ETFs vs. Index Funds: The Definitive Guide for Cost-Conscious Investors in 2026

The landscape of modern investing has undergone a radical transformation. Gone are the days when retail investors were forced to pay exorbitant commissions to stockbrokers or high management fees to active fund managers who rarely beat the market. Today, the focus has shifted toward passive investing—a strategy designed to mirror the performance of a specific market index. Within this realm, two titans dominate: Exchange-Traded Funds (ETFs) and Index Mutual Funds.

While both vehicles offer a way to gain broad market exposure at a low cost, they are not identical. For the retail investor or trader in 2026, understanding the structural, tax, and operational differences between these two is the key to maximizing net returns. Whether you are building a retirement nest egg or executing a tactical swing trade, the choice between an ETF and an index fund can impact your bottom line by thousands of dollars over time. This guide breaks down the nuances to help you minimize costs and optimize your portfolio efficiency.

1. Trading Mechanics: Real-Time Precision vs. End-of-Day Simplicity

The most fundamental difference between ETFs and index funds lies in how they are bought and sold. This distinction is critical for traders and investors who value liquidity and timing.

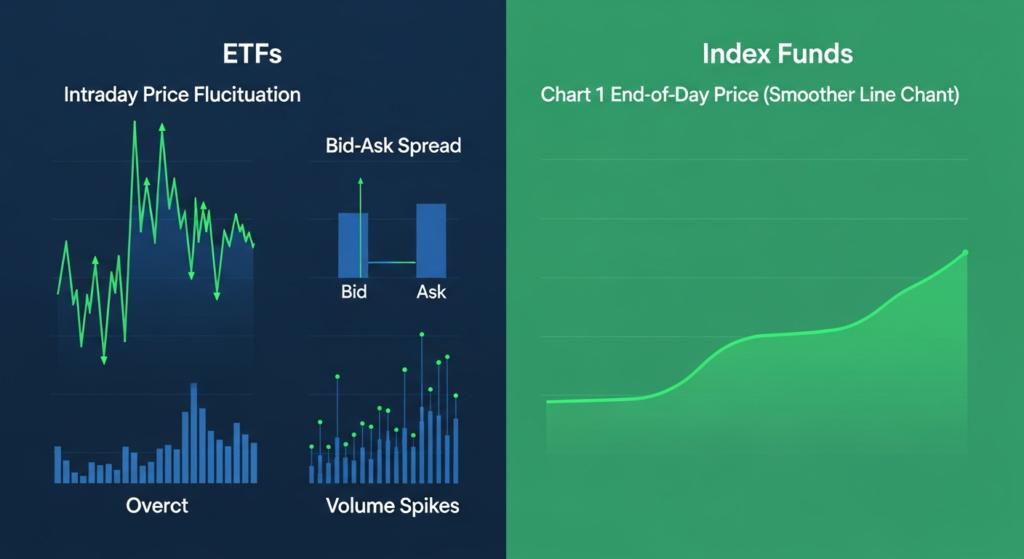

**Exchange-Traded Funds (ETFs):**

As the name suggests, ETFs trade on national stock exchanges, just like individual shares of Apple or Tesla. This means they offer intraday liquidity. You can buy or sell an ETF at any point during market hours at the current market price. For a trader, this allows for the use of advanced order types, such as limit orders, stop-loss orders, and even buying on margin or short-selling. In the volatile market environment of 2026, the ability to exit a position at 10:30 AM rather than waiting for the market close can be a significant advantage.

**Index Mutual Funds:**

Index funds are priced only once per day, after the market closes. When you place an order to buy or sell an index fund, your transaction is executed at the Net Asset Value (NAV) calculated at the end of the trading session. There is no “day trading” index funds. While this lack of immediacy might frustrate a tactical trader, it often benefits the long-term retail investor by preventing emotional, knee-jerk reactions to midday market swings. However, from a cost perspective, the inability to set a limit order means you have less control over your entry and exit points compared to an ETF.

2. Analyzing the Cost Structure: Expense Ratios and Beyond

For the cost-minimizing investor, the “sticker price” of a fund is the expense ratio. However, the total cost of ownership involves several hidden layers that differ between ETFs and index funds.

**Expense Ratios:**

Generally, both ETFs and index funds offer incredibly low expense ratios, often dipping below 0.05% for broad-market trackers. However, in the current 2026 landscape, ETFs frequently hold a slight edge. Because ETFs outsource the record-keeping and administrative tasks to the brokerage firms where they are traded, the fund providers (like Vanguard, BlackRock, or State Street) can operate them with lower overhead.

**Transaction Costs:**

This is where the math gets specific to your broker. Most major brokerages now offer commission-free trading for both ETFs and index funds. However, ETFs carry a “bid-ask spread”—the difference between the highest price a buyer is willing to pay and the lowest price a seller is willing to accept. If you are trading high volumes or choosing niche ETFs with low liquidity, these spreads can act as a hidden tax. Index funds do not have bid-ask spreads; you always trade at the NAV.

**Management Fees:**

Some index mutual funds carry “12b-1 fees,” which are annual marketing or distribution fees. While these are becoming rarer in the “low-cost” tier of funds, they are virtually non-existent in the ETF world. When minimizing costs, always check the prospectus for these secondary fees.

3. Tax Efficiency: The “In-Kind” Advantage

Taxation is often the largest “cost” an investor faces, yet it is frequently overlooked. ETFs are structurally more tax-efficient than index funds due to the way they handle the creation and redemption of shares.

When an investor wants to sell their shares in a traditional index mutual fund, the fund manager must often sell the underlying securities to generate the cash to pay the investor. If those securities have appreciated in value, the sale triggers a capital gain. By law, mutual funds must pass these capital gains on to all shareholders at the end of the year. This means you could owe taxes on gains you didn’t even participate in.

ETFs utilize an “in-kind” redemption process. Instead of selling stocks for cash, the ETF manager swaps the underlying securities with “authorized participants” for ETF shares. This exchange is not considered a taxable event by the IRS. Consequently, ETFs rarely trigger capital gains distributions. For investors holding assets in a taxable brokerage account (rather than a 401k or IRA), the ETF is almost always the superior choice for minimizing the “tax drag” on a portfolio.

4. Accessibility and Investment Minimums

For the retail investor just starting out, the barrier to entry is a major consideration. Historically, index funds required significant “initial minimum investments,” while ETFs were accessible for the price of a single share.

**Index Fund Minimums:**

Many popular index funds require a minimum initial investment ranging from $1,000 to $3,000. While some providers have waived these for certain account types, they can still be a hurdle for younger investors or those practicing a “core and satellite” strategy with smaller amounts of capital.

**ETF Accessibility:**

ETFs have no such minimums. You can buy a single share. Furthermore, in 2026, almost every major brokerage platform offers “fractional shares” for ETFs. This means if you have $10, you can buy $10 worth of an S&P 500 ETF, regardless of whether the share price is $400. This level of granularity makes ETFs the ultimate tool for retail investors looking to put every dollar of their paycheck to work immediately.

5. Dividend Reinvestment and Automation

Where index funds often reclaim the crown is in the realm of automation and “set it and forget it” investing.

**Automated Contributions:**

Most mutual fund platforms allow you to set up automatic recurring investments from your bank account. You can tell the system to buy $500 worth of an index fund every Friday. Because index funds trade in dollar amounts rather than shares, this process is seamless. While some brokers are catching up with automated ETF investing, the infrastructure for index funds is generally more mature and robust for those who want to automate their wealth building.

**Dividend Reinvestment (DRIP):**

Both vehicles allow for dividend reinvestment. However, with index funds, your dividends are typically reinvested back into the fund immediately and fully. With ETFs, unless your broker offers a specific DRIP (Dividend Reinvestment Plan) that supports fractional shares, your dividends might sit in your account as cash until you have enough to buy a full share. This “cash drag” can slightly diminish your long-term returns compared to the immediate reinvestment seen in index funds.

6. Strategic Suitability: Which One Should You Choose?

Deciding between an ETF and an index fund depends on your specific financial goals and the type of account you are using.

* **For the Taxable Brokerage Account:** The ETF wins. The tax-efficient structure of the “in-kind” exchange process ensures that you aren’t hit with unexpected capital gains distributions, allowing your money to compound more effectively over decades.

* **For the Active Trader:** The ETF wins. The ability to use limit orders, trade intraday, and utilize options for hedging makes the ETF a versatile tool for those who follow market trends closely.

* **For the Disciplined “Automator”:** The Index Fund wins. If your goal is to set up a recurring transfer from your paycheck and never look at the account, the simplicity and automated nature of index mutual funds remove the “decision fatigue” and potential for market-timing errors.

* **For the Small-Scale Investor:** The ETF wins. With the ubiquity of fractional shares and no minimum investment requirements, ETFs allow for maximum diversification even with a very small starting balance.

FAQ: Common Questions for 2026 Investors

**Q1: Can I switch from an Index Fund to an ETF without paying taxes?**

Generally, no. Selling an index fund to buy an ETF in a taxable account is a “taxable event.” However, some providers like Vanguard offer a unique structure where certain index funds have an ETF “share class,” allowing for a tax-free conversion. Always check with your brokerage before making the move.

**Q2: Is one safer than the other during a market crash?**

Neither is inherently “safer” in terms of market risk; both will fall if the underlying index falls. However, during periods of extreme volatility, ETFs can sometimes trade at a “discount” or “premium” to their NAV. Index funds always trade at the NAV, which can provide a sense of pricing certainty during chaos.

**Q3: Do ETFs and Index Funds hold the exact same stocks?**

If they track the same index (e.g., the S&P 500), their holdings will be virtually identical. The difference lies in the “wrapper” (the legal structure) around those stocks, not the stocks themselves.

**Q4: Which is better for a Roth IRA or 401k?**

Since these are tax-advantaged accounts, the tax efficiency of ETFs doesn’t matter. In these accounts, the choice should be based purely on the expense ratio and whether you prefer the automated features of an index fund or the trading flexibility of an ETF.

**Q5: Are there any “hidden” costs in ETFs I should look out for?**

Yes. Beyond the expense ratio, look at the “tracking error.” This is the difference between the fund’s performance and the index’s performance. A high tracking error means the fund is not doing a good job of mimicking the index, which is a hidden cost to the investor.

Conclusion: The Path to Low-Cost Wealth Building

In the showdown between ETFs and index funds, there is no universal “winner,” but there is a “better fit” for your specific strategy. For the retail investor focused on minimizing costs in 2026, the ETF offers superior tax efficiency and unparalleled accessibility. It is the tool of choice for those who want to control their entry points and avoid the “tax bite” of year-end distributions.

Conversely, the index mutual fund remains the gold standard for investors who prioritize automation and psychological discipline. By removing the temptation to trade during market hours and simplifying the contribution process, index funds help investors stay the course through the inevitable cycles of the market.

Ultimately, the best vehicle is the one that you can stick with for the long term. Whether you choose the real-time flexibility of the ETF or the end-of-day simplicity of the index fund, the key is to keep your expenses low, stay diversified, and let the power of the market work for you. In a world of complex financial products, these two passive powerhouses remain the most reliable paths to financial independence.