buy to Close” order. This returns the shares and locks in your profit.

—

6. Key Rules and Regulations to Know

The regulatory environment for short selling is stricter than for long investing, designed to prevent market manipulation.

#

Regulation SHO and the “Uptick Rule”

In many markets, including the U.S., the “Alternative Uptick Rule” (Rule 201) can be triggered if a stock drops more than 10% in a single day. Once triggered, short selling is only allowed on an “uptick”—meaning you can only sell at a price higher than the last best bid. This prevents short sellers from relentlessly driving a stock’s price into the ground.

#

Tax Implications

Short-term capital gains taxes usually apply to short sales. Because you never technically “own” the asset for a period of time in the traditional sense, almost all short-sale profits are taxed at your ordinary income tax rate, regardless of how long you hold the position. Always consult with a tax professional in 2026 to see if any specific “constructive sale” rules apply to your situation.

—

FAQ: Short Selling Stocks for Beginners

**Q1: Can I short sell stocks in a Roth IRA or 401(k)?**

Generally, no. IRS regulations prohibit short selling and the use of margin in most retirement accounts. However, you can achieve a similar result by purchasing “Inverse ETFs” within your IRA, as these are treated like regular stocks.

**Q2: How long can I hold a short position?**

Theoretically, there is no time limit, as long as you have enough collateral in your margin account and the lender doesn’t call back the shares. However, because of daily margin interest and borrow fees, shorting is typically a short-to-medium-term strategy.

**Q3: What is the minimum amount of money needed to start shorting?**

Most brokers require a minimum of $2,000 in equity to open a margin account. However, since you need to maintain a “maintenance margin” (often 30-35% of the position value), it is safer to start with a larger cushion to avoid accidental liquidation.

**Q4: What happens if the stock I shorted gets delisted?**

If a company goes bankrupt and its stock is delisted (valued at $0), the short seller wins. You essentially bought the shares back for nothing. You get to keep the entire initial sale amount, though you may have to wait for the bankruptcy process to finalize before the position is officially cleared from your account.

**Q5: Is short selling unethical?**

Short selling is a legitimate market function. It helps identify fraudulent companies (like the Enron or Wirecard scandals) and prevents stocks from becoming overvalued. While it feels “negative,” it provides a vital check and balance to the financial ecosystem.

—

Conclusion: Balancing the Scales

Short selling is an essential evolution for any retail investor who wants to move beyond passive “buy and hold” strategies. By learning to profit from downward movements, you effectively double your opportunities in the market. In the volatile landscape of 2026, the ability to hedge your losses and capitalize on overvalued assets is a significant competitive advantage.

However, with great profit potential comes the need for great discipline. The unlimited risk of shorting means that a single “short squeeze” can wipe out an unprepared trader. Start small, focus on high-liquidity stocks with low borrow fees, and always, without exception, use stop-loss orders. By mastering the mechanics and minimizing the costs of short selling, you can transform a falling market from a source of stress into a source of significant opportunity.