Understanding “Money While You Sleep”: The Power of Passive Income

The concept of “making money while you sleep” fundamentally revolves around passive income. Unlike active income, which requires your direct, ongoing involvement – such as a salary from a job or earnings from a client project – passive income streams are designed to generate revenue with minimal continuous effort once the initial setup is complete. This distinction is critical for anyone aspiring to genuine financial freedom. Imagine a scenario where your investments continue to grow, dividends are paid out, or rental income flows in, irrespective of whether you are at your desk, on vacation, or indeed, asleep. This isn’t about getting something for nothing; it’s about front-loading your effort and capital into systems that then operate semi-autonomously.

The primary benefit of passive income is its ability to decouple your income from your time. This liberation offers immense potential for lifestyle choices, early retirement, or simply reducing financial stress. It provides a safety net, allowing you to pursue passions, spend more time with family, or even switch careers without the immediate pressure of an active income source. However, it’s a common misconception that passive income requires no work at all. On the contrary, establishing truly passive income streams often demands significant upfront investment – whether of time, capital, or intellectual property – and typically requires ongoing maintenance, monitoring, and adaptation to market changes. The “set it and forget it” mantra is rarely 100% accurate, but the goal is to minimize active engagement over time.

In the context of investing, passive income usually derives from assets that produce regular returns without the owner needing to actively manage daily operations or transactions. This can range from the dividends paid by shares in profitable companies to the interest accrued on bonds, or the rent collected from real estate. The beauty of these mechanisms is their compounding potential. When the income generated is reinvested, it begins to earn its own income, creating a powerful snowball effect that can significantly accelerate wealth accumulation over the long term. Understanding this foundational principle is the first step toward building a financial strategy that truly works for you, even when you’re not actively working for it.

Laying the Foundation: Financial Literacy and Budgeting for Passive Income

Before embarking on any investment journey, especially one focused on generating passive income, a solid financial foundation is non-negotiable. This involves two critical components: enhancing your financial literacy and implementing effective budgeting strategies. You wouldn’t build a skyscraper on shaky ground, and similarly, you shouldn’t attempt to build a robust passive income portfolio without first understanding your current financial position and establishing healthy money habits. This foundational work ensures that the capital you allocate to investments is truly disposable and that your personal finances are resilient enough to withstand market fluctuations.

Financial literacy, in this context, means understanding core economic principles, investment vehicles, risk management, and tax implications. It’s about empowering yourself with the knowledge to make informed decisions rather than relying solely on external advice. Reading financial news, taking online courses, and engaging with reputable financial blogs like Trading Costs are excellent starting points. Knowledge is your most powerful asset when it comes to navigating the complexities of the investment world.

Equally important is effective budgeting. To start investing, especially if you’re asking “How To Start Investing Little Money 2026,” you first need to identify and free up capital. This is where budgeting becomes your best friend. A well-structured budget allows you to track your income and expenses, identify areas where you can save, and consciously allocate funds towards your investment goals. Many people mistakenly believe budgeting is restrictive, but in reality, it’s an empowering tool that gives you control over your money. For 2026, the landscape of personal finance technology offers an array of sophisticated tools. When considering the Best Money Apps Budgeting 2026, look for those that offer intuitive interfaces, automated expense tracking, categorization, goal setting, and robust security features. Apps like Mint, YNAB (You Need A Budget), Personal Capital, or even specialized banking apps, can provide invaluable insights into your spending habits and help you systematically save for investments. The goal is to create a surplus each month that can be consistently channeled into your passive income strategies.

Beyond budgeting, it’s crucial to address existing high-interest debt, such as credit card balances. The interest paid on such debts often far outweighs any potential returns from conservative passive income investments, effectively creating a negative passive income stream. Prioritizing debt reduction before aggressive investing is usually a sound financial move. Once your financial house is in order – with an emergency fund established, high-interest debt minimized, and a clear understanding of your cash flow – you are then truly ready to begin allocating capital towards income-generating assets. This meticulous preparation is not merely a formality; it’s a strategic prerequisite for sustainable wealth creation.

Core Investment Strategies for Passive Income Generation

Dividend Stocks: A Timeless Income Stream

Investing in dividend stocks is one of the most classic and widely adopted strategies for passive income. When you own shares in a company that pays dividends, you receive a portion of the company’s profits, typically on a quarterly basis, simply for being a shareholder. These payments can provide a consistent income stream that grows over time, especially if you choose companies with a history of increasing their dividends. Look for established companies with strong balance sheets, stable earnings, and a proven track record of returning value to shareholders. While dividend stocks are generally considered a more stable form of passive income compared to speculative growth stocks, they are not without risk. Company performance can impact dividend payouts, and the stock price itself can fluctuate. However, for those looking for a long-term, relatively hands-off approach, reinvesting dividends can significantly compound your returns over decades, making it an excellent strategy for building wealth while you sleep.

Real Estate: Beyond Direct Ownership

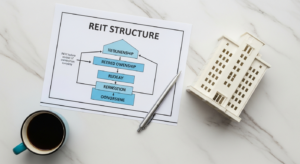

While direct ownership of rental properties can be a lucrative source of passive income, it often demands significant upfront capital and active management (finding tenants, maintenance, etc.). For investors seeking real estate exposure with less direct involvement, Real Estate Investment Trusts (REITs) offer an excellent alternative. REITs are companies that own, operate, or finance income-producing real estate across various sectors like commercial, residential, healthcare, and retail. They are legally required to distribute at least 90% of their taxable income to shareholders annually, typically in the form of dividends. This makes them highly attractive for passive income generation. Investing in REITs allows you to gain exposure to real estate without the complexities of property management, offering diversification and liquidity similar to stocks. Furthermore, real estate crowdfunding platforms are emerging as a viable option for those asking “How To Start Investing Little Money 2026,” allowing individuals to pool funds and invest in larger real estate projects for a share of the returns, democratizing access to this asset class.

Bonds and Fixed-Income Securities: Stability and Predictability

Bonds represent a loan made by an investor to a borrower (typically a corporation or government entity). In return for the loan, the borrower promises to pay the investor regular interest payments over a specified period, and then repay the original principal amount at maturity. Bonds are generally considered less volatile than stocks and can provide a predictable stream of income, making them a cornerstone for many passive income portfolios, especially for risk-averse investors or those nearing retirement. Government bonds (like Treasury bonds) are often considered among the safest investments, while corporate bonds carry slightly higher risk but often offer higher yields. While bond yields might not always match the growth potential of equities, their stability and regular interest payments offer a dependable source of passive income, balancing out the risk of a more aggressive portfolio. For those starting with smaller amounts, bond ETFs (Exchange Traded Funds) or mutual funds can provide diversified exposure to a basket of bonds.

High-Yield Savings Accounts and Certificates of Deposit (CDs)

For individuals asking “How To Start Investing Little Money 2026” or those prioritizing capital preservation, high-yield savings accounts and Certificates of Deposit (CDs) offer a low-risk way to earn passive income. While the interest rates might not compete with market returns from stocks or real estate, they provide guaranteed returns and are typically FDIC-insured, making them extremely safe. High-yield savings accounts offer liquidity, allowing you to access your funds when needed, while CDs lock your money away for a specific term in exchange for a slightly higher, fixed interest rate. These options are excellent for parking your emergency fund or short-term savings, ensuring your money earns something rather than sitting idle, and building a habit of earning income from your capital, however modest the initial sums.

Advanced Strategies for Enhanced Passive Returns

Once you’ve established a foundation with traditional passive income streams, you might consider more advanced strategies to potentially accelerate your returns. These often involve a higher degree of complexity or risk but can offer significant income-generating potential for the informed investor.

Options Trading for Income: A More Active Passive Approach

While often perceived as highly speculative, certain options trading strategies can be employed to generate consistent passive income, albeit with a more active management component than simply holding dividend stocks. For those exploring an Options Trading Beginners Guide, it’s crucial to understand that not all options strategies are about high-risk speculation. Strategies like writing covered calls or selling cash-secured puts can generate premium income on a regular basis.

A covered call involves owning shares of a stock and then selling call options against those shares. You collect a premium for selling the option. If the stock price stays below the strike price by expiration, the option expires worthless, and you keep the premium and your shares. If the stock rises above the strike price, your shares might be “called away” (sold) at the strike price, but you still keep the premium, and potentially profit from the stock’s appreciation up to that point. This strategy is ideal for stocks you already own and are comfortable selling at a specific price, or for generating extra income on relatively stagnant holdings.

A cash-secured put involves selling a put option and setting aside enough cash to buy the underlying stock if the option is exercised. You collect a premium upfront. If the stock price stays above the strike price, the option expires worthless, and you keep the premium. If the stock falls below the strike price, you are obligated to buy the shares at the strike price. This strategy is suitable for stocks you wouldn’t mind owning at a certain price, effectively allowing you to get paid for waiting for a potential entry point.

It’s important to emphasize that options trading requires a deep understanding of market mechanics, volatility, and risk management. It’s not a “set it and forget it” strategy and demands ongoing monitoring. A thorough Options Trading Beginners Guide will always stress starting small, using a paper trading account, and understanding the potential for capital loss before committing real money. However, for the disciplined and knowledgeable investor, these strategies can be powerful tools for enhancing passive income.

Peer-to-Peer (P2P) Lending: Direct Lending for Returns

Peer-to-Peer (P2P) lending platforms connect individual investors directly with borrowers, bypassing traditional banks. As an investor, you can lend money to individuals or small businesses and earn interest on those loans. Platforms like LendingClub or Prosper allow you to diversify your investments across many small loans, mitigating the risk of any single default. The interest rates offered on P2P loans can be significantly higher than traditional savings accounts or even some bonds, making them attractive for income generation. While it offers potentially higher returns, P2P lending also carries risks, primarily default risk. Borrowers may fail to repay their loans, leading to a loss of capital. Diversification across numerous loans and careful selection of borrowers (often aided by the platform’s credit scoring) are crucial to managing this risk. For those comfortable with a slightly higher risk profile in exchange for better yields, P2P lending can be a compelling passive income stream for 2026.

Creating Digital Products and Content: Leveraging Your Expertise

While not strictly an investment in the traditional sense, creating digital products or content can evolve into a significant source of passive income. This involves an initial, often substantial, investment of time and effort to create assets that can then be sold repeatedly with minimal ongoing work. Examples include writing and self-publishing an e-book, creating an online course, developing a software application, or building a monetized blog or YouTube channel. Once the product is created and marketed, sales can generate income around the clock. The beauty of this approach is its scalability and low marginal cost per sale. While the initial “work” phase is active, the subsequent “income” phase can be largely passive. This strategy often appeals to individuals with specialized knowledge or creative talents who are looking to leverage their expertise beyond a traditional job, creating an asset that works for them while they sleep.

The Role of Automation and Long-Term Vision in Passive Income

Achieving true financial freedom through passive income isn’t just about selecting the right investment vehicles; it’s equally about establishing efficient systems and maintaining a long-term perspective. Automation and a clear vision for the future are powerful allies in transforming sporadic income streams into a robust, self-sustaining financial engine.

Automating Your Investments

One of the most effective ways to ensure consistency in your passive income journey is to automate your contributions. Many brokerage firms and investment platforms allow you to set up automatic transfers from your checking or savings account directly into your investment accounts. Whether it’s a fixed amount invested weekly, bi-weekly, or monthly into a dividend stock portfolio, an ETF, or even a P2P lending account, automation removes the psychological barrier of manually initiating investments and ensures you’re consistently putting your money to work. This strategy also benefits from dollar-cost averaging, where you invest a fixed amount regularly, regardless of market fluctuations. Over time, this can reduce the impact of volatility by ensuring you buy more shares when prices are low and fewer when prices are high, leading to a lower average cost per share. This “set it and forget it” approach to contributions is perhaps the closest you can get to truly making money while you sleep, as it ensures your capital is continuously deployed without your daily intervention.

The Power of Compounding and Reinvestment

The magic of passive income truly unfolds through the power of compounding. When the income generated by your investments (e.g., dividends, interest, rental profits) is reinvested back into the same or new income-generating assets, that reinvested money begins to earn its own returns. This creates an exponential growth effect, often referred to as “interest on interest.” For example, if you own dividend stocks and choose to automatically reinvest those dividends, you’ll acquire more shares over time, which in turn generate even more dividends, accelerating your wealth accumulation. This principle applies across various asset classes. The earlier you start investing and the more consistently you reinvest your returns, the greater the impact of compounding will be over the long term. This is why patience and discipline are paramount in any passive income strategy. It might take years to see substantial results, but the cumulative effect can be truly transformative.

Patience, Consistency, and Adaptability

Building significant passive income streams is rarely an overnight phenomenon. It requires immense patience, unwavering consistency, and the adaptability to navigate changing market conditions. There will be market downturns, periods of low returns, and perhaps even some initial investment failures. A long-term vision allows you to ride out these inevitable fluctuations without panic-selling or abandoning your strategy. Regularly review your portfolio, not to react to every market whim, but to ensure your investments still align with your goals and risk tolerance. As your financial situation changes or new opportunities arise (or old ones diminish), be prepared to adjust your strategy. This might involve rebalancing your portfolio, exploring new investment vehicles, or even increasing your automated contributions. The journey to making money while you sleep is a marathon, not a sprint, and those who succeed are often those who remain steadfast in their approach while being flexible enough to adapt.

Mitigating Risks and Diversification for Sustainable Passive Income

While the prospect of making money while you sleep is incredibly appealing, it’s crucial to approach passive income strategies with a clear understanding of the inherent risks. No investment is entirely risk-free, and the pursuit of passive income requires thoughtful risk management and strategic diversification to ensure sustainability and protect your capital. A well-diversified portfolio is your strongest defense against the unpredictable nature of financial markets and individual asset performance.

Understanding and Managing Investment Risks

Every passive income stream comes with its own set of risks. For dividend stocks, there’s the risk of dividend cuts or suspension if a company’s financial health deteriorates. REITs are susceptible to real estate market downturns and interest rate changes. Bonds carry interest rate risk (their value can fall if interest rates rise) and credit risk (the issuer might default). Even high-yield savings accounts are exposed to inflation risk, where the purchasing power of your money erodes if inflation outpaces your interest earnings. Options trading, as discussed in any comprehensive Options Trading Beginners Guide, involves significant risk of capital loss if not managed properly. The first step in mitigation is education: understand the specific risks associated with each investment you choose.

Beyond understanding, active management of these risks is essential. This includes:

- Due Diligence: Thoroughly research any company, property, or platform before investing.

- Risk Assessment: Only invest what you can afford to lose, especially in higher-risk ventures.

- Stop-Loss Orders: For actively traded assets, these can limit potential losses.

- Regular Monitoring: Keep an eye on the performance of your investments and the broader economic landscape.

The Imperative of Diversification

Diversification is the bedrock of intelligent investing, particularly for passive income generation. It involves spreading your investments across different asset classes, industries, geographic regions, and even types of passive income streams. The principle is simple: don’t put all your eggs in one basket. If one investment performs poorly, others in your diversified portfolio may perform well, cushioning the overall impact on your returns. For example:

- Across Asset Classes: Don’t just invest in dividend stocks; consider REITs, bonds, and possibly some P2P lending to spread risk.

- Within Asset Classes: If you invest in dividend stocks, diversify across different industries (e.g., tech, healthcare, utilities) and market capitalizations (large-cap, mid-cap). For REITs, diversify across different property types (residential, commercial, industrial).

- Geographic Diversification: Consider international investments to reduce reliance on a single economy.

- Income Source Diversification: Mix passive income from investments with potential income from digital products or other ventures to create multiple streams.

Diversification helps to smooth out portfolio returns over time, reducing volatility and making your passive income streams more reliable. It’s a strategy that acknowledges the inherent unpredictability of markets and aims to protect your financial future by spreading risk, ensuring that even if one component of your “money while you sleep” strategy falters, your entire edifice doesn’t collapse. Regularly rebalancing your diversified portfolio – adjusting allocations back to your target percentages – is also a crucial practice to maintain optimal risk exposure and align with your evolving financial goals for 2026 and beyond.

FAQ: Making Money While You Sleep

Is it really possible to make money while I sleep?

Yes, absolutely. The concept of “making money while you sleep” is synonymous with generating passive income. This involves setting up income streams that, once established, require minimal ongoing effort to maintain. Examples include dividends from stocks, interest from bonds, rental income from real estate (or REITs), royalties from intellectual property, or premium income from certain options strategies. While it requires initial capital, time, and strategic planning, the goal is to decouple your income from your active working hours, allowing your investments to generate returns around the clock.

How much money do I need to start investing for passive income?

You can start investing for passive income with surprisingly little money, especially in 2026 with fractional shares and micro-investing apps. Many platforms allow you to start with as little as $5 or $10. For example, you can invest in dividend-paying ETFs or mutual funds with small, regular contributions. High-yield savings accounts require no minimum to open. While larger sums will naturally generate more significant passive income, the key is to start early and consistently, leveraging the power of compounding over time. Strategies like those discussed in “How To Start Investing Little Money 2026” emphasize accessibility for all budget sizes.

What are the safest passive income investments?

Generally, the safest passive income investments prioritize capital preservation over high returns. These include high-yield savings accounts, Certificates of Deposit (CDs), and government bonds (like U.S. Treasury bonds). These options are typically FDIC-insured (for bank accounts) or backed by the full faith and credit of the government, making them very low-risk regarding principal loss. However, “safest” often means lower returns, and these investments may not keep pace with inflation. For slightly higher, yet still relatively low-risk options, consider diversified portfolios of investment-grade corporate bonds or stable, dividend-paying blue-chip stocks with a long history of payouts.

Can I use options trading for passive income as a beginner?

While options trading can be used for passive income through strategies like covered calls or cash-secured puts, it is generally not recommended for absolute beginners without significant education and practice. Options involve leverage and can lead to rapid capital loss if misunderstood or mismanaged. A comprehensive “Options Trading Beginners Guide” would always emphasize starting with a deep understanding of options mechanics, volatility, and risk management, often through paper trading (simulated trading) before committing real capital. It’s a more advanced strategy that requires active monitoring and is not a “set it and forget it” passive income stream.

How do I choose the best budgeting app for 2026?

Choosing the “Best Money Apps Budgeting 2026” depends on your individual needs and preferences. Look for apps that offer:

- Intuitive Interface: Easy to navigate and understand.

- Automated Tracking: Links to your bank accounts and credit cards for automatic transaction categorization.

- Goal Setting: Features to help you save for specific financial goals.

- Reporting: Visualizations and insights into your spending habits.

- Security: Robust encryption and privacy measures.

- Cost: Some are free, others have subscription fees.

Popular choices often include Mint, YNAB (You Need A Budget), Personal Capital, and Rocket Money. Trialing a few free versions can help you find the best fit.

What’s the biggest mistake people make when pursuing passive income?

The biggest mistake people make is often the expectation of instant riches with no effort or initial investment. Passive income requires significant upfront work, capital, or time to establish, and ongoing maintenance. Other common mistakes include:

- Lack of Diversification: Putting all funds into one type of asset or a single investment.

- Ignoring Risk: Underestimating the potential downsides of investments.

- Lack of Patience: Giving up too soon when returns aren’t immediate.

- Poor Financial Foundation: Trying to invest for passive income before managing debt or building an emergency fund.

- Not Reinvesting: Failing to leverage compounding by spending all generated income instead of reinvesting some of it.

A long-term, disciplined, and educated approach is crucial for sustainable success.

Recommended Resources

Explore How To Create A Marketing Budget For Small Businesses for additional insights.

Learn more about this topic in Amazon Prime Benefits Worth It Guide at Gold Points.